Compounder Fund: Paycom Software Investment Thesis - 06 Feb 2021

Data as of 1 February 2021

Paycom Software (NASDAQ: PAYC), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Paycom is one of the leading providers of a cloud-based HCM (human capital management) software solution. The company’s software runs on a single-database, an approach that solves a big pain point for the human resource departments of many companies – with Paycom, there’s no need to integrate and replicate human resource-related data among different service providers and this saves companies time and money.

There are many different software applications offered by Paycom (over 30 at the end of 2019) that fall under the following broad categories: talent acquisition; time and labour management; payroll; talent management; and HR management. But the most important application would be Payroll and Tax Management, which comes under the payroll category. All of Paycom’s clients are required to use this application in order to access the company’s other services.

Paycom earned US$620.5 million in revenue in the first nine months of 2020 and the majority of it likely came from payroll processing (it was the case in 2019). The company currently does not do business outside of the USA.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Paycom.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

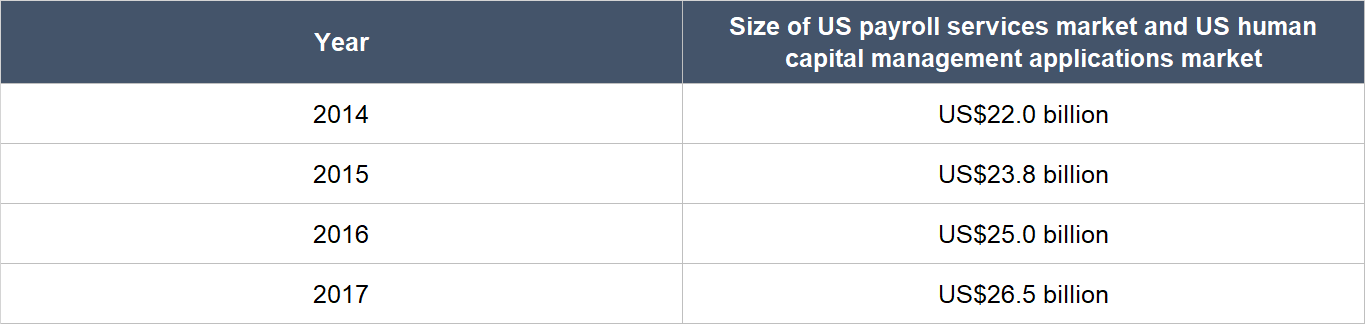

According to estimates from International Data Corporation, the size of the US payroll services market and US HCM applications market (excluding payroll and expense management services) was US$8.8 billion and US$17.7 billion, respectively, in 2017. These numbers add up to US$26.5 billion and it is significantly larger than Paycom’s revenue of US$813.9 million in the 12 months ended 30 September 2020.

We don’t have more recent data for Paycom’s addressable market, but we think it’s reasonable to conclude that it has been stable or growing slowly since 2017. The table below shows the growth in Paycom’s market for 2014-2017, based on data from International Data Corporation:

Source: Paycom annual reports (based on estimates from International Data Corporation)

We believe that Paycom has a good chance of significantly increasing its market penetration in the USA in the years ahead. Here are a few reasons why:

- The company has an excellent track record of growth, which we will discuss in more detail later.

- The company has plenty of room to increase its geographical footprint, even in the USA alone. At the end of 2019, Paycom had offices in only 38 of the 50 largest metropolitan statistical areas (MSAs) in the country, and only five of these areas were served by multiple Paycom sales teams. Paycom has plans to expand its sales operations in its existing markets, and to open new sales offices in other MSAs where it does not have sales teams yet.

- Paycom used to focus on small and medium businesses (SMBs) that have 50 to 2,000 employees, although it also had much larger clients. In recent years, it began targeting larger businesses and its average client-size grew significantly as a result. Now, Paycom’s target client is a company with 50 to 5,000 employees. The great thing here is that Paycom did not have to make any changes to its software solutions to serve larger clients.

- Paycom has posted robust client-retention metrics for a long time and we will share more about this later.

- We think the software tools provided by Paycom help solve important pain points that many companies experience.

