Compounder Fund: Starbucks Investment Thesis - 03 Mar 2021

Data as of 28 February 2021

Starbucks Corporation (NASDAQ: SBUX), which is listed and headquartered in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Most of you reading this should be familiar with Starbucks. The company is one of – if not the – largest speciality coffee chains in the world. As of 27 December 2020, it had 32,938 stores worldwide, of which 15,340 and 4,863 were in the USA and China, respectively. The rest of the stores come from other parts of the world. The USA and China are the two most important countries for the company.

Starbucks has two different business models for its coffee stores: (1) There are company-operated stores, where Starbucks earns revenues directly from customers who make purchases at the stores; and (2) Licensed-stores, where Starbucks earns revenue from royalties, licensing fees, and a margin from the sale of coffee, tea, food, and other products to licensees. The licensed stores in Starbucks’ portfolio are run by established and experienced retailers with in-depth market knowledge; the licensees also provide Starbucks with improved – and sometimes the only – access to good store locations.

Of the 32,938 stores that Starbucks currently has, 50.8% (16,742) are company-operated while 49.2% (16,196) are licensed-stores. Within the USA, around 60% of Starbucks’s stores are company-operated. Starbucks only has company-operated stores in China.

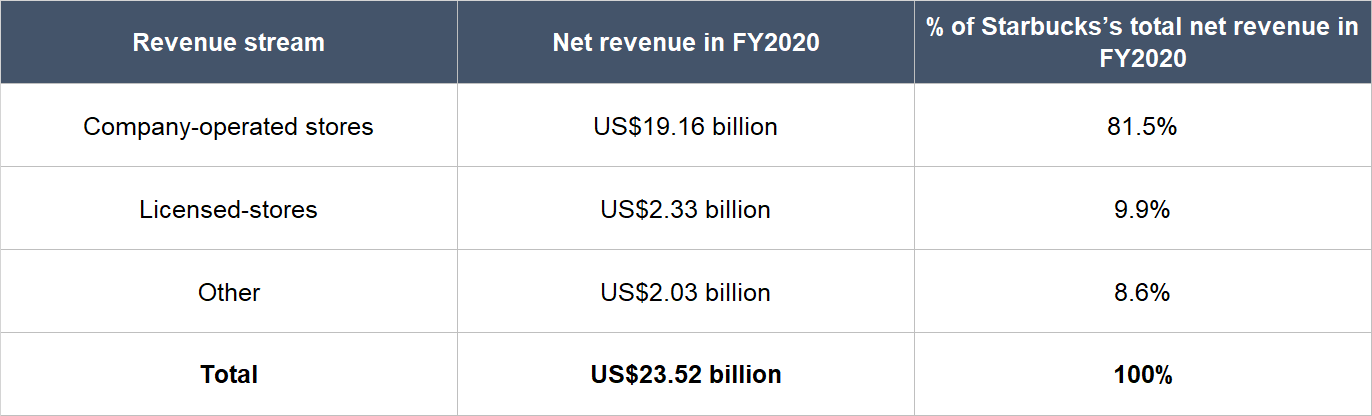

In the fiscal year ended 27 September 2020 (FY2020), Starbucks earned US$23.52 billion in net revenue. The table below shows a breakdown of the net revenue from company-operated stores, licensed stores, and other revenue streams that are grouped together as “Other”. The Other revenues are also known as the Channel Development segment, and it consists of (1) sales of packaged coffee, tea, and beverage products to consumers in retail locations such as supermarkets and convenience stores, and (2) royalties received from partnerships, such as the Global Coffee Alliance with Nestlé.

(Starbucks established the Global Coffee Alliance with Nestlé in May 2018. Under the terms of the partnership, Nestlé received rights to market, sell, and distribute Starbucks-branded products in authorized channels. In exchange, Starbucks would receive royalties from Nestlé. When the partnership was first set up, Nestlé prepaid around US$7 billion in royalties to Starbucks. This US$7 billion would be recognised as revenue by Starbucks over time.)

Source: Starbucks annual report

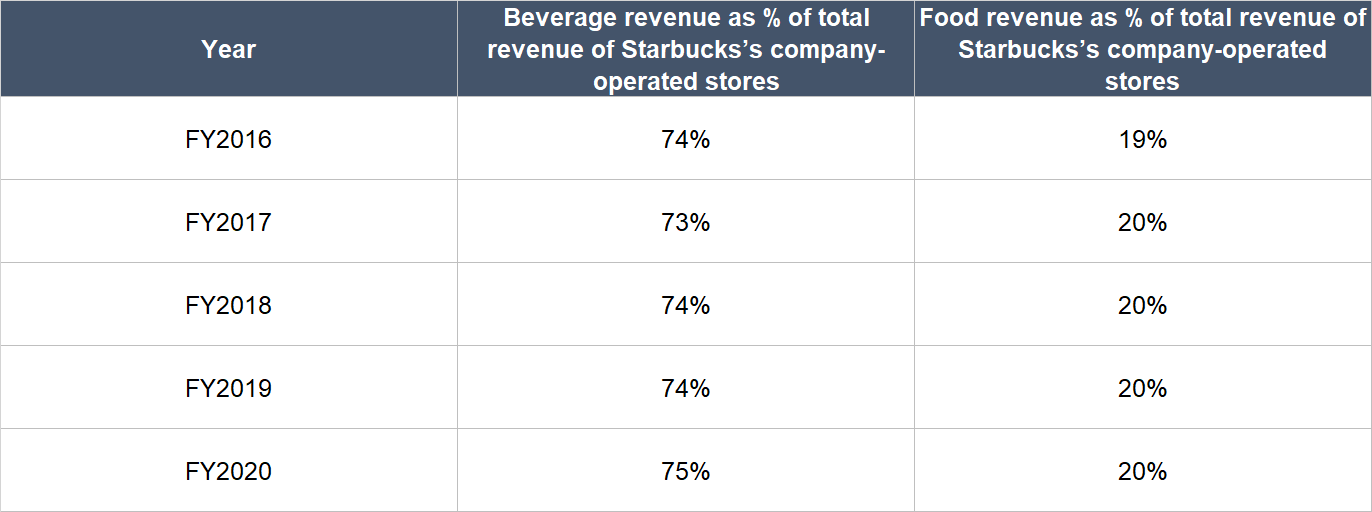

Within Starbucks’s company-operated stores, 75% of the US$19.16 billion in revenue in FY2020 came from the sale of beverages. Food was the next largest product-category at 20%. The remaining 5% came from serveware as well as packaged and ready-to-drink beverages.

