Compounder Fund: Nu Holdings Investment Thesis - 24 Jul 2024

Data as of 22 July 2024

Nu Holdings (NYSE: NU), which is based in Brazil but listed in the USA, is a company in Compounder Fund’s portfolio that we invested in for the first time in June 2024. This article describes our investment thesis for the company.

Company description

Nu Holdings, the holding company of Nubank, which is one of the largest digital banks in the world today, was founded in 2013 by David Vélez, Cristina Junqueira, and Edward Wible. From Nu Holdings’ earliest days, its mission was – and still is – to fight complexity to empower people. Its founders thought providing financial services in Latin America was a way to fulfil the mission. So in 2014, Nu Holdings’ first product, the Nu Credit Card, a purple Mastercard-branded credit card, was launched in Brazil. From then to now, Nu Holdings has expanded its product suite and geographical reach.

The Nu Holdings of today offers customers in Brazil financial products across what it calls the “Five Financial Seasons”, namely, spending, saving, investing, borrowing, and protection. All of Nu Holdings’ products are fully digital solutions and available through its mobile app; Nubank has no physical branches. The products for the Five Financial Seasons are:

- Spending solutions:

- Nu Credit and Prepaid Card: Nu Holdings’ core product, it is still a Mastercard-branded card, is 100% digital, and is both a credit and a debit card. Some of its key features include no fees or annuity charges (when the Nu Credit Card was launched, it was the first credit card in Brazil to have no annual fees); integration with WhatsApp Pay (a prepaid card-only function), Android Pay, and Apple Pay; and acceptance by more than 30 million merchants worldwide.

- Ultraviolet Bundle: This is a product for affluent customers that consists of Nu Holdings’ premium metal credit and prepaid card and a list of perks that include, among others: (1) full benefits of Mastercard Black, such as VIP airport lounge access, (2) premium 24/7 customer support, (3) free insurance against digital transaction fraud, and (4) benefits for managing family finances. The Ultraviolet Bundle comes with a monthly fee of R$49 (around US$9), but is free for customers who spend more than R$5,000 or have more than R$50,000 in invested assets with Nu Holdings.

- Mobile Payments: NuAccount customers can make and receive instant payments for money transfers, bills, and everyday purchases through their mobile device. Launched in 2017, NuAccount is Nu Holdings’ fully-digital banking account solution that pioneered free deposits, transfers, and payments, and low-fee ATM cash withdrawals. It also gave customers a yield on their savings that equaled to 100% of Brazil’s interbank deposit rate. In contrast, incumbent banks charged a range of fees for similar services, and paid a much lower yield to customers. It’s worth noting that the NuAccount’s mobile payments solutions embrace PIX, which is a 24/7, instant payment system launched in late-2020 by the Central Bank of Brazil. PIX is widely adopted by Brazilians, with around 72% of the country’s population holding an active PIX key at the end of 2023. Total PIX volumes reached US$2.9 trillion in 2023, up 51% from 2022.

- Nu Shopping: Nu Holdings’ mobile app has an integrated function for customers to shop at some of Brazil’s largest ecommerce retailers and it comes with cashback deals and exclusive benefits, offers, and pricing, among other features.

- Nu Business Prepaid and Credit Card: This is similar to the Nu Credit and Prepaid Card but is available for businesses to use.

- Saving solutions:

- Nu Personal Accounts: The NuAccount for individual customers. As mentioned earlier, the NuAccount is a fully-digital banking account. It has no annual or maintenance fee and supports a whole range of personal finance activities, from daily purchases to money transfers and savings. The NuAccount today still provides a yield on customers’ savings that equal the Brazilian interbank deposit rate.

- Nu Business Accounts: The NuAccount designed specifically for businesses. It also has no annual or maintenance fee and has features that help customers manage their businesses, such as the ability to set up regular payments and receive payments from customers.

- Investing Solutions:

- Money Boxes (Caixinhas): A goal-based investing solution for customers that comes with segregated investment portfolios. Importantly, customers have the option to increase their Nu Credit Card limits through assets invested in Money Boxes.

- Nucoin: Nu Holdings’ proprietary utility token for its loyalty program. Customers get Nucoins when spending with the Nu Credit and Prepaid Cards and these coins can be traded by customers. Holders of Nucoins may also be offered financial benefits (such as lotteries and discounts in transaction fees) by Nu Holdings.

- Investment Accounts: This solution, which is branded as NuInvest, came from Nu Holdings’ acquisition of Easynvest in 2021. NuInvest offers stocks, fixed-income, stock options, exchange-traded funds, and multimarket funds directly to customers. Some highlights for customers include transparent fee pricing, no-fee stock trading, and the ability to invest as little as US$1.

- NuCrypto: A solution for customers to trade cryptocurrencies 24/7 through Nu Holdings’ mobile app. Similar to NuInvest, customers of NuCrypto can get started with as little as US$1.

- Borrowing solutions:

- Personal unsecured loans: Launched in 2019, Nu Holdings’ personal unsecured loans product is 100% digital for customers of the Nu Credit Card and NuAccount. Nu Holdings provides real-time underwriting and instant deposit of money upon loan approval. Borrowers get to enjoy rates that are lower than the market average, and easy management of their loans through Nu Holdings’ mobile app.

- Personal secured loans (backed by investments): Borrowers can use their investments with Nu Holdings as a guarantee to access a larger line of credit at lower interest rates.

- Personal secured loans (payroll deductible loans): Borrowers can use their future income as a guarantee to obtain loans with very low interest rates (the rates are in fact, the lowest in the market). Loan instalments are deducted directly from borrowers’ payroll.

- Personal secured loans (backed by FGTS): FGTS is a severance unemployment benefit in Brazil and borrowers can have early-access to FGTS payments through this Nu Holdings product. A borrower’s FGTS-loan instalments are repaid by FGTS directly to Nu Holdings.

- PIX financing: Customers can use their credit line with Nu Holdings to make PIX transactions.

- Boleto financing: Nu Credit Card and NuAccount customers can make Boleto payments using their credit lines. Boletos are banking payment slips issued by merchants that are used for payments in Brazil.

- Purchase financing: Nu Credit Card customers can split their purchases into instalments after making a purchase.

- NuPay: Launched in 2022, NuPay allows Nu Holdings customers to pay for online purchases through Nu Holdings’ mobile app and skip the need to provide credit card and/or bank details. One of the key benefits of NuPay is the elimination of fraud-risk and theft of credit card information.

- Protection solutions: Nu Holdings acts as a broker for customers to purchase life, mobile, auto, home, and financial protection insurance policies. The policies’ underwriters are Chubb (for all insurance policies except auto insurance) and Usebens (for auto insurance). Premiums for life policies purchased through Nu Holdings start as low as US$2 and customers get to enjoy a fast application process, customised insurance packages, and an easy claims process.