As we mentioned earlier, Paycom has only one geographical market currently, and that is the USA. It’s reasonable to assume that the global addressable markets (excluding the USA) for payroll services and HCM applications are, at the very least, similar in size to the US analogues – after all, the USA accounted for only 24% of global gross domestic product in 2018. This means that there is a huge international opportunity for Paycom to capture, should it decide one day to expand its reach beyond its home country.

2. A strong balance sheet with minimal or a reasonable amount of debt

As of 30 September 2020, Paycom’s balance sheet held US$156.4 million in cash and investments, and just US$31.3 million in total debt. This is a strong balance sheet in our view.

It also helps that Paycom has been generating positive and growing free cash flow since 2014. More on this later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Paycom is led by its 49-year old founder Chad Richison, who has served as the company’s president and CEO since its founding in 1998. We appreciate the fact that Richison is relatively young, but already has more than two decades of experience leading the company. Paycom’s management bench also includes other experienced leaders. For instance, Craig Bolte, 56, has been Paycom’s chief financial officer since February 2006 while the 52 year-old Jeffrey York has served as Paycom’s chief sales officer since 2007.

In 2019, Richison’s total compensation was US$21.1 million. This is a princely sum and looks even more so when compared to the scale of Paycom’s business (net profit and free cash flow for the year were US$180.6 million and US$131.3 million, respectively). And although more than 87% of Richison’s total compensation of US$21.1 million (works out to US$18.4 million) came from stock-related awards, we think they are not well-designed, all things considered.

The pros of the stock-related awards:

- Around 45% of Richison’s US$18.4 million in stock-related awards came from restricted stock awards that vest over a three-year period.

- This multi-year vesting period means that a significant portion of Richison’s total compensation for 2019 is tied to the long-term business performance of Paycom, since the long-term stock price performance of the company is governed by its long-term business performance.

The cons of the stock-related awards:

- The remaining 55% or so of Richison’s US$18.4 million in stock-related awards came from stock awards that would vest once Paycom hits certain enterprise value targets.

- Specifically, half of the stock awards would vest when Paycom attains an enterprise value of US$8.65 billion and the other half would vest at an enterprise value of US$9.35 billion.

- The enterprise value is calculated as the sum of Paycom’s market capitalisation and net-debt (total debt minus cash and investments).

- We don’t like this portion of Richison’s stock-related awards for three reasons. First, there is no time-frame given for when the enterprise value targets should be attained; we would have preferred if the targets were measured over a multi-year timeframe. Second, the enterprise value targets were utterly uninspiring. For perspective, Paycom’s enterprise value at the end of 2018 was US$7 billion, which was very close to the targets of US$8.65 billion and US$9.35 billion; in fact, the stock awards vested by February 2019, merely one month after they were granted. Third, a company can increase its enterprise value, all things being equal, by taking on debt and then spending cash on unproductive assets. These actions, if taken, will hurt the strength of the business.

We think the cons of Richison’s stock-related awards outweigh the pros. But this is not a deal-breaker for us. According to Richison’s latest regulatory filings (as of 14 December 2020), he controlled 8.567 million Paycom shares, a stake that’s worth nearly US$3.4 billion at the 1 February 2021 share price of US$396. Paycom’s founder has significant skin in the game and crucially, the number of shares controlled by Richison has increased slightly over the past few years, as shown in the table below:

Source: Paycom proxy statements

Ultimately, we think that Richison’s large ownership stake in Paycom aligns his interests well with those of the company’s other shareholders.

On capability and ability to innovate

We rate Richison and his team highly here and there are a few things we want to discuss.

First, Richison founded Paycom back in 1998 because of his desire to better serve payroll customers. Prior to founding Paycom, he was employed at two payroll processing companies – Automatic Data Processing and Payroll 1 – and likely saw first-hand the problems posed by legacy payroll services. We are attracted to companies that are created because their founders saw a problem that needed fixing. To us, this is a strong signal of the entrepreneurial drive and innovative mindset of the companies’ leaders. It’s another big positive note that Paycom was one of the first few companies that brought payroll services entirely online – and this was back in 1998, when the internet was still a nascent technology!