For a geographical perspective, 71.8% of Starbucks’s total net revenue in FY2020 came from the USA. China accounted for 11.0% and other countries around the world (primarily Japan, Canada, and the UK) made up the remaining 17.2%.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Starbucks.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

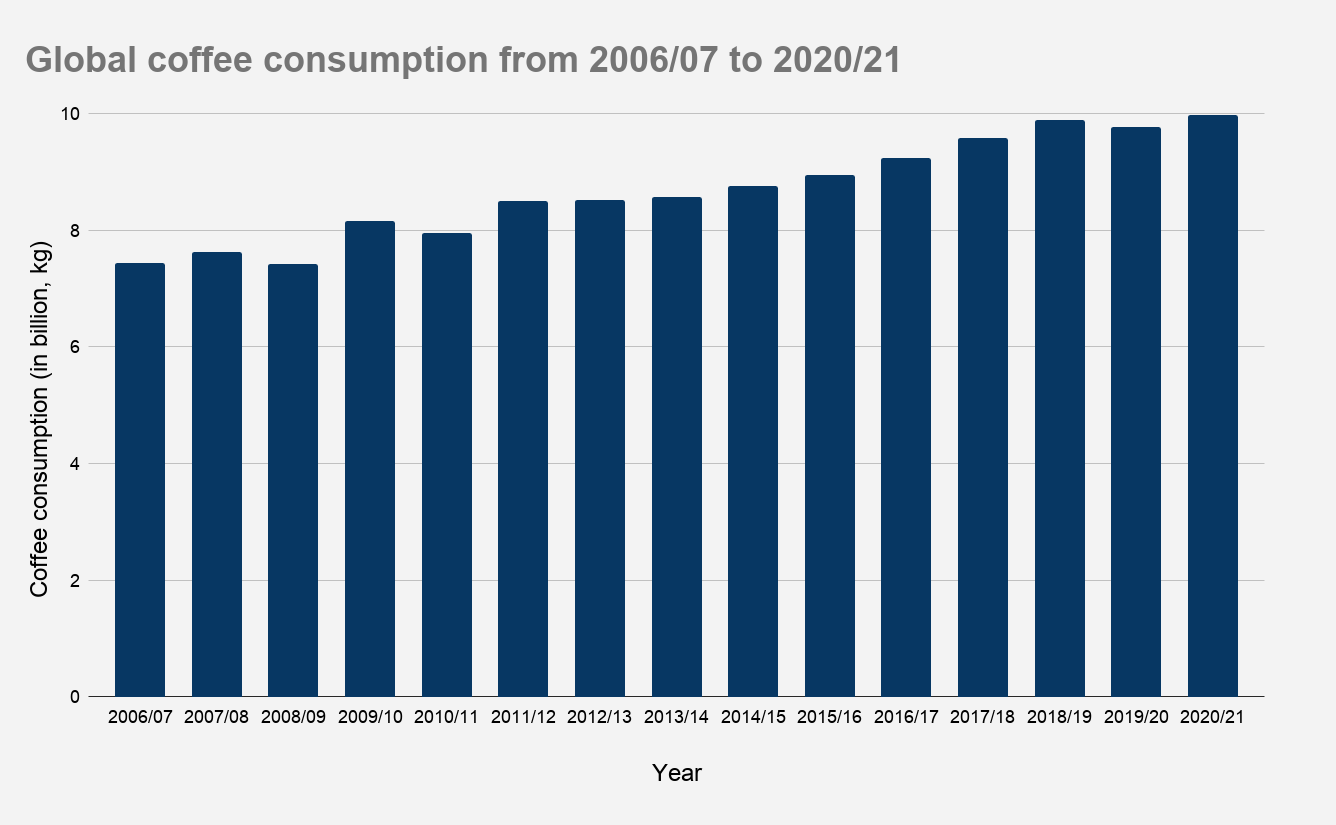

People drink a lot of coffee. According to the USA Department of Agriculture, global coffee consumption over the past year was around 9.98 billion kilograms worth of beans. The Specialty Coffee Association states that for a good cup of coffee to be made, the coffee-to-water ratio should be around 8.25 grams of coffee beans to 150 milliliters of water. Using this ratio, the amount of coffee that people all across the world drank over the past year (as a beverage) was around a staggering 180 billion litres. This works out to roughly 23 litres per person per year.

The long-term growth in coffee demand around the world is not spectacular (a compound annual growth rate of 2.1% for the past 14 years) but it has been remarkably steady. These traits about global coffee consumption are shown in the chart below:

Source: USA Department of Agriculture

Source: USA Department of Agriculture

This huge appetite for coffee in the world creates a large market opportunity for Starbucks. According to Statista, the global coffee market is currently US$437 billion, with the USA accounting for US$81.2 billion. For perspective, Starbucks’s net revenue in the 12 months ended 27 December 2020 was just US$23.17 billion. It’s worth noting that for Starbucks’s licensed-stores, the company counts only licensing fees, royalty fees, and a margin from the sale of products to the licensees as net revenue. So if we account for the full revenues from the licensed-stores, the total consumer expenditure that Starbucks enjoyed over the past year is likely close to US$40 billion (there’s a pretty even split in the number of company-operated stores and licensed stores). Nonetheless, the market opportunity in the USA and globally still seems large for Starbucks.

Importantly, we also think that the global coffee market is likely to continue growing in the future. This comes from the steady long-term growth in coffee consumption around the world that we mentioned earlier.

On the part of Starbucks, the company is looking to increase its retail footprint to win an even greater share of the massive global coffee market. During Starbucks’s 2020 Biennial Investor Day event held in December, management shared that the company is looking to increase its store count from around 33,000 today (across 83 markets) to 55,000 in 10 years’ time (across 100 markets).

Source: Starbucks 2020 Biennial Investor Day presentation

Source: Starbucks 2020 Biennial Investor Day presentation

We’re also particularly intrigued by the China opportunity for Starbucks, despite some estimates pegging the company’s market share in the country to already be around 80%. This is because we see two key growth drivers for Starbucks in China.

First, there’s the potential for higher coffee consumption in the country. According to research firm Euromonitor, China’s citizens consumed just 5.4 cups of coffee per capita in 2019, compared to 341 cups in the USA and 591 in Western Europe. There’s plenty of room for the gap in consumption to close, even if China never gets anywhere close to the level of coffee consumption seen in the Western world.

Second, there’s the potential for Starbucks to open more stores in China. Starbucks currently has only 4,863 stores in the country. With China’s population of 1.44 billion, this works out to around 300,000 people per store. For context, there are over 140 Starbucks outlets in Singapore and we have a population of 5.88 million here (we live in Singapore), which equates to around 40,000 people per store. In the USA, the ratio is around 21,500 people per store (15,340 stores and a population of 332 million). During Starbucks’s aforementioned 2020 Investor Day, management shared that China will be one of the company’s fastest-growing countries in terms of store openings for FY2022 through to FY2024 – see the chart below.

Source: Starbucks 2020 Biennial Investor Day presentation

Source: Starbucks 2020 Biennial Investor Day presentation

Starbucks also has more than just the coffee market. Over the past few years, as shown in the table below, food sales have made up around 20% of the total revenue from Starbucks’s company-operated stores. Beverages, meanwhile, accounted for around 75%. But even then, the beverages Starbucks sells go beyond just coffee. And other beverage markets are also huge. For example, Starbucks also tea and the global tea market was US$55 billion in 2019, according to Allied Market Research.

Source: Starbucks annual reports

2. A strong balance sheet with minimal or a reasonable amount of debt

At first glance, Starbucks’s balance sheet looks horrible. As of 27 December 2020, the coffee giant held US$5.45 billion in cash and investments, but had US$15.92 billion in total debt. In addition, there were operating lease liabilities of US$9.02 billion. But a different picture emerges if we look beneath the latte foam. Starbucks has highly recurrent revenues and a strong ability to generate free cash flow (we will discuss both later). These two traits mean that Starbucks is able to take on debt while still keeping risk low. There are two other things that give us comfort.