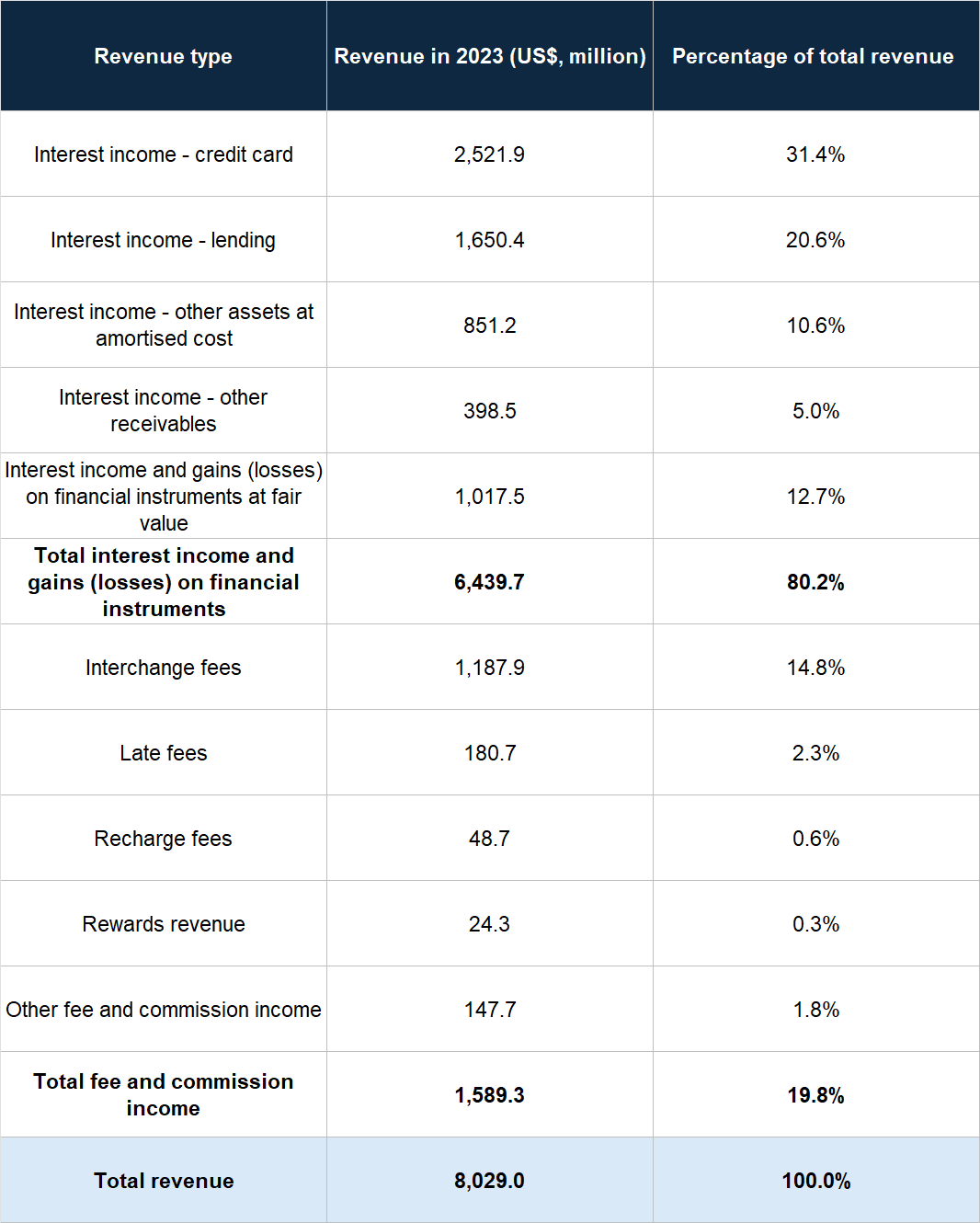

The products for the Five Financial Seasons bring a number of different revenue streams for Nu Holdings. These streams, and their amounts in 2023, are shown in Table 1 below. The streams can be grouped into two major categories: (1) Interest income and gains or losses on financial instruments, and (2) fee and commission income. In the first category, Nu Holdings earns revenue from the interest from loans, credit card receivables, and other financial assets. The first revenue category also comprises interest from, and changes in the fair value of, certain financial assets – mostly Brazilian government bonds – that Nu Holdings owns. The second category consists of interchange fees that Nu Holdings earns when customers use the Nu Credit and Debit Card (the interchange fee is earned by issuers of credit and debit cards when they are used; see our thesis on Adyen for more information). There are also:

- Late fees, which are fees from late payment of credit card bills

- Recharge fees, which are revenue from the sale of prepaid telephone credits to customers

- Rewards revenue, which consists of subscription and interchange fees related to NuRewards; NuRewards is Nu Holdings’ loyalty program

- Other fee and commission income, comprising brokerage commissions from Protection solutions, commission income from issuing boletos, fees for cash withdrawals, and commissions from merchants participating in NuShopping.

Table 1; Source: Nu Holdings 2023 annual report

From the figures shown in Table 1, it’s clear that most of Nu Holdings’ revenue in 2023 came from interest-related income, and most of that interest-related income was from the company lending money to customers (this comprises “Interest income – credit card”, “Interest income – lending”, and “Interest income – other receivables”). Table 1 also illustrates the importance of the Nu Credit and Debit Card product as it directly accounted for at least 46.2% (this comprises “Interest income – credit card” and “interchange fees”) of Nu Holdings’ revenue in 2023.

Regarding Nu Holdings’ geographic expansion, it entered Mexico in 2019, followed by Colombia in 2020. In both cases, Nu Holdings launched with its flagship Nu Credit Card product. Although Nu Holdings’ business now extends beyond Brazil, the company is still Brazil-centric. It ended the first quarter of 2024 with 99.3 million customers (it crossed the 100 million mark in May 2024), of which 91.8 million are in Brazil, 6.6 million in Mexico, and 0.9 million in Colombia. For another perspective on the geographic distribution of Nu Holdings’ business, 93% of the company’s revenue in 2023 from its main lending operations and fee and commission income was from Brazil.

It’s not surprising that with 100 million customers currently, Nu Holdings does not experience any customer-concentration risk. There was no single customer that accounted for 10% or more of the company’s revenue in each year going back to at least 2018.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Nu Holdings.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

For context, Latin America had a total population of 645 million people and GDP of US$6.5 trillion in 2023, based on data from the International Monetary Fund (IMF). Meanwhile, Brazil, Mexico, and Colombia – the three countries Nu Holdings currently operates in – accounted for 60% (around 387 million) of the region’s population and 66% (around US$4.3 trillion) of its GDP. Brazil is the largest country among the trio, with a population of 204 million and GDP of US$2.2 trillion. This is followed by Mexico, where the self-same figures are 131 million and US$1.8 trillion. Colombia’s population of 52 million and GDP of around US$360 billion makes it the smallest.

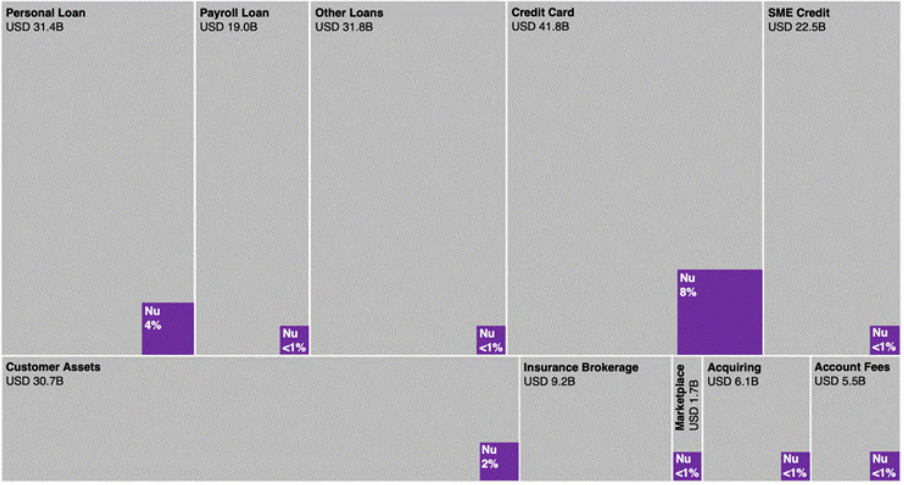

Nu Holdings’ management estimates the company’s serviceable addressable market (SAM) in Brazil alone to be US$145.7 billion in 2023. This comprises the following revenue streams:

