Compounder Fund: Portfolio Update (April 2021) - 13 Apr 2021

Jeremy and I intend to share frequent but non-scheduled updates on how Compounder Fund’s portfolio looks like. The last time we shared an update on this was for Compounder Fund’s portfolio in mid-January 2021.

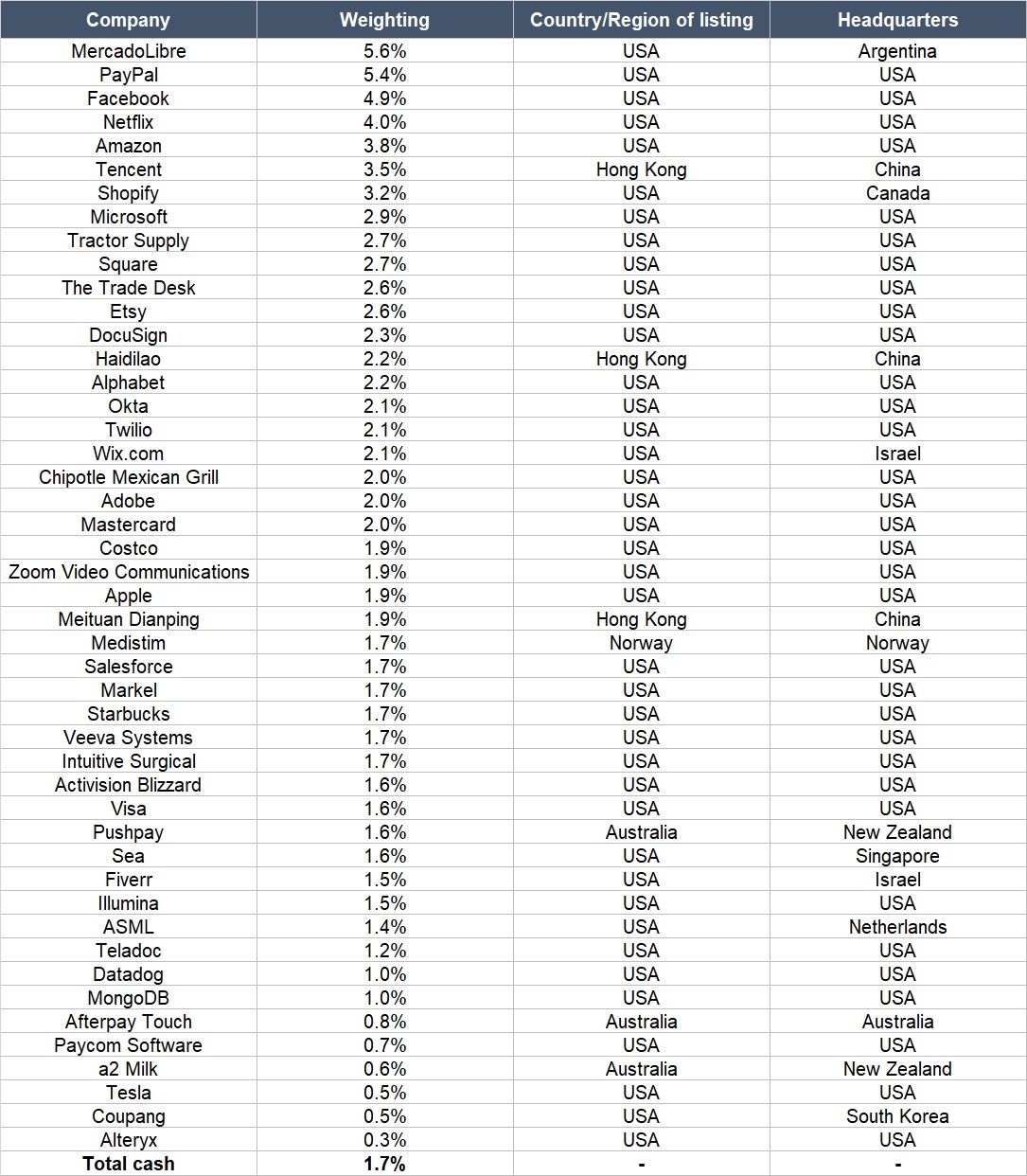

In it, I shared all 43 holdings in the fund’s portfolio. As of the date of this article, the portfolio contains the same 43 holdings, plus the addition of four new stocks.

As you know, Compounder Fund is able to accept new subscriptions once every quarter with a dealing date that falls on the first business day of each calendar quarter. In the middle of March 2021, Jeremy and I successfully closed Compounder Fund’s third subscription window since its initial offering period (which ended on 13 July 2020).