First, the amount of debt Starbucks has is not too taxing for itself, in our opinion. The company currently has net debt (total debt, net of cash and investments) of US$10.47 billion against free cash flow of US$3.24 billion in FY2019. (We used free cash flow for FY2019 because we think it’s a good representation for the kind of free cash flow Starbucks can generate when COVID-19 eventually blows over.)

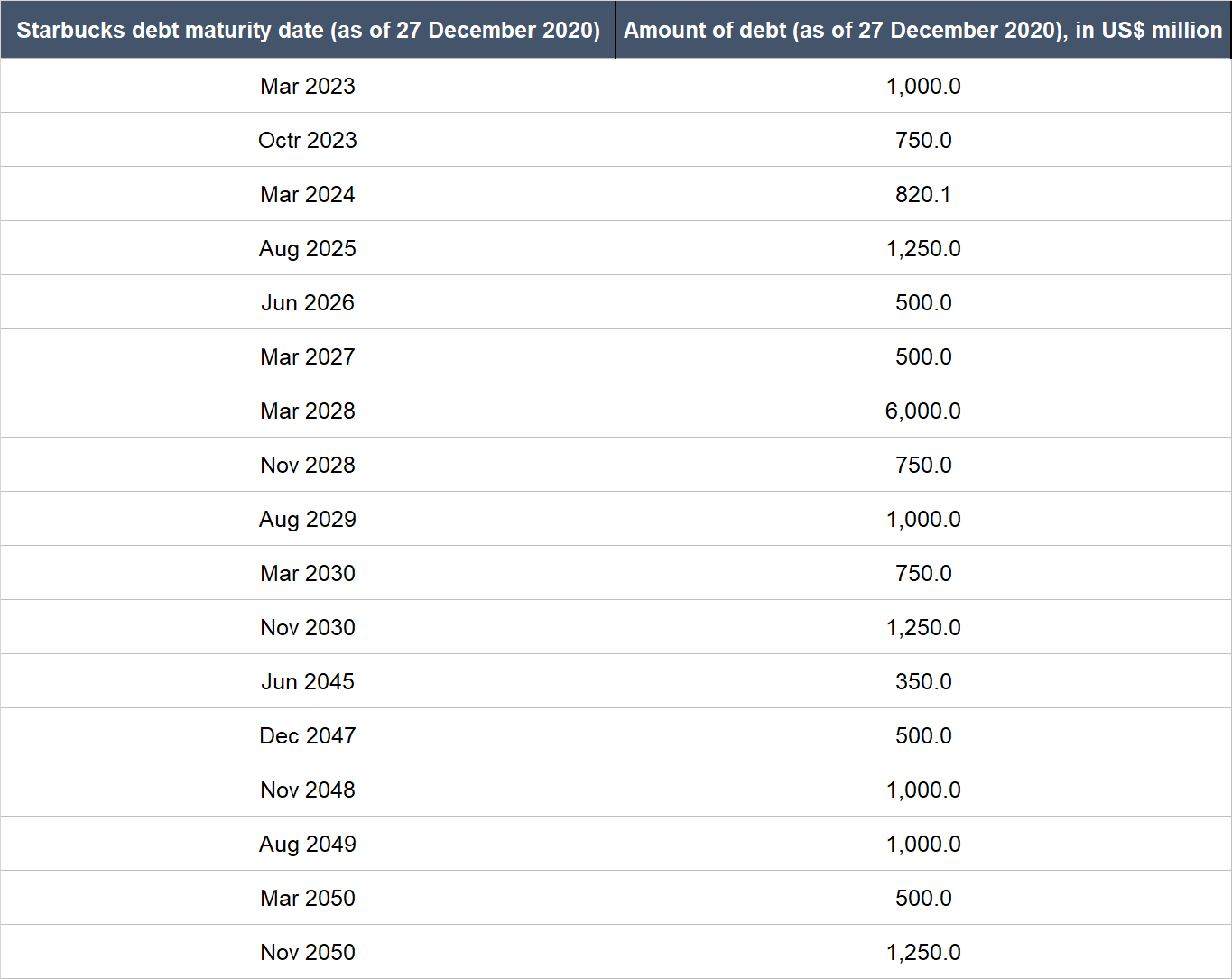

Second, we think short-term liquidity risk is really low for Starbucks. Of its total debt of US$15.92 billion, around 85% (approximately US$13.8 billion) would come due only in March 2023 or beyond. Moreover, these US$13.8 billion in borrowings also have a well-staggered maturity profile as shown in the table below.

Source: Starbucks quarterly earnings update

3. A management team with integrity, capability, and an innovative mindset

On integrity

Starbucks is led by Kevin Johnson, who succeeded the company’s legendary leader, Howard Schultz, as CEO in April 2017. Johnson, who’s 60, has been a Starbucks director since 2009. Prior to being CEO, he was Starbucks’s chief operating officer from March 2015 to April 2017. We appreciate the fact that before Johnson became CEO, he already had around eight years of close contact with Starbucks as a director and then as COO.

In FY2020, Johnson was paid a salary of US$1.54 million, an annual incentive bonus of US$1.86 million, other miscellaneous compensation of US$0.10 million, and stock-awards that have a target value of US$13.5 million. His total pay package thus represents a pretty penny of US$17 million. But importantly, this is a more than reasonable sum when compared to the scale of Starbucks’s business. For perspective, even when faced with severe business disruptions because of COVID-19, Starbucks still managed to post a net profit of US$928.3 million in FY2020. Even more importantly, we think Johnson’s stock-awards are very well-structured. Here are the salient points:

- 40% of the US$13.5 million comes from time-based restricted stock units (RSUs) that vest over four years.

- The remaining 60% comes from performance-based restricted stock units (PRUs). The PRUs depend on Starbucks’s (1) annual earnings per share growth over a three-year period, and (2) total shareholder return – stock price changes, with dividends included – over the same time frame. Depending on Starbucks’s earnings per share performance, the actual PRUs awarded to Johnson could range from 0% to 200% of the target, and this amount could be adjusted up or down (by 25%) based on Starbucks’s total shareholder return.

Putting it all together, an overwhelming majority of Johnson’s total compensation in FY2020 came from stock-awards that depend on Starbucks’s long-term share price performance, which is in turn determined by the company’s long-term business performance. In our view, this aligns Johnson’s interests very well with those of Starbucks’s other shareholders.

And speaking of alignment of interest, Johnson controlled 1.571 million Starbucks shares as of 14 December 2020. At Starbucks’s 28 February 2021 share price of US$108, Johnson’s stake has a value of around US$169.7 million. We think this represents significant skin in the game for Starbucks’s current CEO.

The other senior leaders in Starbucks include:

Source: Starbucks website and regulatory filings

Ruggeri and Lis are very new in their current roles, while Culver is also relatively new. The good thing is that all three of them have decades of collective experience at Starbucks. For us, it’s also a good sign on Starbucks’s culture that it has been promoting from within. It’s worth noting too that all three of them were selected for their current roles after Johnson became CEO.

We don’t know what the compensation structure for Ruggeri and Lis look like since they’re new to their posts. But we’re confident that the structure will be sound, given the following: (1) What we know of Johnson’s remuneration in FY2020; (2) the lion’s share of Culver’s compensation for FY2020 came from stock awards that have the exact same traits as Johnson’s; and (3) the respective predecessors of Ruggeri and Lis – Patrick Grismer and Lucy Helm – were compensated in a similar manner as Culver and Johnson.