- Retail credit, which is interest income net of funding costs and credit charges from secured and unsecured personal loans, auto loans, credit card financing and credit card revolvers

- SME credit, which is interest income net of funding costs and credit charges from lending to small, medium enterprises (Nu Holdings also serves SMEs – at the end of 2023, the company had 93.9 million customers, of which 3.6 million are SMEs in Brazil)

- Interchange fees from payments

- Fees earned from customer assets, such as brokerage fees for investments, and interest income net of yields on customer deposits

- Insurance brokerage fees

- Fees from e-commerce marketplace transactions

- Acquiring and services fees, which are fees paid by merchants in card-transactions and other account-related transaction fees

Meanwhile, the same revenue streams in Mexico and Colombia provide SAMs of US$38.3 billion and US$16.0 billion, respectively, for Nu Holdings. This brings the total SAM for Nu Holdings in the three countries to US$200 billion currently, which dwarves the company’s trailing revenue of US$9.2 billion. Figure 1 below illustrates management’s estimates of Nu Holdings’ market share, based on 2023 numbers, for the product categories it is exposed to; note the single-digit market share in each category, with the highest being credit cards at just 8%.

Figure 1; Source: Nu Holdings 2023 annual report

For another perspective on Nu Holdings’ room for growth, there’s the low penetration rate in Latin America for banking services. Here’s the relevant data from Nu Holdings’ 2023 annual report:

“According to the latest available World Bank data, 16.0% of the 169.3 million people aged 15 and above in Brazil did not have a bank account as of 2021; this compares to 44.0% of the 39.2 million people aged 15 and above for Colombia, according to the same source; and in Mexico 50.9% of the 101.8 million people aged between 18 and 70 years old did not have a bank account as of 2021, according to INEGI’s ENIF (National Survey of Financial Inclusion). Thus, we estimate that the three countries collectively accounted for 77.1 million unbanked adults as of 2021…

…Credit card penetration in Brazil and Colombia stood at 40% and 13% of the population aged 15 and above, respectively, compared to 67% in the United States and 62% in the United Kingdom, according to World Bank’s most recent data from 2021. In Mexico, credit card penetration stood at 11%, considering those issued by banks, and 20% considering retailers, of the population aged between 18 and 70 years old, according to the INEGI’s ENIF 2021 report.”

We believe Nu Holdings is poised to win significant share in the financial services markets of Brazil, Mexico, and Colombia in the years ahead. This is for three reasons.

Firstly, incumbent banks in Brazil, Mexico, and Colombia have large and expensive branch networks, which results in a high cost-to-serve. In 2023, each of the main incumbents in Brazil had between 2,695 and 3,992 branches, and 55,611 and 86,220 employees. Nu Holdings has no physical branches and a headcount of just around 7,700. Nu Holdings’ management estimates that the company’s cost-to-serve and general and administrative expense per active customer in 2023 was 85% lower than those of the incumbents. Having a lower cost-to-serve is an important competitive advantage because it allows Nu Holdings to provide financial products to customers at more attractive prices than the incumbents and yet still retain positive unit economics. This is aptly illustrated by what’s happening in Mexico at the moment. Deposits are the largest source of profit for incumbent Mexican banks because these banks tend to pay a deposit rate of 3%-4% to customers while earning a low-teens yield on Mexican government debt. Nu Holdings has managed to earn positive unit economics and successfully win customers in Mexico while offering much higher deposit yields.

We want to highlight that the banking industries of Brazil, Mexico, and Colombia are all highly concentrated, with the five largest banks in each of these three countries controlling 70% to 87% of all loans in various segments in 2022. This means that Nu Holdings has a low cost-to-serve advantage against all or at least most of its major banking competitors. We will further discuss Nu Holdings’ cost-to-serve in the “A management team with integrity, capability, and an innovative mindset” subsection.

Secondly, incumbent banks in Nu Holdings’ markets tend to provide poor customer service. Part of Nu Holdings’ founding lore involves the horrid experience that co-founder and CEO David Vélez had with opening a bank account in Brazil when he was working there (he’s from Colombia). This is what he shared in his shareholders’ letter in Nu Holdings’ IPO prospectus:

“In mid-2012, I entered the branch of one of Brazil’s largest banks to open my first Brazilian bank account. As I approached the first bulletproof door that was flanked by armed security guards, I sensed that this was not going to be easy. During the following four months I spent long hours in queues, calling the call center, and returning to the bank branch with an increasing number of documents, until finally a bank account that would charge hundreds of reais per year in fees was approved in my name. The entire experience was incredibly frustrating.”

Nu Holdings’ management, in contrast, is obsessed with the customer experience, so much so that the company’s NPS (Net Promoter Score) is at a level that management believes is two to three times better than incumbents and other fintechs in Brazil, Mexico, and Colombia. There are other examples supporting the idea that Nu Holdings is providing a much better customer experience than incumbents banks:

- In the “Company description” section, we mentioned that the Nu Personal Account and Nu Business Account both do not have annual charges or maintenance fees. This is not the case with at least some of the incumbent banks in Brazil (including some of the largest, such as Itaú Unibanco and Banco Bradesco), whose personal banking and business banking accounts tend to carry a range of maintenance fees.

- An average of 80%-90% of Nu Holdings’ acquired customers per year since its inception have come from word-of-mouth or direct unpaid referrals from existing customers without the need for significant marketing expenses.

- Brazil’s central bank conducts a periodic survey on the rate of customer complaints that the country’s financial institutions receive. An edition of the survey, for the first quarter of 2023, found that Nu Holdings had the second lowest rate of customer complaints among the top 15 Brazilian financial institutions by number of customers.

- Nu Holdings has established a primary banking relationship with 59% of its active customers who had been with the company for more than 12 months as of the first quarter of 2024, up from 58% in 2022 and 55% in 2021; Nu Holdings considers itself the primary bank for active customers who have been with the company for over a year and have at least 50% of their post-tax monthly income move out of their NuAccount (excluding self-transfers) in any given month.

- Nu Holdings has given first-time access to credit cards to nearly 50 million individuals in Brazil as of December 2023.

Thirdly, Nu Holdings’ customers skew younger compared to incumbent banks in Latin America, which gives the company more room to grow with its customers as they gain wealth. Customers under the ages of 35 and 45 comprised 54% and 77%, respectively, of Nu Holdings’ customers at end-2022, compared to 30% and 52% for incumbent banks at end-2021. Meanwhile, Nu Holdings’ customers aged 20-24 are expected to grow their real income by about 70% over the next decade (based on a comparison of income levels between customers aged 20-24 and those aged 30-34).