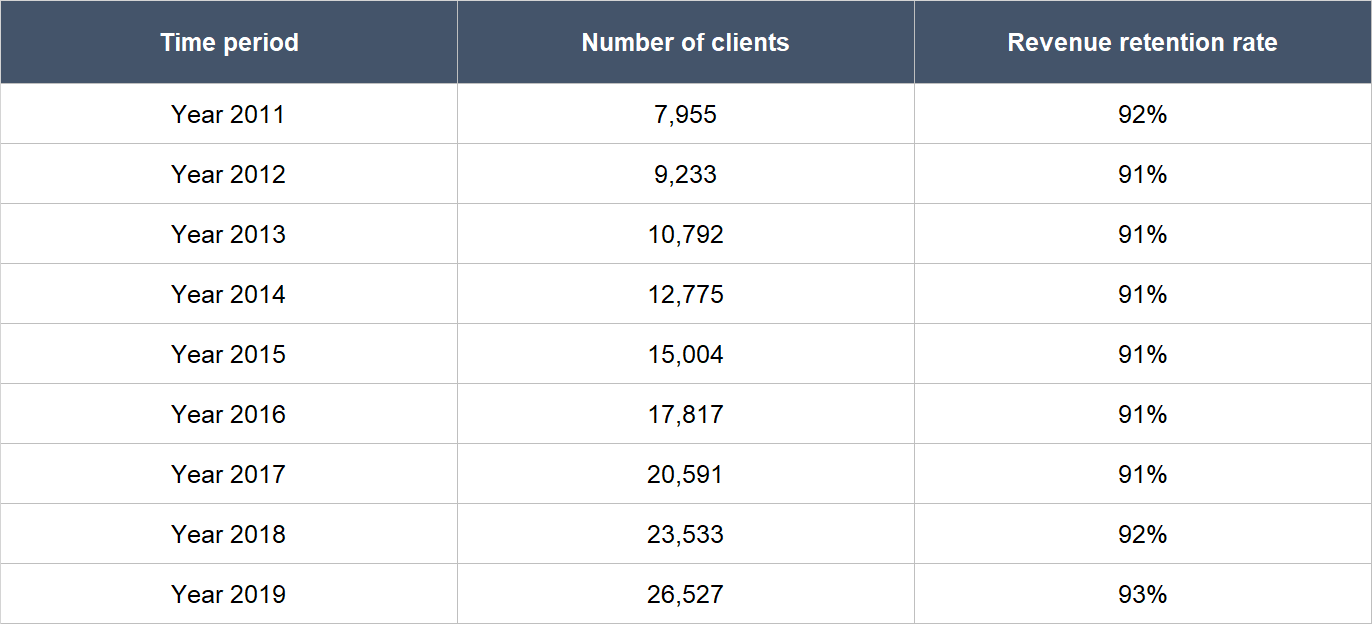

Second, Paycom has excelled at both growing its customer base and retaining its customers. The table below shows Paycom’s customer count and revenue retention rates from 2011 to 2019. In this period, Paycom increased its customer base by 16.2% annually while maintaining its revenue retention rate at 91% or higher.