On capability and ability to innovate

Kevin Johnson had big shoes to fill when he succeeded Howard Schultz as CEO in April 2017. Even though Scultz is not the founder of Starbucks, he was the key architect of Starbucks’s growth through the ages.

Schultz first joined Starbucks in 1982. Shortly after, he discovered the magic of an espresso in 1983 while at a café in Italy during a work trip. As Schultz puts it, he was “captivated by the beverage, the barista who prepared it and the romance of the café atmosphere.” This gave him the inspiration to create a specialty coffee store in the USA that would provide a comforting “third place between work and home.” But the original founders of Starbucks did not buy into his vision.

Undeterred, Schultz left Starbucks to start his own chain of espresso bars named Il Giornale. In 1987, with three Il Giornales, Schultz returned to Starbucks as CEO in August, after purchasing the company with the help of local investors. He remained CEO until 2000 when he took a step back and became chairman of the company. Starbucks’s business started to decline slowly in the years after Schultz stepped down as CEO. In 2008, Schultz returned to the helm and revived the business. Then in April 2017, Schultz once again relinquished his CEO post to take up the mantle of executive chairman. In June 2018, Schultz officially left Starbucks, holding the title of emeritus chairman.

From the outset of his return to Starbucks in 1987, Schultz wanted to create a special company. From Schultz’s personal website (emphases are ours):

“I never set out to build a global business. I set out to build the kind of company that my father never had a chance to work for. One that treats all people with dignity.

The image of my father immobile on the couch, after his accident, stayed with me. So did the fear of not having healthcare. Not long after he passed away, in 1988, Starbucks became one of the first companies in America to give health insurance to all its employees—including part-time workers, a benefit that was unheard of at the time, especially in retail.

As a kid, I also knew what it felt like not to have money. My parents never owned anything, or had any savings. In 1991, Starbucks became the only company we knew about to give stock ownership to all employees. We called it Bean Stock. Since its inception in 1991—and after Starbucks went public in 1992—Bean Stock has generated more than [US]$1.5 billion in pre-tax gains for the company’s baristas and managers, helping some put down payments on homes, finance cars, pay off loans, even pay for weddings.

We did those two things in the late eighties and early nineties, and never stopped trying to be a different kind of company.

One of my favorite benefits has been the Starbucks College Achievement Plan. In 2014, Starbucks and Arizona State University created the first-of-its kind program to give employees a tuition-free college education. By spring of 2019, more than 3,000 Starbucks partners (employees) will have graduated. Twenty percent of those who have participated in the program are like me, the first in their families to go to college.”

As you’ll see later, in Schultz’s second stint as CEO (2008-2017), Starbucks delivered strong growth while taking good care of its employees, who are affectionately called partners. From FY2007 to FY2017, Starbucks’s revenue grew from US$9.41 billion to US$22.39 billion, profit more than quadrupled to US$2.88 billion, and free cash flow more than 10x-ed to US$2.73 billion.

In our view, Johnson has done an admirable job since he received Schultz’s baton. The things that we think make Starbucks special – the creation of a sense of community in its stores, and the dignified way it supports its partners (again, Starbucks calls its employees partners) – are still well and alive. We want to share three examples.

First, in FY2020, Starbucks granted shares to 211,000 non-executive partners as part of the Bean Stock program that was mentioned in Schultz’s quotes above; US$148 million in pre-tax gains from previously granted Bean Stock awards were also realised by Bean Stock participants during the fiscal year.

Second, Johnson mentioned in Starbucks’s December 2020 Investor Day event that the Starbucks College Achievement Plan, in partnership with Arizona State University, has produced nearly 5,000 graduates, and now has more than 17,000 participants. So nearly 5,000 Starbucks partners have received a college degree for free because of the company’s efforts.

Third, in the same Investor Day event, Johnson called out how Starbucks could help with the social healing process following widespread lockdowns because of COVID-19:

“Now, as we look to the future, it’s important to understand how the recent disruption of the pandemic has accelerated certain changes in consumer behavior and how Starbucks is well-positioned to further differentiate the Starbucks experience and better serve our customers. We believe many of these changes are here to stay and we will continue to adapt our business accordingly to ensure we are meeting our customers how and where they want to engage with Starbucks. Through the relationships we have with our customers around the world, we are focusing on five shifts in consumer behavior to guide us as we adapt in ways that we expect will extend our market leadership position globally.

First, customers will continue to have a fundamental need to be seen and experience a feeling of connection to others, human connection. This feeling has long been the bedrock of community. While deep strong connections can be formed through digital relationships, there is a distinct and natural ease to in-person experiences that are important even among our younger generation of customers. A Starbucks partner saying hello and offering a smile to a customer as they pick up a mobile order that was personally handcrafted just for them. It provides that small but powerful human interaction we all crave. In fact, former US Surgeon General, Vivek Murthy, recently described the pandemic as creating a social recession, supporting our prediction that people will seek out these community connection experiences as a vaccine is distributed. And I believe Starbucks will be a top destination to facilitate social healing through human connection.”