Another aspect of Nu Holdings’ growth opportunities we want to discuss is the possibility of the company moving beyond financial services. In the “Company description” section, we wrote that Nu Holdings’ mission is to fight complexity to empower people; notice that there’s no specific mention of financial services or banking. It is a carefully chosen mission statement and speaks to the unbounded (but realistic) ambition that the management team has. During an internal interview in May 2024, Vélez shared (emphases are ours):

“One of the decisions, design decisions, that we did at the very beginning was: “What was going to be the purpose of the company, why do we exist?” And after a lot of conversations and discussion with that early group of 10-15 people, we concluded that the goal of the company is to fight complexity to empower people. We decided that the biggest enemy that consumers have is complexity. And specifically when we saw financial services, it’s such a complex environment where there was not that many alternatives when we started…

…We think that complexity also exists beyond Brazil. This is not a Brazilian-specific problem or maybe even a Latin America-specific problem. Complexity is everywhere, globally in all sectors. And so that’s the beauty of this big core purpose. It’s almost an infinite goal…

…And your phase three, which is going beyond financial services, is also a way where we are executing that core purpose, where we suddenly start hearing from consumers: “Nubank, when are you launching insurance?”

“Nubank, when are you launching a beverage company?”

“Nubank, when are you launching an airline?”

No, we’re not going to go do all of this stuff. Obviously, we’re going to pick our areas. But I think what we hear from the consumer is: “Help me. I see complexity in all of these different areas. And the moment I started getting services from Nubank, that’s the gold standard of services. I expect that type of service in health care, in telecom, in insurance, in really everywhere. I get almost used to that level of service and I cannot accept anything else beyond being in the center of the company.””

During the first half of 2024, Nu Holdings branched into telecommunications services in two small ways. Firstly, the company gained approval from Brazil’s telecommunications regulator for its plan to become a MVNO (mobile virtual network operator) in Brazil by partnering with Claro, a telco operating in Latin America and Europe. Secondly, the company launched an eSIM (embedded SIM) service that provides customers with 10GB of free roaming internet in more than 40 countries. Nu Holdings has been low-key about these developments (there are no official press releases on its partnership with Claro, for example) so not much is currently known about their progress.

We appreciate the ambition of Nu Holdings’ management team and the carefully crafted mission statement, which reminds us of Amazon’s own, which is to be Earth’s Most Customer-Centric Company (this is not the only similarity that Nu Holdings shares with Amazon – more on this in the “A management team with integrity, capability, and an innovative mindset” subsection). Notice that Amazon’s mission does not mention e-commerce or cloud computing or digital advertising, which are today the three important pillars of the company’s business. But nonetheless, the intense focus on customers by Amazon’s leaders have pushed the company to grow in multiple different ways. A similar thing may happen for Nu Holdings in the distant future. But to be clear, our current stance is that any success the company has outside of Latin America’s financial services industry is merely icing on the cake for us. We’ll also be watching Nu Holdings’ forays beyond financial services to ensure that it’s not biting off more than it can chew.

2. A strong balance sheet with minimal or a reasonable amount of debt

Since Nu Holdings’ primary business is being a digital bank, we’re looking at the leverage ratio, which is the ratio of total assets to shareholders’ equity, as the main way to assess the strength of its balance sheet. The lower the leverage ratio, the higher the percentage of the bank’s assets that is being funded directly by shareholders’ equity, and the sturdier its balance sheet.

As of 30 March 2024, Nu Holdings had total assets of US$43.8 billion and shareholders’ equity of US$6.8 billion, which gives it a robust leverage ratio of just 6.4. This is also significantly lower than the leverage ratios of Latin America’s three largest banks by assets (which also happen to be Brazil’s three largest banks). They are, in descending order, Itaú Unibanco, Banco do Brasil, and Banco Bradesco, and they currently have leverage ratios of 14.1, 13.1, and 11.8, respectively.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Nu Holdings’ most important leader is the 42-year-old David Vélez, who as we mentioned earlier, is the company’s co-founder and CEO. We appreciate the fact that Vélez has already been leading Nu Holdings for more than a decade despite his current young age. Prior to founding Nu Holdings, he had stints at investment and investment banking firms such as Sequoia Capital, General Atlantic, Goldman Sachs, and Morgan Stanley. Vélez came up with the idea of Nu Holdings, but he also recognised that he had plenty of gaps to fill, since he was an outsider to Brazil’s banking industry and was not sufficiently proficient with software development. Nu Holdings’ other two co-founders, the aforementioned Cristina Junqueira and Edward Wible, were approached by Vélez to complement his skillsets. Junqueira, 41, understood the inner-workings of Brazil’s banking industry from her previous employment with Itaú Unibanco (Brazil’s largest bank at the moment) and is currently the Chief Growth Officer of Nu Holdings. Wible was responsible for Nu Holdings’ entire technology strategy from its earliest days and only stepped down as Chief Technology Officer in April 2021 to fulfil a long personal wish to be in a role where he can contribute directly to the company’s systems and infrastructure; it’s unclear to us if Wible is still involved with Nu Holdings. The company’s current Chief Technology Officer is Vitor Olivier, 34, who joined in 2014.

There’s very little that’s known about the compensation structure for Nu Holdings’ management team. The company has to-date never publicly disclosed the compensation paid to management on an individual basis. Some of the key things that are known:

- The total compensation of Nu Holdings’ directors and key management were US$60.1 million in 2023, US$122.9 million in 2022, and US$34.4 million in 2021; these are the calendar years that ended after Nu Holdings’ initial public offering (IPO) in December 2021.

- Management’s compensation currently includes a fixed base salary, participation in a profit sharing program, and share-based compensation.

- Management’s share-based compensation consists of awards of options and RSUs (restricted stock units) and the amount depends on a number of factors including individual performance, business unit performance, Nu Holdings’ overall performance, and performance according to certain of the company’s long-term goals and objectives.

None of the key things above particularly inspires confidence in us on the integrity of management. The compensation amounts are somewhat high (for perspective, Nu Holdings’ net profit attributable to shareholders in 2023 and 2022 were US$1.03 billion and -US$364.6 million, respectively). There’s also no information on whether management is incentivised on Nu Holdings achieving sustainable, long-term per share business growth. But we see three important saving graces.

Firstly, there’s the history behind Vélez’s 2021 Contingent Share Award (2021 CSA) that was granted on 22 November 2021. Under the 2021 CSA, Vélez was set to be issued the following:

- Nu Holdings Class A shares equal to 1% of the total number of fully-diluted ordinary shares in issue when the Class A share price is equal to or greater than US$18.69 but less than US$35.30

- Nu Holdings Class A shares equal to 1% of the total number of fully-diluted ordinary shares in issue when the Class A share price is equal to or greater than US$35.30 per share

In total, the 2021 CSA would result in shareholder dilution of up to 2% if Nu Holdings’ share price exceeded US$35.30. But on 29 November 2022, Vélez terminated the 2021 CSA on his own accord. He thought that his ownership of over 20% of Nu Holdings’ shares (at the time) was more than sufficient to align his interests with the company’s other shareholders. He also declined any new compensation in any form for 2022 and 2023. We think Vélez’s decision to cancel his 2021 CSA demonstrates high integrity on his part. We actually see the 2021 CSA as an absolutely fair compensation scheme. Nu Holdings’ share prices at the close on the day of its IPO and on 28 November 2022 (the day before the award was terminated) was US$10.33 and US$4.22, respectively – this means that Vélez has to build substantial value in Nu Holdings’ business in order for its share price to rise to sufficient heights for both tranches of the 2021 CSA to kick in. Yet, he chose to walk away from the award.

