Compounder Fund: Teladoc Health Sell Thesis - 21 Nov 2022

Data as of 20 November 2022

Compounder Fund’s investment in Teladoc Health (NYSE: TDOC) can be traced to Livongo, which is one of the 40 companies in the fund’s initial portfolio.

We first bought shares of Livongo in July 2020. A few months after our investment, Livongo was acquired by Teladoc in October 2020 in a stock and cash deal. After assessing the deal and the business prospects of the combined Teladoc and Livongo entity, we decided to keep the Teladoc shares that were given to Compounder Fund as part of the acquisition. Our investment thesis for Teladoc can be found here. In mid-August this year, we made a full sale of Compounder Fund’s Teladoc shares. This article describes our Sell thesis for the company.

When we first invested in Teladoc, the tele-health specialist had a multi-year history of rapid growth in (1) revenue, (2) telehealth visits, (3) US paid members, and (4) visit-fee-only individuals. But as time passed after our investment, the company’s performance in a number of these key areas has weakened significantly.

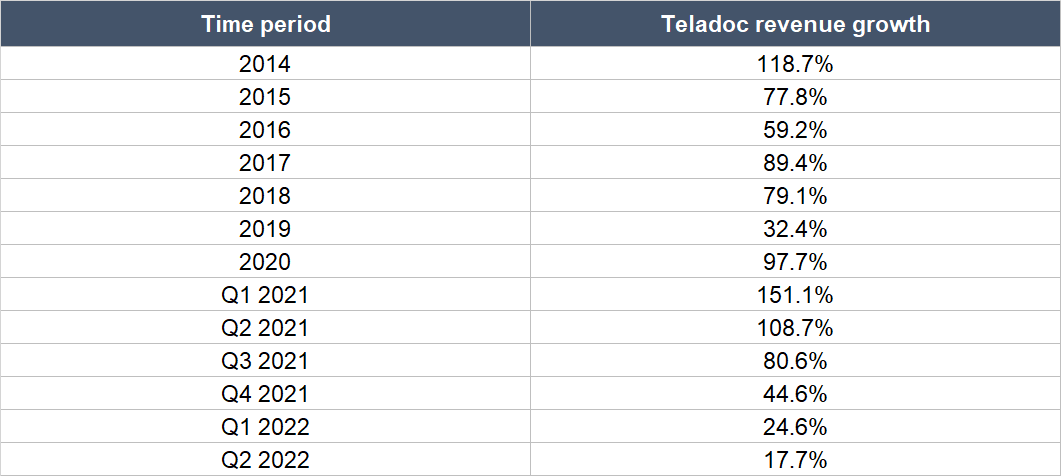

Table 1 below shows Teladoc’s revenue growth from 2014 to the third quarter of 2022. The growth rate had slowed markedly from 97.7% in 2020, to less than 25% in the second and third quarters of 2022. During 2020, Teladoc benefitted from the emergence of COVID-19 (telehealth services became an important avenue for individuals to access medical care) as well as the acquisitions of InTouch Health and Livongo in the second half of the year. So it’s not especially troubling to observe a slowdown in Teladoc’s revenue growth in the subsequent quarters after 2020.

Table 1; Source: Teladoc annual reports and quarterly earnings

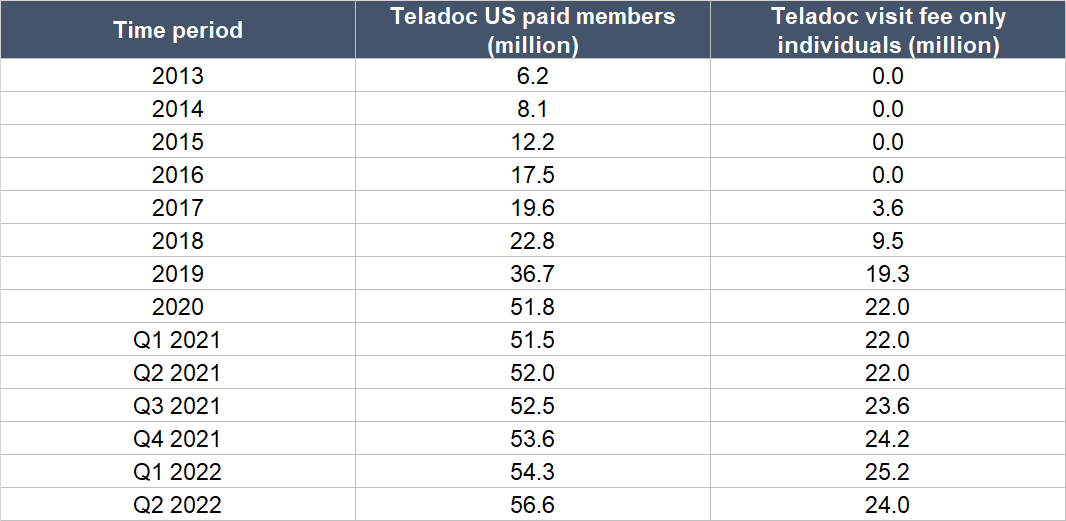

But the lower revenue growth became a concern for us when paired with Teladoc’s failure to showcase any material increase in US paid members and visit-fee-only individuals after 2020. This is illustrated in Table 2 below.