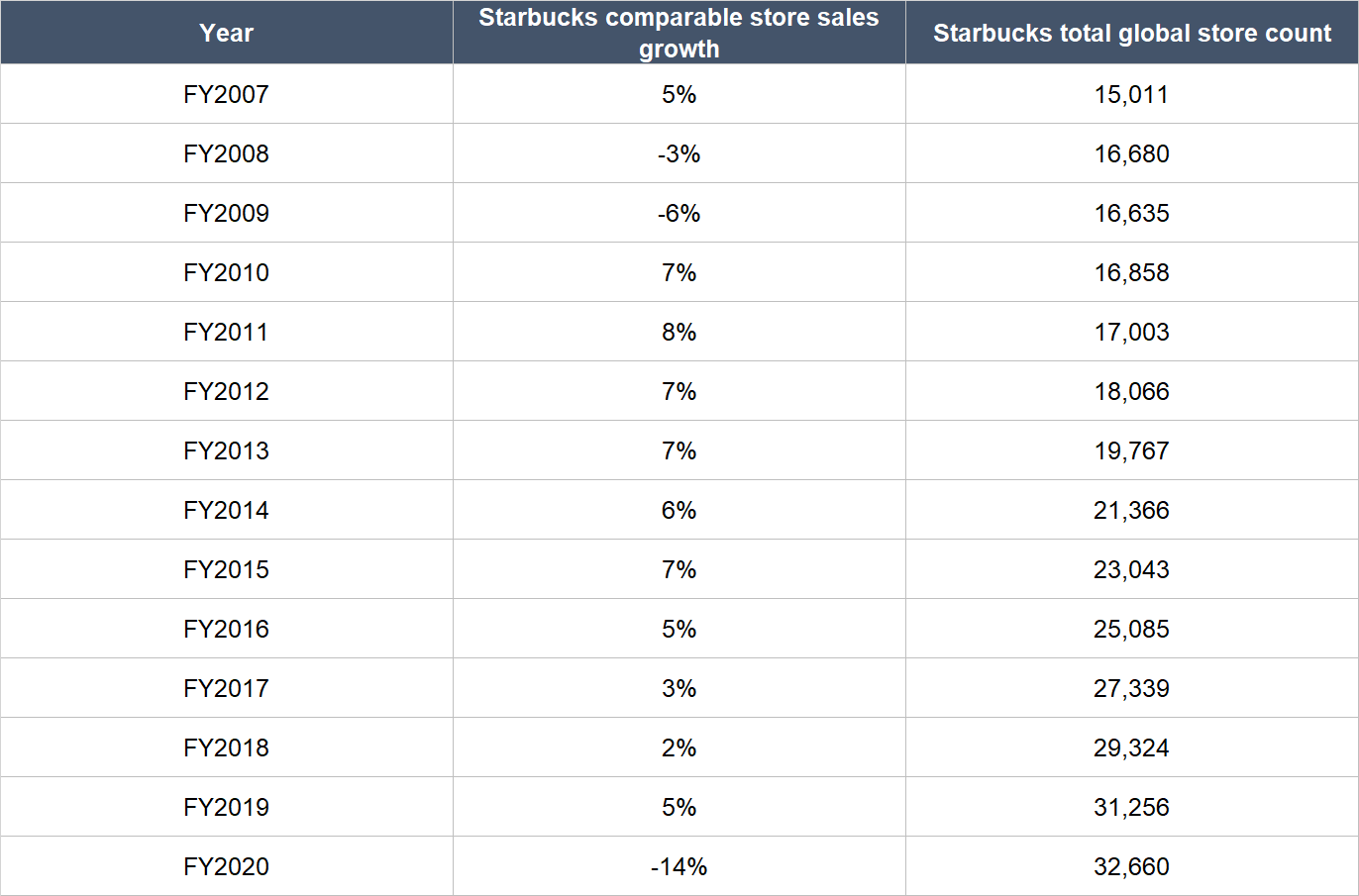

The important business numbers from Starbucks – beyond just the financials – are also a strong indicator that Schultz and Johnson have been excellent leaders of the company. The table below shows the growth in Starbucks’s total global store count (includes both company-operated and licensed stores) for FY2007-FY2020 as well as changes in the company’s comparable store sales growth over the same period. Comparable store sales growth measures the change in period-over-period revenue for Starbucks’s company-operated stores that have been in operation for 13 months or longer as of the reporting period; put simply, it shows how fast the company’s existing stores are growing.

Source: Starbucks annual reports

Starbucks’s global store count had doubled from FY2007 to FY2019 and in those years, comparable store sales growth were positive, except for FY2008 and FY2009. FY2020 was a difficult year for Starbucks because of COVID-19, but it’s not a Starbucks-specific issue – the business was affected because of lockdowns and store closures.

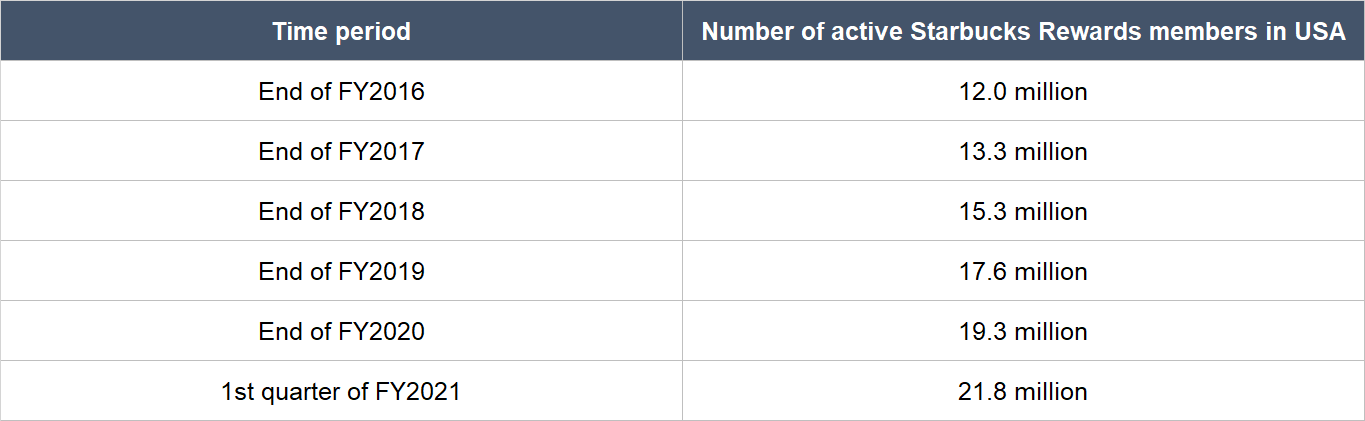

We also see the growth in the number of active US members in Starbucks Rewards (the company’s loyalty programme) as another positive sign on Johnson’s leadership. As the table below shows, active Starbucks Rewards members in the USA have nearly doubled from 12 million at the end of FY2016 to 21.8 million in the first quarter of FY2021. Starbucks Rewards members have historically spent more than non-members, and they accounted for 42% and 47% of Starbucks’s revenue in the USA in the fourth quarters of FY2019 and FY2020, respectively. Starbucks Rewards members make up a strong foundation of highly loyal customers for the company, and we think Starbucks’s business strengthens as the membership base grows.

Source: Starbucks quarterly earnings updates

We’re also impressed by what Johnson and his team have done since the outbreak of COVID-19. Some examples:

- In May 2020, Starbucks started transforming the format of the company’s portfolio of stores in the USA, with an emphasis on expanding curbside delivery and pickup. By the fourth quarter of 2021, Starbucks would have launched curbside pickup in “several hundred existing locations” and add more than 50 Starbucks Pickup locations.

- Starbucks continued its quest to protect the environment and the community through a few ways: (1) It launched plant-based meat products in its stores in June 2020; (2) in support of its commitment toward 100% ethically sourced coffee, Starbucks announced a new initiative in the fourth quarter of FY2020 – the Starbucks Digital Traceability tool – that can track the movement of coffee beans from farm to stores; and (3) the company joined the “Transform to Net Zero” initiative as a founding member, also in the fourth quarter of FY2020, to accelerate the transition to a net-zero emissions global economy no later than 2050.

- Starbucks opened 581 net new stores in China in FY2020, a record high for store openings in the country. In all, Starbucks’s total capital expenditure in FY2020 was US$1.48 billion, not far from the US$1.81 billion seen in FY2019.

- Starbucks announced in March 2020 that it would invest US$130 million to develop a state-of-the-art coffee roasting facility in China. Named Coffee Innovation Park (CIP), the facility is Starbucks’s first coffee manufacturing investment in Asia. In November 2020, Starbucks announced that construction for CIP had begun and that it would be raising its investment to US$150 million.

We think it’s not an easy feat for Johnson and his team to focus on improving the consumer experience, protecting suppliers and the environment, and investing for the future – all of which delivers value to Starbucks, but likely only in the long-term – while having to combat a shorter-term threat such as COVID-19.

Earlier, we discussed why we think China is an attractive growth opportunity for Starbucks. But we also want to highlight that it’s incredibly difficult to succeed as a coffee store in the country. Here are the relevant excerpts on the topic from a July 2020 Reuters article:

“This year’s admission by delivery-focused and coupon-reliant Luckin Coffee that it fabricated [US]$310 million in sales underscores how the coffee opportunity in China has been exaggerated, analysts said.

“Luckin’s fraud proved that even though coffee in China is almost free, the Chinese still don’t drink much of it,” said Beijing-based independent analyst Keso Hong…

…Like Luckin, other domestic chains are struggling to fulfil big dreams.

Coffee Box, which focuses on coffee deliveries and raised some [US]$56 million in funding, has shut or suspended business at dozens of its stores. Grey Box, which offers speciality coffee, said in 2018 it wanted 12 stores in Beijing by end of that year, but has just four. Bruno Caffe has closed most stores and only two remain.