Secondly, Vélez insisted on including a complicated program into Nu Holdings’ IPO process to make an impact on investor-education and on increasing the amount of participation in the stock market by the Brazilian public. During a recent interview, Federico Sandler, who was Nu Holdings’ investor relations officer during its IPO (he left the company in March 2022), described the program and the difficulties management faced:

“All IPOs are complex because it’s a ton of work. But in this IPO in particular, you had a dual listing. But then you had what you mentioned, which is a DSP, which is the Direct Share Program. Basically what happened is Nubank gifted and enrolled 7.5 million customers into NuSocios, where they gave them one BDR, or a Brazilian Depository Receipt, and then they also offered to 800,000 customers the ability to make a paid reservation for shares that would come out in the IPO. And basically the addition of the 7.5 million people who were gifted a share, plus the 800,000 that were able to make a paid reservation, you were able to almost double the amount of retail investors in Brazil. It went from 2.5 million to north of 5 million.

Why was this complex? Because the Brazilian regulator is not like the US regulator. They had no idea what a DSP was. There was a whole chapter around financial education. It’s not just, I give you the BDR and you do whatever you want with it. The idea is, I give you the BDR but I don’t let you sell it for 12 months so that I can educate you in what is risk, what is compounding, what is the long term. And then the bet was that over the last over 12 months, you wouldn’t sell the shares. But how do you first of all pitch this to the regulator? But then how do you design the product so that your app doesn’t blow up once people come to reserve the shares? So it was like dying by a thousand paper cuts essentially.”

The third saving grace we observed is something we alluded to earlier: Vélez’s high insider ownership of Nu Holdings shares. He currently controls 967.3 million shares of the company. At Nu Holdings’ 22 July 2024 share price of US$12.99, Vélez’s stake is worth more than US$12.5 billion, which represents significant skin in the game.

We do note that the lion’s share (962.1 million) of Vélez’s Nu Holdings shares are of the Class B variety. Nu Holdings has two share classes with identical economic rights but different voting rights: (1) Class B, which are not traded and hold 20 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. As a result, Vélez controlled 75.9% of Nu Holdings’ voting power (as of 31 December 2023) despite holding just 20% of the company’s total shares. A manager having significant control over the company can potentially be bad for shareholders. This high concentration of Nu Holdings’ voting power in the hands of Vélez means that we need to be comfortable with him at the company’s helm. We are.

On capability

We think Nu Holdings’ management team is exceptional when it comes to capability and innovation. Let’s discuss the capability angle first.

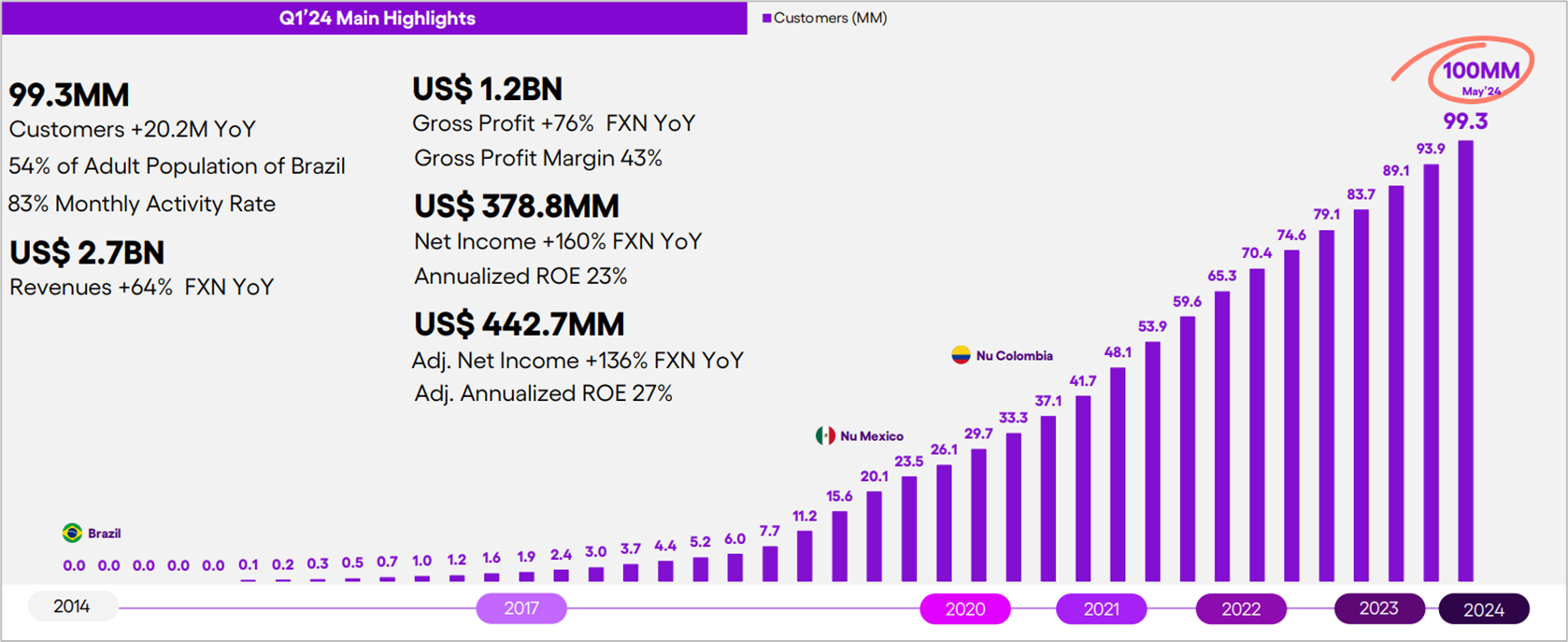

Earlier, we mentioned that Nu Holdings’ first-ever product – the purple Nu Credit Card – was launched only in 2014 and that it reached the impressive milestone of 100 million customers in May 2024. So, management has grown the company’s customer base impressively from zero to more than 100 million in merely a decade, as illustrated in Figure 2 below. Moreover, as we had also discussed previously, Nu Holdings had acquired, on average, 80%-90% of its customers each year since its inception from word-of-mouth or direct unpaid referrals from existing customers without the need for significant marketing expenses. Indeed, Nu Holdings’ customer acquisition cost was just US$6.50 per customer in 2022 and US$7 per customer in 2023 and the first quarter of 2024.

Figure 2; Source: Nu Holdings 2024 first-quarter earnings presentation

Nu Holdings’ recent growth rate in customers has slowed from the scorching pace in earlier years, but remains impressive. In 2023, the number of customers increased by 26% from 2022 while in the first quarter of 2024, the number of customers was up by 6% sequentially and 26% from a year ago.