This new capital was deployed quickly in the days after the last subscription window’s dealing date of 1 April 2021. Jeremy and I invested the new capital across 13 of Compounder Fund’s existing holdings. They are (in alphabetical order): Adobe, Costco, DataDog, DocuSign, Facebook, Fiverr, Mastercard, MongoDB, Netflix, Shopify, Tesla, Twilio, and Zoom. The four new companies that we invested in are ASML, Coupang, Etsy, and Sea Limited. A few quick words on the new companies in the portfolio:

- ASML provides lithography machines and other related systems to manufacturers of integrated circuits, or chips. Lithography is the process of using light to create tiny, tiny structures (called transistors) on a silicon wafer to produce chips. What’s unique about ASML is that it is the only company in the world with the technological knowhow to manufacture EUV (extreme ultraviolet) lithography machines. EUV lithography is currently the most advanced lithography process and it uses ultraviolet light of an extremely short wavelength of 13.5 nm. In a world that is increasingly going digital, there is a need for a chip to contain more and more transistors because this improves a chip’s cost and performance. This is where EUV lithography machines shine. Because they use light with such a short wavelength, they allow chip manufacturers to produce chips with transistors that have mind bogglingly small sizes. How small? Some of ASML’s customers are already working on producing chips with 3 nm and even 2 nm nodes. (For perspective, a sheet of paper is about 100,000 nm thick.) We’re attracted to ASML because of the importance of its products in powering the growth of the semiconductor industry, which itself is an indispensable part of our everyday lives (just think about living in a world without electronics and the internet!). It helps too that ASML has a strong financial profile: Revenue increased by 17.3% annually from €6.3 billion in 2015 to €14.0 billion in 2020; meanwhile the average free cash flow margin (free cash flow as a percentage of revenue) for the same period was 21.8%.

- “To create a world where customers wonder: “How did I ever live without Coupang?”” is the audacious mission statement of the South Korea-based Coupang, one of the most customer-centric companies in the word we’ve studied. (Its name comes from a mishmash of the words “coupon” and “pang”, the Korean word for hitting the jackpot.) The company is the largest e-commerce player in South Korea – it operates only in the country – with revenue of US$12.0 billion in 2020. Founded in 2010, Coupang has poured billions of dollars since 2013 into its technology and fulfillment infrastructure to provide superior customer experiences. The results so far? Coupang can boast of the largest logistics footprint among 1st-party ecommerce companies in South Korea. At the end of 2020, the company’s fulfillment and logistics centres (more than 100 of them across 30 cities) covered 2.3 million square metres, placing 70% of the South Korean population within 11 km of a Coupang logistics facility. Coupang’s dense logistics network – together with its 15,000 directly-employed full time drivers – allow the company to provide the following services: Dawn delivery (delivery before 7am if ordered before midnight); same-day delivery (delivery in the same day if ordered in the morning); free, one-day delivery nationwide, 365 days a year; boxless packaging; and frictionless returns (customers simply tap a button on Coupang’s app and leave the item outside their door for pickup). Coupang has compounded its revenue impressively by 63.5% per year from 2016 to 2020 and more growth is likely to be ahead. South Korea’s the 12th largest economy in the world (as of 2019) and the country’s total retail, grocery, consumer foodservice, and travel spend is expected to increase from US$470 billion in 2019 to US$534 billion in 2020.

- Etsy’s mission is to “Keep Commerce Human” and true to form, it operates an ecommerce platform that connects creators of unique handcrafted goods with buyers looking for such products. A recent survey of Etsy buyers found that 88% agreed that Etsy has items that can’t be found anywhere else. The company’s revenue growth was already rapid even before COVID-19 (a 33% compound annual growth rate from 2014 to 2019), and accelerated to 111% in 2020. Etsy has also amassed a huge, growing, and global network of active buyers (81.9 million in 2020) and sellers (4.4 million in 2020). If the company remains true to its unique mission statement, we think its network effect – of more buyers leading to more sellers, which leads to more buyers, and so on – will grow stronger and become increasingly difficult to break over time. And impressively, Etsy ended 2020 with free cash flow of US$671 million, representing a free cash flow margin of 39%, up from an already solid 23% in 2019.

- Sea Limited is based in Singapore but counts itself as a global computer gaming giant (Garena) and Southeast Asia’s leading e-commerce platform (Shopee). Garena ended 2020 with 73.1 million paying users, up 120% from end-2019 and up a staggering 514% from end-2018. Shopee’s GMV (gross merchandise value) experienced similarly strong growth of 247% from US$3.4 billion in 2018 to US$11.9 billion in 2020. Sea also has a fast-growing digital payments arm called Sea Money. The digital payments and ecommerce opportunities for Sea look exciting to us (ecommerce still makes up only a small percentage of total retail sales in Southeast Asia), especially when the company has the highly-profitable – and growing – Garena churning out cash to support any growth investments.

In Compounder Fund’s Owner’s Manual, we mentioned that “if Compounder Fund receives new capital from investors, our preference when deploying the capital is to add to our winners and/or invest in new ideas.” Not all of the 13 existing holdings in Compounder Fund’s portfolio that we added capital to have seen their stock prices rise strongly after we initially invested in them. But all of them have executed brilliantly in recent times and produced wonderful results (the only exception was Mastercard, where revenue growth in the last reported quarter was negative). They are winners, according to our definition. The four new stocks we invested in have also produced excellent results. Here’s how Compounder Fund’s portfolio looks like as of 9 April 2021:

The biggest addition to our existing holdings was Facebook. We added to our position in the company despite Apple’s much-publicised change to the privacy policy for its IDFA (Identifier for Advertisers). Without going into detail (see here for more), Apple’s new upcoming policy will require apps to get users’ permission to track their data across apps or websites owned by other companies. Here’s a March 2021 CNBC article on how Apple’s move could hurt Facebook’s advertising business:

“Most critically at stake for Facebook is what’s known as view-through conversions. This metric is used by ad-tech companies to measure how many users saw an ad, did not immediately click on it, but later made a purchase related to that ad.