Source: Paycom annual reports

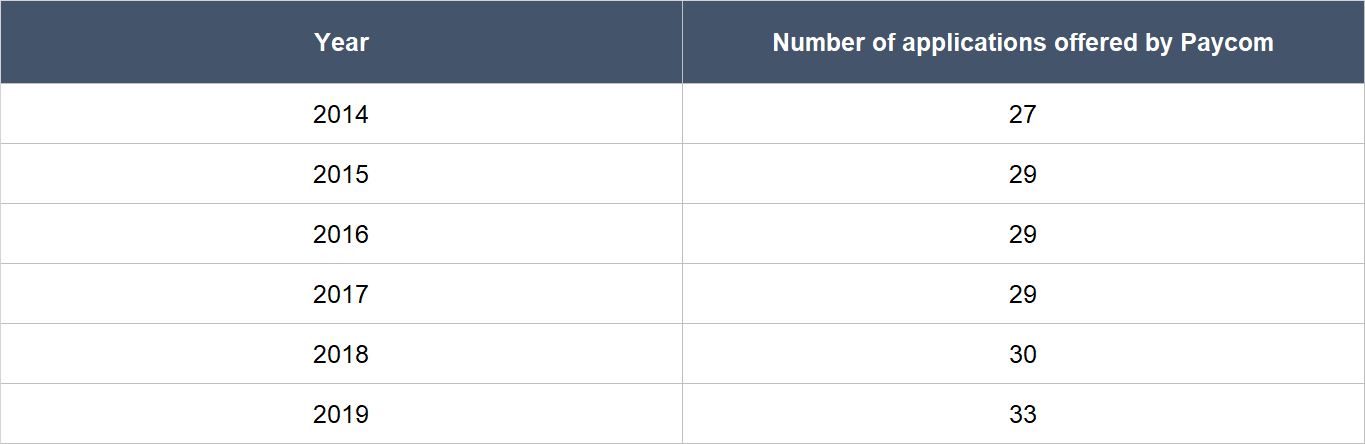

Third, Paycom has been steadily introducing new software applications over time, which are illustrated in the table below. Recent innovations that caught our eye include the Ask Here and Direct Data Exchange (DDX) platforms. Ask Here is Paycom’s one-stop online communication tool for employees of its customers to easily connect with their company-representatives whenever they have work-related questions. It automatically routes inquiries to representatives with the relevant expertise and ensures that all inquiries are addressed and that actions are taken. In 2019, Paycom launched DDX, an industry-first, which gives the company’s customers real-time insights on the efficiencies they gain through the use of human-resource technologies. DDX has gained significant traction since launch, and it helps Paycom’s customers to clearly see the benefits they can gain from the company’s software solutions. Here are some comments on the subject shared by Paycom’s management team in recent earnings conference calls:

“[First quarter of 2020]

We continue to see strong usage patterns of our products as measured by our Direct Data Exchange or DDX with usage scores well above Q4 levels. DDX numbers continue to be strong and improve as companies adopt a full employee usage strategy. When employees have a direct relationship with the database, the employee wins, the company wins from real savings estimated at $4.51 per HR task or data entry point as well as higher efficiency and overall employee satisfaction.[Third quarter of 2020]

DDX usage continues to trend upwards toward the 100% mark, up from the low 90s. In July, we changed our sales procedures to ensure that new clients commit to 100% usage. We are now at our highest DDX usage rate since launching the industry’s only software of its kind last year. CEOs and HR executives continue to see the savings from an employee’s direct relationship with the database. As a reminder, when an employee makes a data change themselves, the company saves $4.51, and the savings are calculated in real time using the DDX.”

Source: Paycom annual reports

Fourth, Richison appears to have built a wonderful corporate culture at Paycom. He was named one of the Top 100 large US company CEOs on Glassdoor in 2019, based on employee feedback, and Paycom was also recognized as one of Glassdoor’s 2020 Best Places to Work among large-sized US companies. Glassdoor is a platform for employees to rate their companies anonymously. Currently, 88% of Paycom-raters on Glassdoor will recommend the company to a friend and Richison has an approval rating of 94%, far higher than the average Glassdoor CEO rating of just 69% in 2019..

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Paycom is a software-as-a-service (SaaS) company and this means it has recurring revenues. In fact, from 2011 (the earliest year for which Paycom has reported its financials, since the company was listed in April 2014) to 2019, recurring revenues in each year were never less than 97.9% of the company’s total revenue. The company’s recurring revenues come from a few sources:

- Fees customers pay on a regular basis (weekly, bi-weekly, semi-monthly, or monthly) to use Paycom’s software solutions and for Paycom’s service for form filings and delivery of payroll checks and reports. The revenue here depends partly on the headcount of Paycom’s customers as well as the number of transactions Paycom has to process.

- Fees customers pay for Paycom to process annual and other types of payroll forms. Paycom’s revenue has seasonality, with revenue in the first quarter of the year being generally higher than in subsequent quarters, because payroll forms are typically processed in the first quarter.