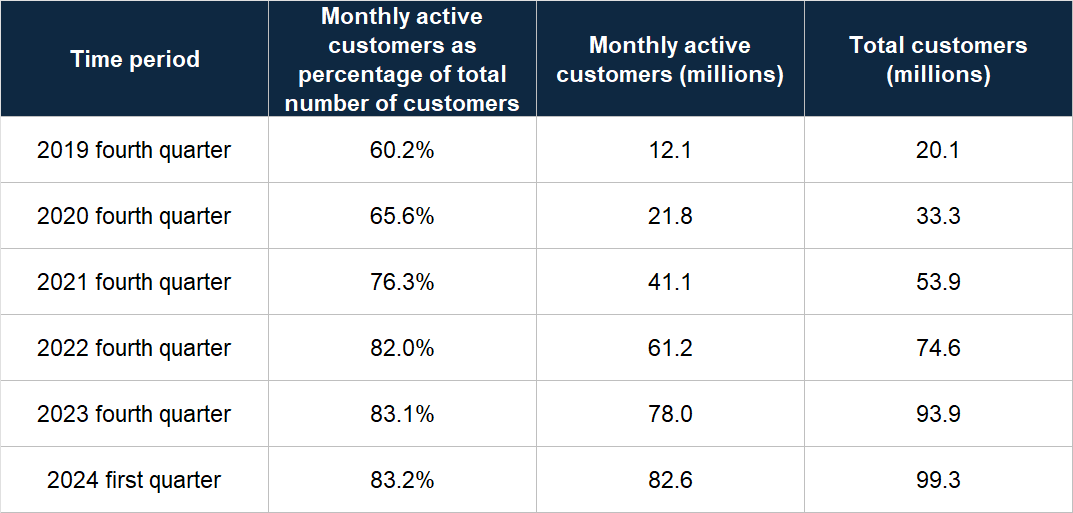

Growing the customer base alone is not enough – customer churn needs to be kept low (or Nu Holdings would have to constantly fill a leaky bucket) and the customers need to be actively using Nu Holdings’ products. On both fronts, management has excelled. Nu Holdings’ monthly customer churn has fallen from an already low rate of 0.5% in 2020 to just 0.2% in 2023. Meanwhile, Table 2 shows that the company’s monthly active customers as a percentage of total customers has increased substantially from 60.2% in the fourth quarter of 2019 to 83.2% in the first quarter of 2024.

Table 2; Source: Nu Holdings’ earnings updates

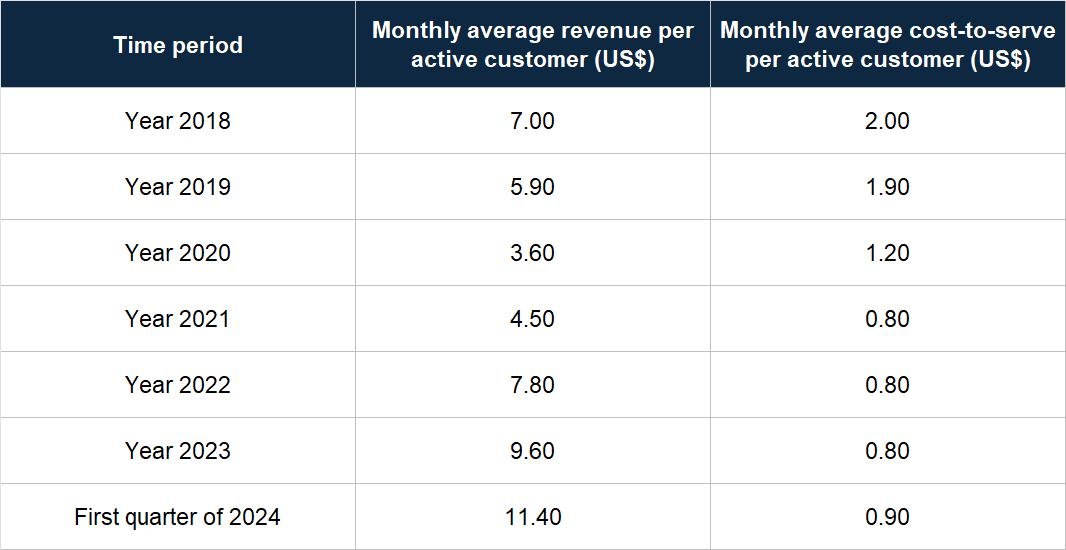

Besides growing Nu Holdings’ number of customers, management has also gradually increased the monthly average revenue per active customer (ARPAC) from an already high level. At the same time, the monthly average cost-to-serve per active customer has been kept low and has declined over time. These numbers are found in Table 3.

Table 3; Source: Nu Holdings IPO prospectus, annual reports, and earnings updates

There are three main factors behind the drop in the monthly ARPAC in 2019 and 2020. Firstly, the NuAccount was introduced in 2017 and allowed Nu Holdings to accept lower-income customers who would have been unable to start a relationship with the company through the Nu Credit Card. New customers who join Nu Holdings only through Nu Account tend to generate lower initial revenue than customers who sign up for multiple products from the start. Secondly, there was significant growth in customers in the few years prior to the affected periods, which increased the relevance of newer customer cohorts; new customers typically generate lower revenue for Nu Holdings. Lastly, in response to COVID-19, Nu Holdings’ management had reduced the initial credit limits for the Nu Credit Card for new customers to lower the company’s risk.

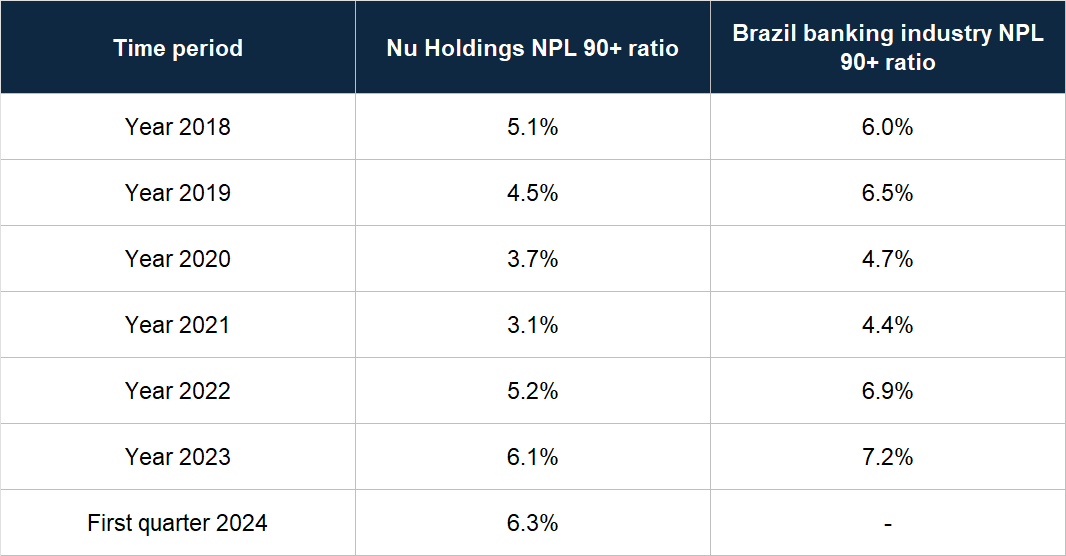

This brings us to what we think are the simple but highly effective ways management is handling credit risk for Nu Holdings. The first is the low-and-grow approach. This is where new borrowers with little to no available credit history are given lower credit limits by Nu Holdings that increase over time only with a positive track record of repayment. Nu Holdings has consistently outperformed Brazil’s banking industry when it comes to the 90-day consumer finance delinquency rate (aka the NPL 90+ ratio), as Table 4 displays. The NPL 90+ ratio compares the volume of loans that are late on repayment for 90 days or more, with the total volume of loans; the lower the ratio is, the better. Moreover, Nu Holdings’ management believes that the bank’s NPL (non-performing loans) ratios are consistently lower than those of Brazil’s banking industry across nearly all income segments, with the outperformance increasing from high to low incomes. It’s worth noting that management’s approach to lending is not to minimise NPLs, but to maximise the value of the loans Nu Holdings underwrites. So Nu Holdings’ NPLs can rise if management finds that the additional revenues that are earned from making riskier loans more than offsets the higher amount of delinquent loans – this was a dynamic that happened throughout 2023 (and continues today). And yet, Nu Holdings’ NPL 90+ ratio outperformed Brazil’s banking industry for the year. This makes Nu Holdings’ outperformance even more impressive. It’s also worth noting that Nu Holdings does not sell delinquent loans, so its NPL ratio is not artificially cleaned up.