Among western firms, Britain’s Costa Coffee, which is owned by Coca-Cola, has 300 China stores according to its website, despite earlier ambitions to have had 2,500 by 2018.”

But yet, Starbucks has done well in China. The same Reuters article said that “Starbucks, the first big Western brand in the market and now with 20 years in China under its belt, appears to be the only resounding success, having carefully cultivated its image as a premium cafe for young professionals.” We credit Schultz and Johnson for Starbuck’s success in the country.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We believe that a large percentage of Starbucks revenue is highly recurring due to customer behaviour. There are two angles to our belief.

First, coffee is a consumable product, so customers who need their caffeine fix regularly will have to constantly purchase Starbucks’s products. But selling a consumable product alone isn’t enough – the customer’s experience when purchasing and consuming the product needs to be great, or the customer won’t return. This brings us to the second angle: We think that Starbucks has a great brand that consumers love to return to. In Starbucks’s FY2020 annual report, management wrote:

“The Starbucks Experience is built upon superior customer service and a seamless digital experience as well as clean and well- maintained stores that reflect the personalities of the communities in which they operate, thereby building a high degree of customer loyalty.”

This is language that has been found in Starbucks’s annual reports going back to at least a decade. In our opinion, the company’s numbers do reflect the presence of a special Starbucks Experience. Earlier, we shared two things: (1) Starbucks has a long history of positive comparable store sales growth; and (2) the number of active US members in Starbucks Rewards (the company’s loyalty programme) has nearly doubled from 12 million at the end of FY2016 to 21.8 million in the first quarter of FY2021

All these said, it’s worth noting that consumers’ willingness to spend at Starubcks’s outlets can still be affected somewhat by broader economic conditions. We saw this happen in FY2008 and FY2009, the years of the Great Financial Crisis, when comparable store sales growth became negative because of declines in consumer traffic. FY2020 was also a difficult year for Starbucks – traffic fell by 22%, leading to a 14% plunge in comparable store sales. COVID-19-related lockdowns on human movement around the world led to store closures for Starbucks and lesser traffic.

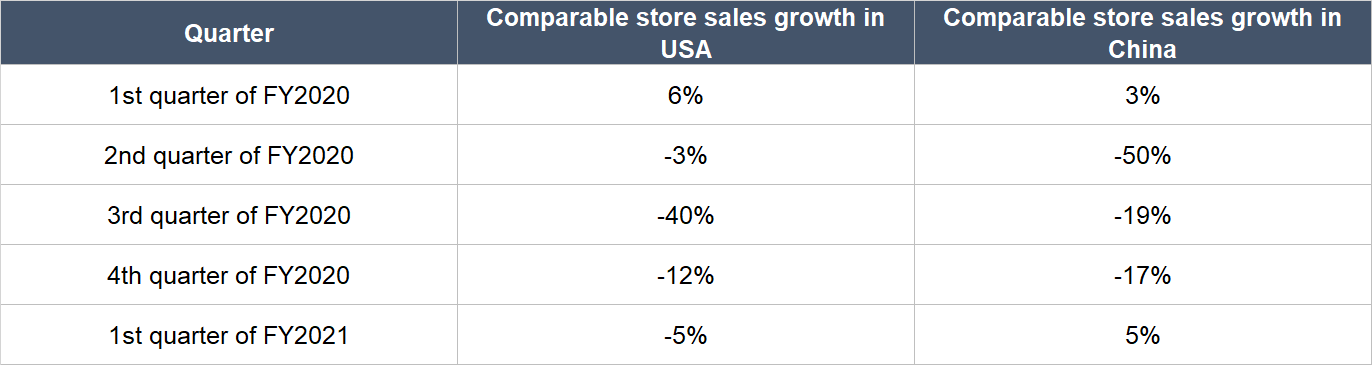

The good thing is that business conditions improved for Starbucks as FY2020 progressed. The table below shows the comparable store sales growth for Starbucks in the USA and China for each quarter of FY2020 and the first quarter of FY2021, and it’s clear that the declines in the metric have been improving. In fact, for the whole of FY2021, Starbucks expects to achieve comparable store sales growth of between 17% and 22% for the USA, and between 27% and 32% for China.

Source: Starbucks quarterly earnings updates

So ultimately, we see COVID-19 as merely a short-term roadblock for Starbucks and our eyes are on the longer-term opportunity for the company. And just to be clear, we think that Starbucks has strong recurring revenue over the long run.