- Interest earned from the funds Paycom holds on behalf of its clients. Paycom collects funds from clients in advance for future payroll tax submissions or to pay employees. These collections from clients are typically disbursed between one and 30 days after Paycom receives them, although some of the funds can be held up to 120 days. Paycom invests these funds in highly liquid money market funds, demand deposit accounts, commercial paper, and certificate of deposits until they have to be disbursed.

5. A proven ability to grow

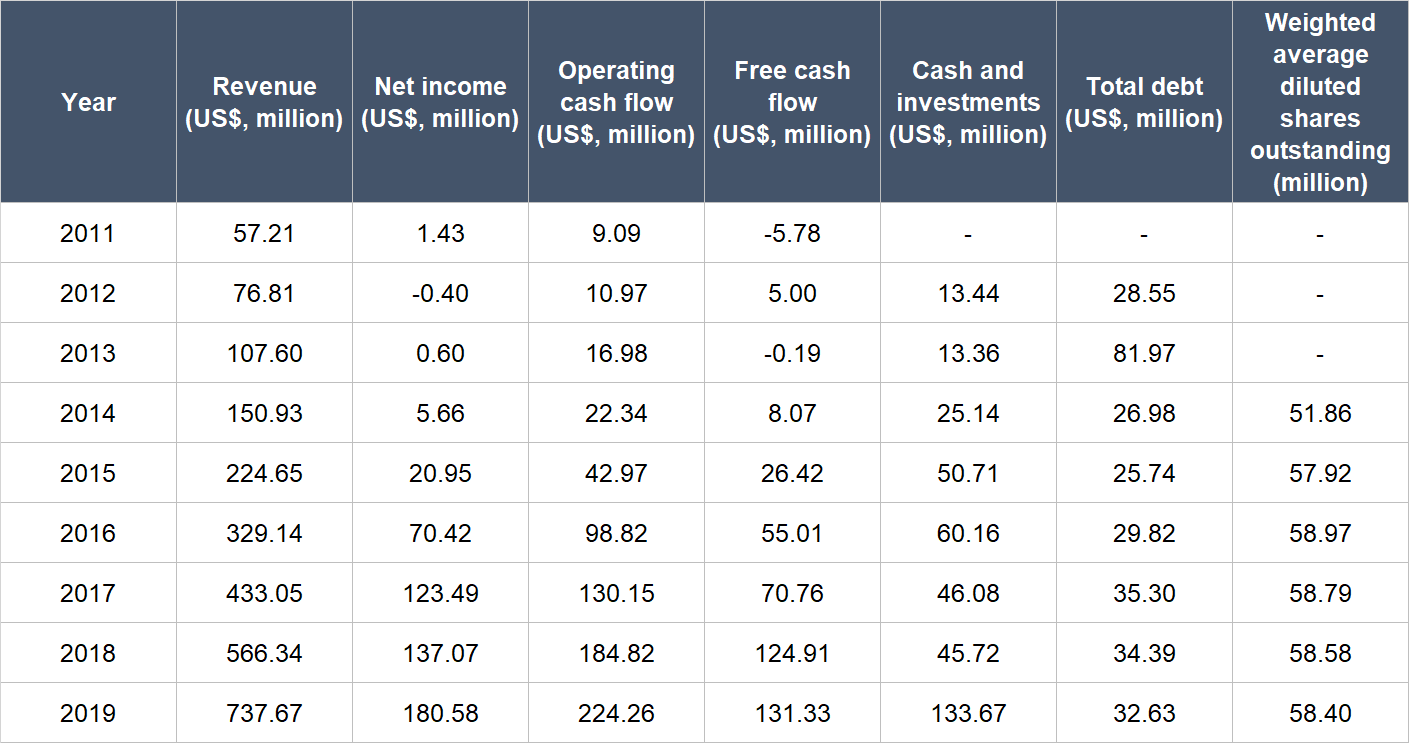

The table below show Paycom’s important financial numbers from 2011 to 2019:

Source: Paycom annual reports

A few things to note about Paycom’s financials:

- Revenue grew in each year, and has compounded at an impressive annual rate of 37.7% for 2011-2019. Paycom’s top-line growth had slowed in more recent times, but was still robust at 30.3% in 2019.