Think of view-through conversions like this: You’re tapping through your Instagram stories and you see an ad for a pair of jeans. You don’t tap the bottom of the ad for more information because you’re busy checking out what your friends are up to, but the jeans were cute. A few days later, you go on Google, search for the jeans you saw on Instagram and buy them.

After the purchase is made, the retailer records the IDFA of the user who bought the jeans and shares it with Facebook, which can determine whether the IDFA matches with a user who saw an ad for the jeans. This shows the retailer that their Facebook ad worked.

Losing that type of measurement could be a big blow for Facebook. If advertisers are unable to accurately measure the effectiveness of their Facebook and Instagram ads, they may feel compelled to shift more of their budgets to other apps and services where they can see the exact return on investment for their ads…

…In terms of specific businesses, the IDFA change will particularly hurt its Audience Network.

The Facebook Audience Network provides advertisements in non-Facebook apps, and it uses IDFA numbers to determine the best ads to show to each user based on Facebook’s data. For instance, a soft drink maker could decide to target 18-to-34-year-old gamers in the San Francisco Bay Area with a new promotion. The company could use the Facebook Audience network to have those ads placed before the right audience within mobile games; Facebook would split the ad revenue with the game makers.

But if users opt out of IDFA tracking, all of that personalization Facebook has built will be rendered irrelevant outside of the company’s own apps. In August, Facebook acknowledged that Apple’s upcoming iOS 14 could lead to a more than 50% drop in its Audience Network advertising business.

Nearly all of Facebook’s revenue comes from advertising, but Facebook’s Audience Network contributes only a small portion of that — well less than 10% of the company’s net revenue, a person familiar with the numbers told CNBC.

Besides view-through conversions, Facebook may lose valuable data about what its iPhone-based users do on their devices when they’re not in Facebook-owned apps. Already, Facebook collects a lot of data about its users from its apps, which include Facebook, Instagram, Messenger, WhatsApp and others, but every additional bit of data makes its algorithms better at what they do, which includes ad targeting.”

In short, changes to the IDFA would make it difficult for Facebook to know the shopping behaviour of Facebook users outside of the company’s own platforms. This would diminish the value of Facebook’s digital advertising services. But the company has not been lying still. It has been actively encouraging commerce activities to take place directly on its own platforms and one such initiative is the launch of Facebook Shops in 2020. Last month, during a Clubhouse session with Josh Constine, Facebook’s CEO and co-founder, Mark Zuckerberg, revealed that Facebook Shops now has more than 1 million active stores and 250 million active users. During the same Clubhouse session, Zuckerberg also shared how Facebook could emerge from Apple’s IDFA issue even stronger than before:

“When it comes to the iOS 14 changes [for IDFA], for example, and their impact on our business, I think the reality is that I’m confident that we’re gonna be able to manage through that situation. And we’ll be in a good position. I think it’s possible that we may even be in a stronger position. If Apple’s changes encourage more businesses to conduct commerce on our platforms, by making it harder for them to basically use their data in order to find the customers that would want to use their products outside of our platforms.”

There are three other reasons for our decision to add to Facebook.

First, the company grew revenue by an impressive 33.2% in the fourth quarter of 2020 while improving its free cash flow margin from an already strong 21.5% a year ago to 33.6%. It’s worth noting too that Facebook spent US$4.6 billion on capital expenditures during the quarter, up 12.5% from a year ago.

Second, the chance of Facebook creating a massive business in the AR/VR (augmented reality and virtual reality) space now looks higher to us than before. Last month, The Verge reported that Facebook has nearly 10,000 employees – around 15% of its total headcount of 58,604 at the end of 2020 – working on AR/VR technology. For perspective, this is a significant increase from 2017, when Facebook had more than 1,000 AR/VR employees, which was around 5% of its total workforce then.

Third, Facebook’s shares had a trailing price-to-free cash flow ratio of 37 at the end of March 2021. We think this is an undemanding valuation for a company that (1) could compound its revenue at north of 20% annually over the next five years, (2) fetched an excellent free cash flow margin of 27% in 2020, and (3) has a fortress of a balance sheet with zero debt and nearly US$62 billion in cash and investments.

We’re sharing all this information with the public and with the fund’s investors for two reasons. First, we believe deeply in investor education and want Compounder Fund’s return and actions to be a source for people to learn about investing. Second, we believe that this transparency will help investors of Compounder Fund develop comfort with our investing process over time, which is great; in turn, this will also free us from the time-consuming activity of dealing with questions on how we invest, and thus give us more to invest better for our investors.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Holdings are subject to change at any time.