5. A proven ability to grow

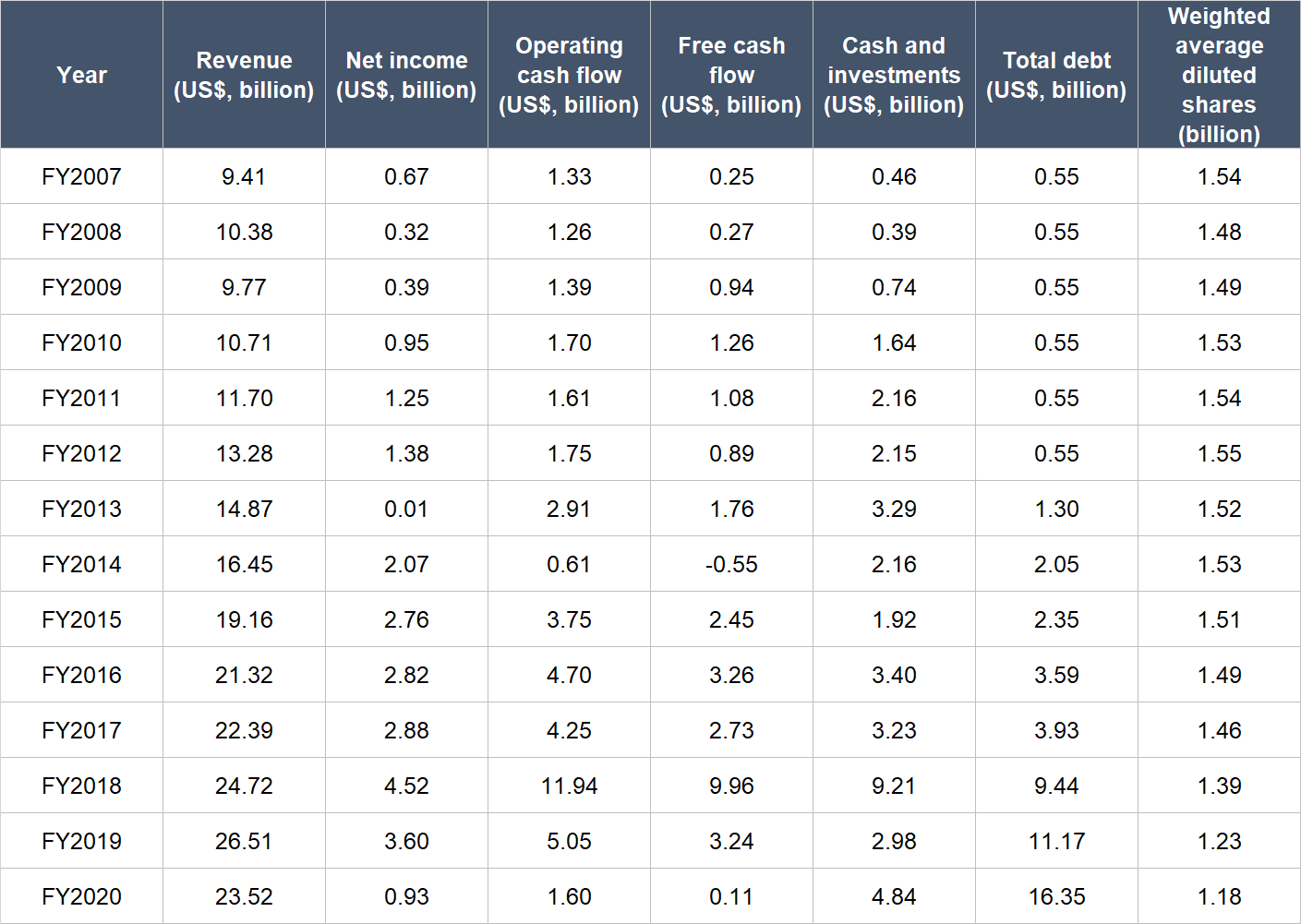

The table below shows Starbucks’s important financials from FY2007 to FY2020 (we chose FY2007 as the starting point to observe how the company fared during the Great Financial Crisis period):

Source: Starbucks annual reports

Here are the important things to note about Starbucks’s historical financials:

- Revenue compounded at a decent clip of 9.0% annually from FY2007 to FY2019; the growth rate remained respectable at 8.5% per year for FY2015-FY2019.

- Net income was positive throughout FY2007-FY2019, and increased by 15.0% per year in that period. The annualised growth rate slowed in the FY2015-FY2019 period, but was still decent at 6.9%.

- The huge fall in Starbucks’s net income in FY2013 was mostly due to a US$2.78 billion legal charge that is associated with a legal dispute the company had with Kraft.

- Starbucks was consistently generating positive operating cash flow and free cash flow for the FY2007-FY2019 timeframe, and both financial numbers also displayed a clear upward trend. Operating cash flow and free cash flow increased by 11.7% and 23.8% per year, respectively, from FY2007 to FY2019; for the FY2015-FY2019 period, the annual growth rates were 7.7% and 7.3%.

- The sharp fall in Starbucks’s operating cash flow – and hence free cash flow – in FY2014 came from the payment of the aforementioned US$2.78 billion legal charge that was booked in FY2013. There was a massive spike in Starbucks’s operating cash flow – and again, hence free cash flow – in FY2018. This was the result of the US$7 billion up-front payment from Nestlé for the Global Coffee Alliance that was mentioned earlier.

- Starbucks’s balance sheet had been reasonably strong from FY2007 to FY2018, with cash and investments being either higher or slightly lower than debt. The picture changed in FY2019 with Starbucks’s debt becoming much higher than its cash and investments. A big reason is because Starbucks spent US$7.13 billion and US$10.22 billion in FY2018 and FY2019, respectively, on share buybacks. Earlier, we discussed why we’re not worried about Starbucks’s heavy debt load.

- Dilution was never a problem for Starbucks. Its weighted average diluted share count inched up by only 0.1% per year from FY2007 to FY2012, before falling by 3.3% annually from FY2012 to FY2020. The lower share count has helped to boost Starbucks’s per share growth rates. For example, the company’s free cash flow per share climbed by 12.9% per year from FY2015 to FY2019, compared to the 7.3% annual increase seen in free cash flow for the same period. In another instance, diluted earnings per share grew by 12.5% annually for the same period, compared to the 6.9% increase seen in net income.

- In FY2020, COVID-19 became a pandemic and it affected Starbucks’s results. Revenue, net income, operating cash flow, and free cash flow all fell. But the good thing is the company was still profitable and generated positive operating cash flow and free cash flow.

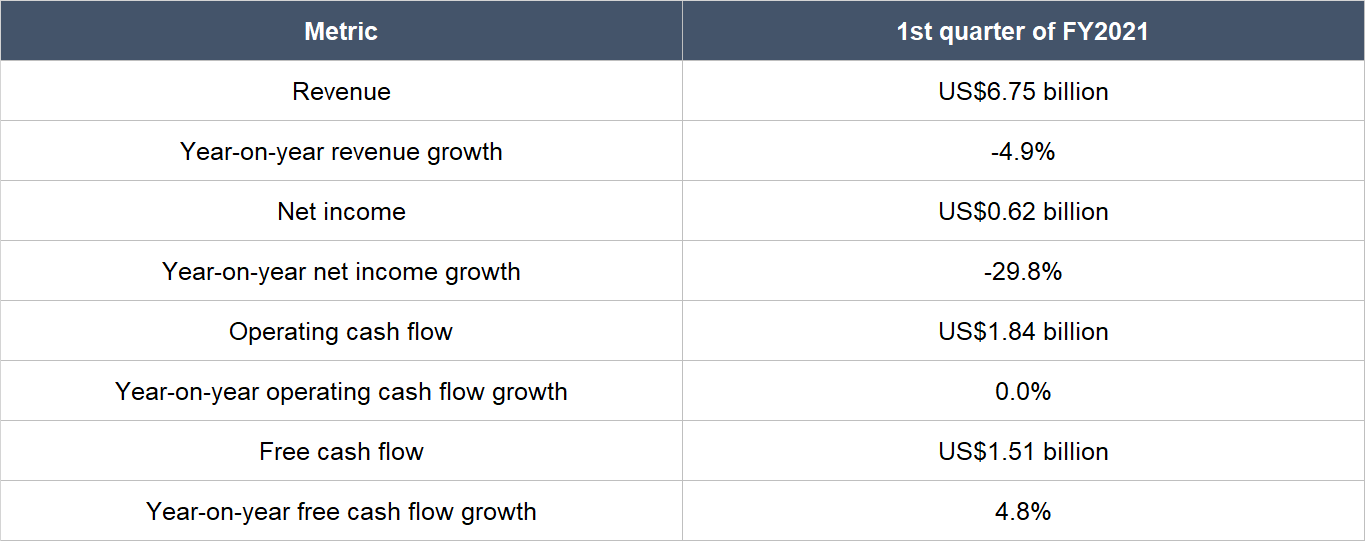

The table below shows the year-on-year changes in Starbucks’s revenue, net income, operating cash flow, and free cash flow in the first quarter of FY2021. During the quarter, Starbucks continued to feel the negative impacts of COVID-19 on its business – revenue and net income both fell (one of them sharply), and operating cash flow was flat. But there’s light at the end of the tunnel. For the whole of FY2021, Starbucks expects to post strong comparable store sales growth, as mentioned earlier. The company also expects (1) revenue of between US$28.0 billion and US$29.0 billion for the year, up 21.2% from FY2020 at the midpoint, and (2) diluted earnings per share of between US$2.42 and U$2.62, up by more than 120% from FY2020, again at the midpoint.

Source: Starbucks quarterly earnings update

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are three reasons why we think Starbucks excels in this criterion.

First, there’s still significant room to grow for Starbucks. Its total revenue at the moment – which includes the sale of food items and beverages beyond coffee – is low when compared to only the global coffee market.

Second, we shared earlier why we think Starbucks has a loyal and growing customer base that gives it a strong foundation of highly recurring revenues.