Table 4; Source: Nu Holdings’ earnings presentations

The second way management handles credit risk is related to the way they model the performance of Nu Holdings’ loans. Management wants loans that can perform in both good times and bad, so they ensure that each borrower cohort can still produce a positive return even when the economy is modelled to become twice as bad than at the point the loans are made. In other words, management has never made loans with the assumption that economic conditions will get better – instead, the assumption is that the economy will become worse.

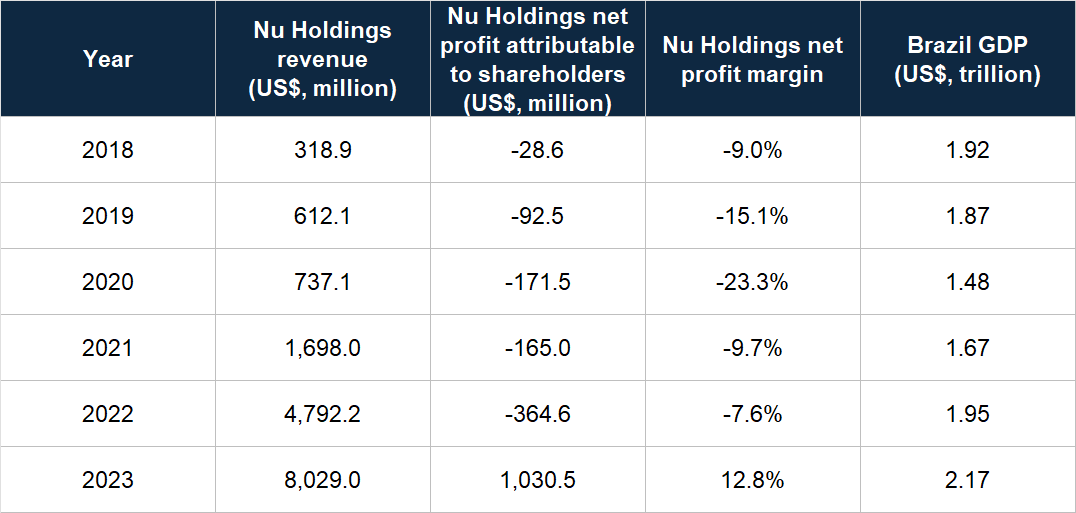

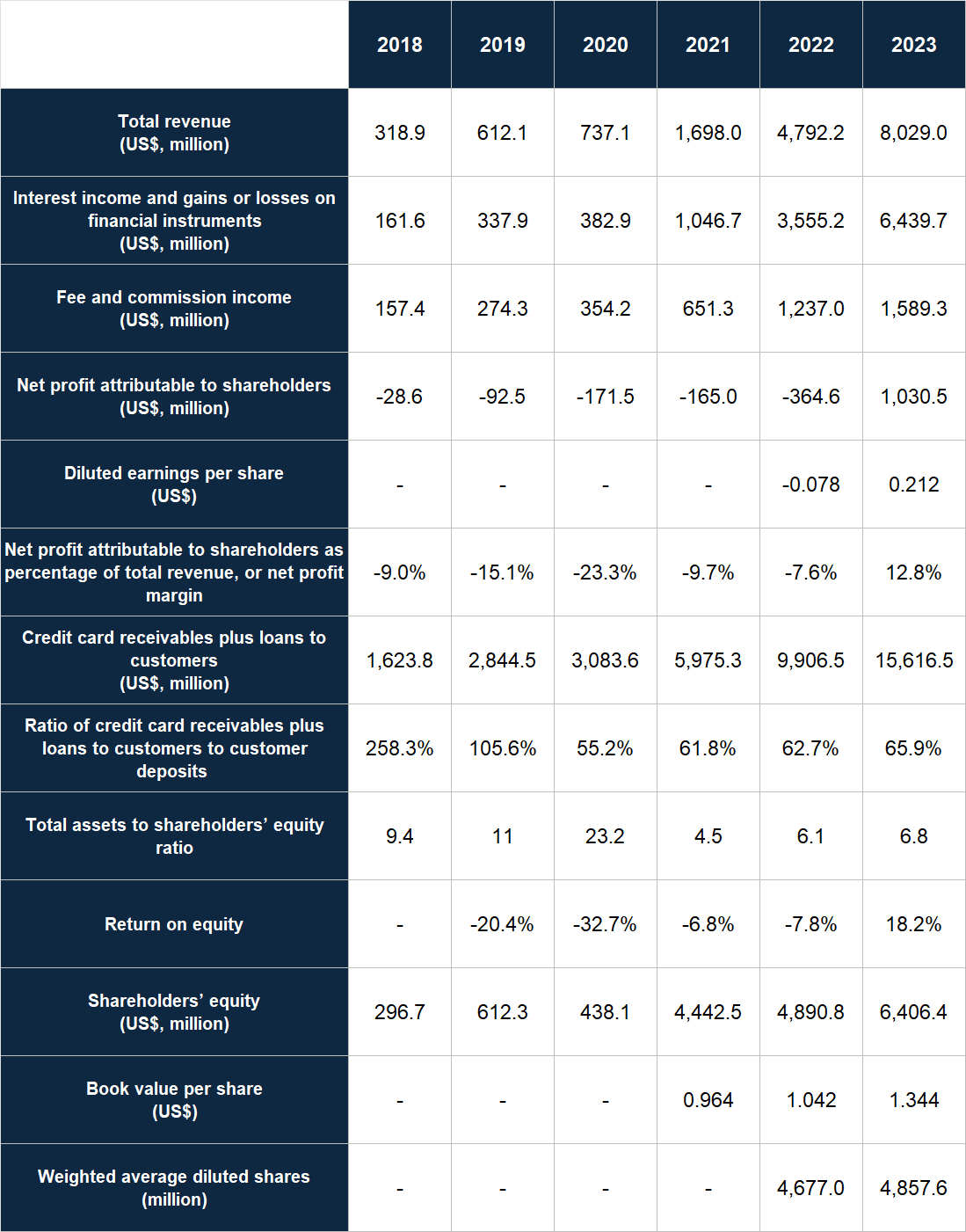

This is a good segue into Nu Holdings’ excellent historical growth in the context of Brazil’s economic performance, which we think underscores the capability of management. 2014, the year of Nu Holdings’ founding, also marked the start of a severe economic crisis in Brazil. The country’s GDP (gross domestic product) fell by 3.5% in 2015 and 3.6% in 2016 in Brazilian reais, according to the World Bank. It marked the steepest back-to-back recession the country has ever faced. Brazil’s economy started a slow recovery in 2017, only for COVID-19 to throw a wrench in the machine in 2020. World Bank data shows that Brazil’s economy was US$2.17 trillion in 2023, down from US$2.46 trillion in 2014. Although Nu Holdings’ main operational currencies are the Brazilian real, the Mexican peso, and the Colombian peso, it reports its financials in the US dollar. Table 5 juxtaposes the company’s excellent progress in revenue and net profit attributable to shareholders for 2018-2023 (2018 was the earliest year for financial data we could find for Nu Holdings) with the volatile and overall tepid growth in Brazil’s GDP in US dollars over the same period.

Table 5; Source: Nu Holdings’ annual reports and World Bank

We also think Nu Holdings’ management team is one that learns well from both successes and failures. This can be seen in the company’s progress in Mexico. The first quarter of 2024 marks 19 quarters since the company’s entry into the country and Figure 3 below shows Nu Holdings’ progress compared to its operations in Brazil also 19 quarters after launch.