- Profitability improved tremendously from 2011 to 2019, and Paycom has been consistently profitable since 2013. Net income growth was excellent for 2015-2019 and 2019 at 71.4% per year and 31.7%, respectively. For further perspective, Paycom’s net income margin expanded from 3.8% in 2014 to 24.5% in 2019.

- Operating cash flow was consistently positive for the timeframe under study, and had grown at 49.3% per year from 2011 to 2019. Growth in 2019 was 21.3%, which is not too shabby.

- In a similar manner to Paycom’s net income, free cash flow had increased markedly from 2011 to 2019, and was consistently positive from 2014 onwards. Growth was only 5.1% in 2019, which is a significant slowdown from the annual growth of 49.3% for 2015-2019, but it’s not a cause for any concern, in our view.

- Paycom has kept its balance sheet strong from 2015 onwards, with the amount of cash and investments exceeding debt by a wide margin.

- Dilution has not been a problem at Paycom, with the weighted average diluted share count increasing by only 2.4% per year from 2014 to 2019 (we started counting from 2014 because the company was listed in the month of April of the year). In fact, the weighted average diluted share count had declined in 2017, 2018, and 2019.

2020 has been a relatively difficult year for Paycom, compared to the lofty standards it has achieved in the past. As discussed earlier, Paycom has SMB customers, and also has revenues that depend on its customers’ headcount and volume of payroll transactions. The emergence of COVID-19, which became a pandemic in March 2020, resulted in headcount reductions in Paycom’s client base. As a result, the growth of the company’s recurring revenues has been affected in 2020, especially in the second and third quarters of the year. Paycom also expects its recurring revenues in future periods to be negatively impacted by the headcount reductions. But it’s not all doom and gloom. The table below shows the year-on-year changes in Paycom’s revenue, net income, operating cash flow, and free cash flow in the first three quarters of 2020:

Source: Paycom quarterly earnings updates

Paycom still managed to produce year-on-year revenue growth in each of the first three quarters of 2020. This is impressive given the backdrop. Moreover, new business wins have been very strong for Paycom for the year thus far. Here’s the company’s management sharing more on the topic in recent earnings conference calls:

“[First quarter of 2020]

First quarter results were strong driven by our high margin recurring revenue business model and continued strength of new business adds.[Second quarter of 2020]

In fact, Q2 was our best quarter ever from a new business sales perspective by a large margin, and we will continue to spend aggressively on advertising throughout Q3 and Q4 above the Q2 levels as we deliver our value proposition to our massive target market. With less than 5% of the total addressable market already captured, we have a long way to go. The digital transformation for business is accelerating, and our investment in expanding our market share is working.[Third quarter of 2020]

Well, I mean, our bookings and our leads, our new business sales and our new business starts have all remained at record highs. And from where I sit right now, I don’t see that changing.”

Ultimately, we see COVID-19 as a temporary setback for Paycom. The pandemic has caused some short-term pain, but over the long run, when the coast is clear, Paycom’s growth should accelerate from 2020’s level as the economy recovers and firms start hiring and expanding their headcount again.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Paycom excels in this criterion.

First, there’s still significant room to grow for the company, even just within the USA. Earlier, we showed that Paycom’s trailing revenue of US$813.9 million is only a tiny fraction of its estimated total addressable market of US$26.5 billion in the country in 2017.

Second, Paycom has been generating strong and growing free cash flow for a number of years, as discussed earlier. The company’s average free cash flow margin (free cash flow as a percentage of revenue) for 2015-2019 was a respectable 16.9%. And despite the presence of COVID-19 in the first nine months of 2020, Paycom’s free cash flow margin was still 16.2% for the period. We think it’s possible for Paycom’s future free cash flow margin to be in the mid-20s percentage range at the very least, given the typically high free cash flow margins achieved by successful SaaS companies.

Valuation

We like to keep things simple in the valuation process. In Paycom’s case, we think the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value. This is because Paycom has already been producing positive and growing profit as well as free cash flow for a number of years.