Third, Starbucks has excelled at generating free cash flow for a long time. Prior to the onset of COVID-19, the company’s average free cash flow margin from FY2015 to FY2019 (excluding FY2018 because of the abnormal spike in operating cash flow and free cash flow that occurred during the year) was a respectable 13.1%. And even in the face of COVID-19 in FY2020, Starbucks still produced positive free cash flow.

Valuation

We like to keep things simple in the valuation process. In Starbucks’s case, we think the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value. This is because Starbucks has been adept at producing positive and growing profit as well as free cash flow for a long period of time.

We completed our purchases of Starbucks shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$77 per Starbucks share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios that were around 67 and -200, respectively. The P/E ratio looked really high while the P/FCF ratio had no useful signal since it was negative.

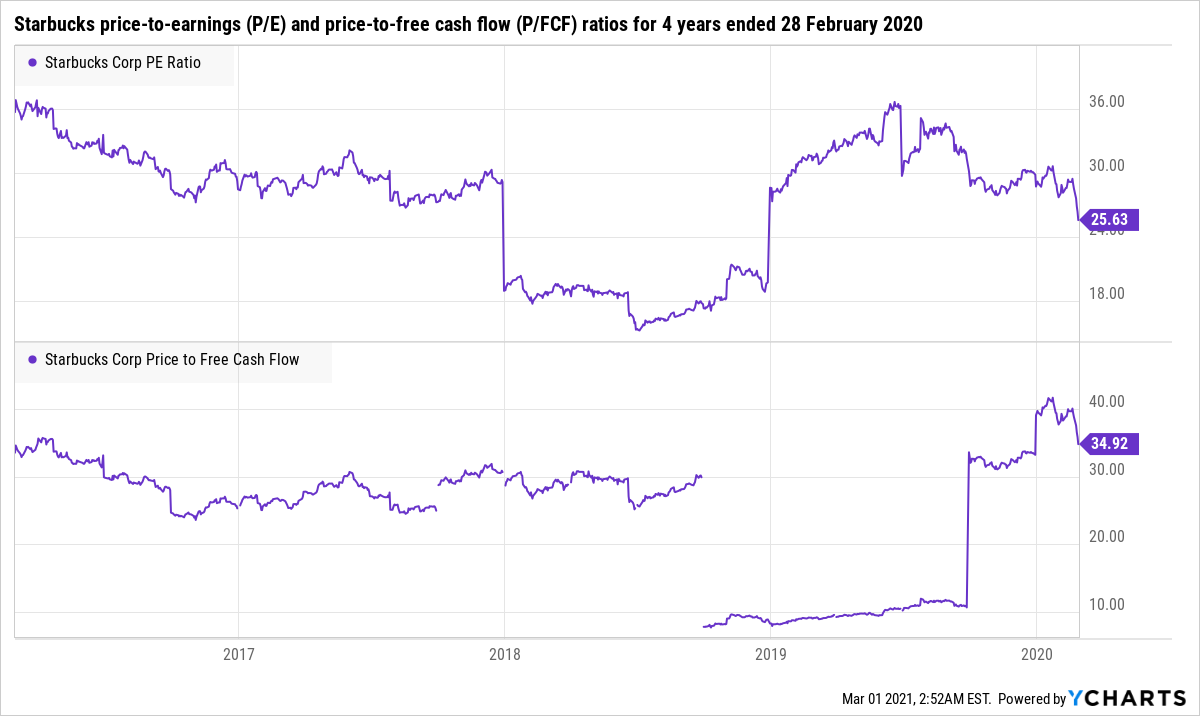

But there’s an important thing to keep in mind: Starbucks’s business was affected by COVID-19 in that period, which depressed its net income and free cash flow. If we used Starbucks’s financial numbers for FY2019, our average purchase price would represent P/E and P/FCF ratios of around 26 and 29, respectively. These adjusted valuation ratios are not high in relation to their own histories. The chart below shows that Starbucks’s P/E and P/FCF ratios over the four years ended 28 February 2020 were mostly hovering in the 30s range (we used an end-point of 28 February 2020 to remove the impact of COVID-19).

We think it’s very likely that Starbucks could grow its revenue in a steady fashion in the high single-digit to low double-digit percentage range on an annual basis in the years ahead. With stable or slightly better margins over time, plus the effects of share buybacks, Starbucks’s earnings per share and free cash flow per share could both easily achieve annual growth rates that are in the low-teens to mid-teens percentage range. For the growth profile in Starbucks’s business, we think that the valuation ratios at which our investment was made – adjusted P/E and P/FCF ratios in the high-20s – are highly reasonable.

For perspective, Starbucks carried trailing P/E and P/FCF ratios of around 190 and 690, respectively, at the 28 February 2021 share price of US$108. If we apply the US$108 share price to Starbucks’s FY2019 financial numbers, we end up with an adjusted P/E ratio of around 37, and an adjusted P/FCF ratio of around 41.

The risks involved

The biggest threat to our Starbucks investment that we see is the risk of an extended period of severe restrictions on human movement in the future to combat COVID-19. Store closures and lockdowns have already cost Starbucks steep declines in revenue in FY2020, leading to even more painful falls in net income and free cash flow. The good thing is that, as discussed earlier, Starbucks sees a solid rebound in its business fortunes in FY2021. But the picture could turn dark quickly if the virus flares up again.

This risk is exacerbated by the fact that Starbucks’s balance sheet currently has way more debt than cash. A prolonged period of low or negative free cash flow could place Starbucks in a difficult liquidity position. The company is nowhere near that danger zone yet, but we’re keeping an eye on things.

Further to this point, an environment of higher interest rates in the future could cause financial difficulties for Starbucks because of its high debt load. For instance, refinancing of maturing debt could be tough in the future if it has to be done when interest rates are high. Thankfully, Starbucks has a well-distributed debt-maturity profile, as discussed earlier. The company also enjoys, in our opinion, high levels of recurring revenues, which helps to lower the risk of it running into financial difficulties.

The current political tension between the USA and China is also another risk for Starbucks. China is one of Starbucks’s major growth markets, but it’s an American company. If the quarrels between the USA and China were to heat up in the future, Starbucks could be caught in the cross-hairs.

Summary and allocation commentary

To sum up Starbucks, it has:

- A large coffee market to grow into, and also the possibility of capturing a good slice of the restaurant and tea markets

- A balance sheet with significantly more debt than cash and investments, but the company has high levels of recurring revenues, thereby lowering the risk of a weak balance sheet

- A management team with (1) incentives that are well-aligned with Starbucks’s shareholders, (2) years of experience at the company, and (3) a strong track record of execution and growth in recent years

- High levels of recurring revenues from customer behaviour

- A long-term history of respectable growth in revenue, net income, operating cash flow, and free cash flow, excluding COVID-19

- A high likelihood of being able to generate a strong and growing stream of free cash flow in the future.

The key risks we’ve identified with Starbucks include the possibility of extended lockdowns in the future to curb COVID-19, and financial risks stemming from the company’s high debt load.

After weighing the pros and cons, we initiated a 2.0% position in Starbucks – a medium-sized allocation – with Compounder Fund’s capital. We think Starbucks offers a cool combination of having a large market opportunity and a high probability of being able to grow at a decent clip over the long run. But our enthusiasm is tempered by our awareness that Starbucks’s historical growth rates are not the fastest, and that the company’s business is currently hampered by COVID-19. So we think a medium-sized allocation is the sensible approach.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Compounder Fund does not own shares in any other companies mentioned. Holdings are subject to change at any time.