Table 2; Source: Teladoc annual reports and quarterly earnings

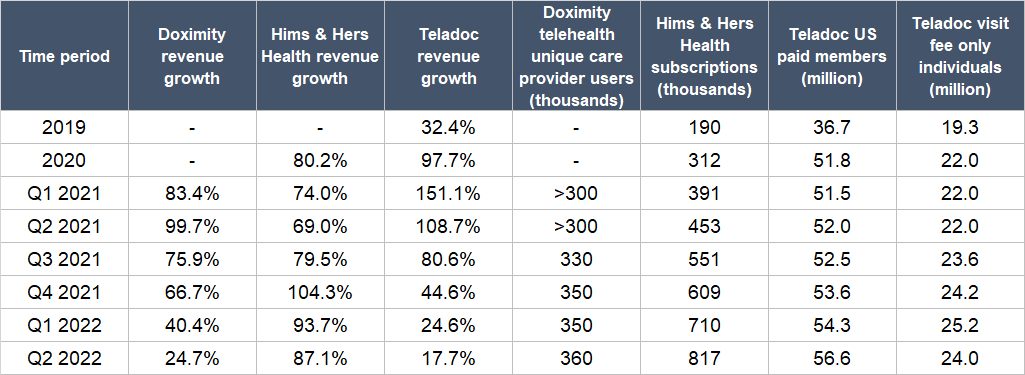

These data points, together, painted a picture in our mind of a company that has failed to execute well. Making this image clearer was the way other US companies with telehealth services – such as Doximity and Hims & Hers Health – managed to post faster growth (sometimes materially so) in overall revenues and telehealth adoption after 2020 compared to Teladoc’s record. Table 3 shows this (note that Teladoc’s revenue growth in the first and second quarters of 2021 benefited from the acquisitions of Livongo and InTouch Health in the second half of 2020):

Table 3; Source: Companies’ annual reports and quarterly earnings

Making matters worse was Teladoc’s massive impairments of goodwill of US$9.6 billion in total in the first half of 2022; for perspective, Teladoc’s revenue for the 12 months ended 30 June 2022 was US$2.23 billion. These impairments were mostly related to the Livongo acquisition (the deal resulted in recognition of US$12.9 billion of goodwill, which made up the lion’s share of Teladoc’s total goodwill of US$14.5 billion at the end of 2021) and the deterioration in Livongo’s business growth. It highlights a weakness in Teladoc management’s capital allocation process as well as our mistake in initially thinking that Livongo would exhibit durable and high revenue growth when we first invested in the company in July 2020.

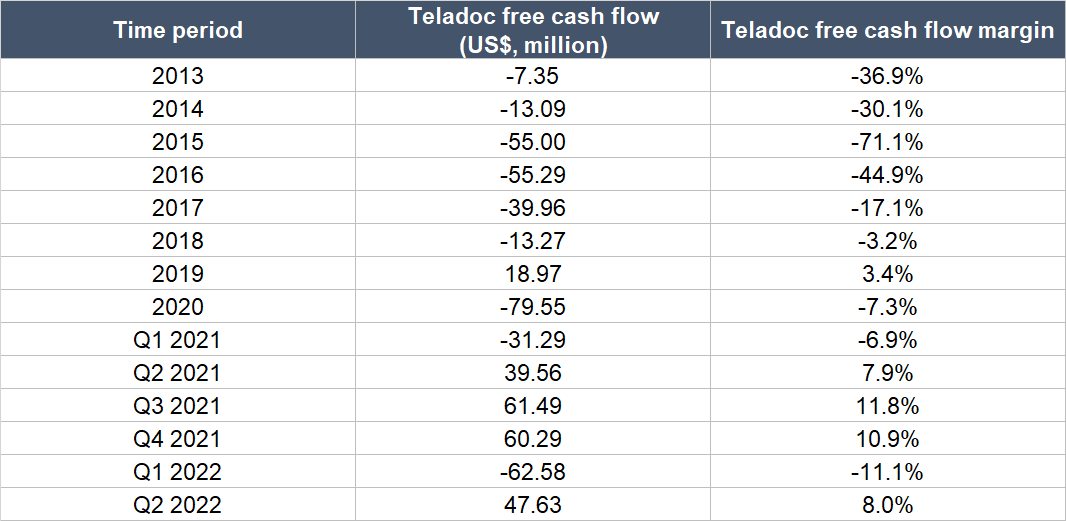

One positive development at Teladoc since our investment is the emergence of positive free cash flow and the gradual improvement in its free cash flow margin (free cash flow as a percentage of revenue) – this is shown in Table 4. But we thought the negative developments at the company overwhelmed this positive change.

Table 4; Source: Teladoc’s annual reports and quarterly earnings

With our analysis of Teladoc being wrong, we decided to sell and redeploy the capital elsewhere.