We completed our purchases of Paycom shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$295 per Paycom share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios of around 88 and 141, respectively. These ratios are high in and of themselves – and that’s a risk. The ratios were also high relative to their own histories. Here’s a chart showing Paycom’s P/E and P/FCF ratios over the five years ended 1 February 2021:

But Paycom has a large total addressable market in relation to its current business. The company’s software products also help to solve an important pain point for its customers, and it has a reasonably long history of solid growth. So we think there’s a high probability that Paycom can continue to take advantage of its market opportunity to increase the scale of its business. Because of these, we’re happy to pay up for Paycom as we think there’s a good chance it could grow into its valuation.

For perspective, Paycom carried P/E and P/FCF ratios of around 141 and 182 at the 1 February 2021 share price of US$396.

The risks involved

There are a few risks that we see with our Paycom investment.

1. A big threat to Paycom’s business, in our view, is competition. The market for HCM software solutions is rapidly evolving and highly competitive. Paycom named 10 competitors in its 2019 annual report and they include companies such as Automatic Data Processing, Oracle Corporation, Paychex, SAP and Workday. Some of the competitors compete with Paycom across a number of application-categories, while some compete only in one category. Paycom has so far held its ground admirably, given its impressive record at retaining and finding new clients. But we can’t take anything for granted. It is possible for any of Paycom’s competitors to come up with a better cloud-based HCM solution compared to what the company has to offer. If so, Paycom’s business could suffer.

2. There’s also key-man risk at Paycom. We think that Chad Richison, Paycom’s founder, president, and CEO, has been a key pillar of the company’s success thus far. We’ll be keeping an eye on the leadership transition process should he step away from the company for any reason. The good thing is that Richison is still relatively young at just 49 years old, so he should still have plenty of gas left in the tank to continue leading Paycom.

3. Another risk to Paycom’s growth is hacking. Due to the nature of its business, the company handles proprietary and confidential information about its clients as well as their employees. If Paycom were to suffer any data breach, it could suffer crippling reputational damage.

4. The fourth risk we’re watching are future downturns in the economy. Paycom serves mainly small to mid-sized business (SMBs) in the USA. SMBs have historically suffered more during recessions as compared to large businesses. According to a study by the Federal Reserve Bank of New York, small companies suffered steeper sales declines than large companies during the 2007-09 financial crisis. In the current context, the presence of COVID-19 is probably the biggest potential driver for any global economic pain in the near-term (after already causing hurt last year). As mentioned earlier, COVID-19 has already had a negative impact on Paycom’s growth in 2020. If the pandemic results in a further extended period of economic contraction in the USA, Paycom’s business is likely to deteriorate.

5. Lastly, Paycom’s high valuation is a risk, as we mentioned earlier. We’re comfortable paying up for the company’s shares. But, if the company’s growth falters – even if it’s temporary in nature – there could be painful falls in its share price.

Summary and allocation commentary

To sum up Paycom, the company has:

- A large addressable market; Paycom is currently operating only in the USA, but the US payroll services and HCM applications markets alone are already much larger than the company’s current revenue

- A robust balance sheet that has more cash and investments than debt

- An innovative and highly capable leader in Chad Richison, who also has significant skin in the game

- High levels of recurring revenues; in fact, recurring revenues in each year have never been less than 97.9% of total revenue

- An excellent multi-year track record of growth in revenue, net income, and free cash flow

- A high likelihood of generating a strong and growing stream of free cash flow in the future.

Paycom’s high valuation is a risk, and there are more. These include the risk of competitors outgunning Paycom; key-man risk; the potential for severe reputational damage because of data breaches; and future recessions.

After weighing the pros and cons, we initiated a 1% position – a small-sized allocation – in Paycom with Compounder Fund’s initial capital. We appreciate all the strengths in Paycom’s business that we saw and described in this article. But our enthusiasm was tempered by two things. First, Paycom’s growth, in the near term at least, is crimped by COVID-19. Second, while Paycom’s pre-COVID growth is excellent, we think the valuation is on the higher end of things when compared to the company’s historical growth rates.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Besides Paycom Software, Compounder Fund does not own shares in any other companies mentioned. Holdings are subject to change at any time.