Figure 3; Source: Nu Holdings 2024 first-quarter earnings presentation

Today, Nu Holdings’ Mexican business has, when compared to the Brazilian business when it was at the same age:

- A higher number of customers and higher market share

- Higher market share of active credit card customers

- Significantly higher number of active Nu Accounts, and a much higher market share

- Nearly half as much credit card purchase volume but a higher market share

- Much higher market share for, and amounts of, customer deposits

- An interest earning earning portfolio that’s double in size

- Materially higher revenue

During Nu Holdings’ 2024 first quarter earnings conference call, management said that the data in Figure 3 suggest that the company is “building a model that could be successfully exported, a feat many previously deemed unachievable in consumer finance.” We agree.

On innovation

Coming to the innovation angle, we think Nu Holdings’ management team excels here because of their astute use of technology, their refreshingly long-term approach to running the business, and their history of consistently launching new products.

On the technology front, here are some highlights:

- Nu Holdings designed and built its proprietary, cloud-based core banking platform, NuCore, from the ground up and it powers all of the company’s products and operations.

- Nu Holdings employs a decentralised technology architecture to manage and deploy over 500 modular microservices that it has developed. The microservices architecture is an approach to software development that emphasises the use of small independent pieces of software that communicate with each other through well-defined APIs (application programming interfaces). This tends to improve the speed of development of applications and the ease of their scaling. By adopting a microservices architecture, Nu Holdings has been able to scale, launch new products, enter new markets, and update its codebase, quickly and efficiently.

- Nu Holdings created its own advanced, immutable ledger with the Datomic database technology that it self-developed. Being a digital bank, it goes without saying that having accurate data is of utmost importance for Nu Holdings and this is why having an immutable ledger is critical. There are other useful features that Datomic brings to the table, but there’s one we find particularly useful because it improves the company’s capabilities in artificial intelligence; Federico Sandler, the aforementioned previous investor relations officer of Nu Holdings, mentioned the following in a recent post on the social networking platform X (emphasis is ours):

“Datomic also captures database transactions as entities in the database. This powerful feature provides timestamps and extensible metadata associated with every write and captures information that engineers rarely think to model explicitly. This metadata, combined with the data itself, provides the basis for novel machine learning features and assists in ensuring operational correctness.”

- Another recent post on X by Sandler mentioned Clojure, a programming language used by Nu Holdings. Although Clojure is less commonly used, it has strong advantages. According to Sandler, Clojure is a simpler programming language that is less prone to errors and this allows Nu Holdings to deploy code rapidly. There are good pieces of evidence supporting this point of view: (1) Nu Holdings has been deploying new software code at an increasing pace in recent years, with its average daily code deployments increasing from 120 in 2021 to 180 in 2022 and 275 in 2023; (2) the company has a history of consistent product innovation, which we will discuss shortly.

- Nu Holdings currently collects more than 30,000 data points per monthly active customer, up from 9,000 data points at the end of 2021. These data feed into the company’s internally developed NuX Credit Engine, which allows the company to reduce risk with its lending activities. The NuX Credit Engine is self-learning and becomes more powerful with more data. A proof point on the capabilities of the NuX Credit Engine can be seen in Nu Holdings’ superior NPL ratios that we discussed earlier.

- In Mexico, where financial inclusion is at one of the lowest levels in the world, Nu Holdings is already running the sixth generation of its proprietary machine-learning underwriting models. The model lowers risk by 70% for a comparable approval rate when compared to generic credit bureau scores, which allows Nu Holdings to accept new customers at a meaningfully higher rate. As proof of the quality of the underwriting models, Nu Holdings’ first payment default rate in Mexico has dropped from 7.4% in 2020 to 5.7% in 2022 and 3.1% in 2023.

- According to a recent internal interview of Vitor Olivier, Nu Holdings’ current Chief Technology Officer, the company has been using AI models in its interactions with customers for some time, even before generative AI rose into the public’s consciousness in late-2022. He also said that after Nu Holdings started deploying generative AI for customer interactions, he has seen a doubling to tripling in customers’ self-service rates.

Regarding management’s long-term approach to running the bank, it’s aptly illustrated in a story that David Vélez shared in his aforementioned internal interview (emphases are ours):

“A couple of years ago we had an analyst that came and said, “Hey, we’re suddenly making more money per customer.” Our cohorts were tilting up very fast. And we went in and took a look and see what was happening. And it turns out that there had been a bug in our system and we had stopped sending a reminder email to our customers. Since the beginning – being we care about the values – we remind the consumer almost every day to pay on time. We don’t want them to revolve unnecessarily. So we remind the consumers and only the ones that really need to revolve will end up revolving and pay a late fee. So for us, having that consumer value was very easy to know what to do. Not only we had to go back and put that email immediately, but also go beyond and send an email to all of our customers and apologize for having stopped reminding them to pay on time and reimburse that fee.

Now here some people might ask, “Well, what are you? Are you not for profit? You’re not going to make that much money anymore. How is this consistent with long-term value creation?” And our view is that they’re actually completely consistent, in the long run. In the long run, that customer that has just received an email from Nubank apologizing for having done something that they didn’t need to do and reimbursing that money will say, “Wow, this is a fundamentally different experience.” And we have just earned a customer for the next 50 years. So that trust is extremely valuable and in the long run, sending that reminder email might make us make less money in the short-term but will help us have a customer working with us for a longer run. And that’s how that value and that strategy are completely consistent with each other and with maximizing for shareholder value in the long run.”

In essence, Vélez strikes us as a leader who believes that proactively delivering as much value as possible to customers, even if doing so would be a short-term negative for Nu Holdings, is the right thing to do for building the company’s long-term value. We agree. The story also reminds us of what Jeff Bezos wrote in Amazon’s 2012 shareholders’ letter (this is the second similarity Nu Holdings shares with Amazon):

“Proactively delighting customers earns trust, which earns more business from those customers, even in new business arenas. Take a long-term view, and the interests of customers and shareholders align.”

Nu Holdings’ adoption of PIX, the aforementioned 24/7, instant payment system launched in late-2020 by the Central Bank of Brazil, is another example of Vélez’s willingness to tolerate short-term pain for longer-term gain. In the “Company description” section, we highlighted the importance of the Nu Credit and Debit Card product with its direct weightage of at least 46.2% of Nu Holdings’ revenue in 2023. The product was even more important during Nu Holdings’ earlier days; for instance the product directly accounted for at least 76.8% of Nu Holdings’ total revenue in 2018. Pix is free to use for individuals, and according to reporting by Reuters in April this year that cited a Bank of International Settlements (BIS) paper, PIX costs an average of 0.22% per transaction for merchants, compared to debit and credit fees that range from 1% to 2.2% per transaction. Nu Holdings also does not earn fees for PIX payments that it processes. So on the surface, and in the short-term at least, adoption of PIX by Brazilian citizens and businesses is a headwind for Nu Holdings. Yet, Vélez was willing to embrace PIX, to the extent that Nu Holdings is now a market leader in the number of registered and active PIX keys in Brazil and had a market share of PIX transfers of 10% at the end of 2023; moreover, more than 35% of Nu Holdings’ active credit card customers were active PIX users at the same point in time. This was because Vélez saw PIX’s strategic value as a way to add customers, increase engagement, and act as a platform for future cross-selling. Here’s Olivier’s description in his aforementioned interview (emphases are ours):

“Jörg Friedemann [Nu Holdings’ investor relations officer]: Listening to you, it reminds me about PIX, which was faced by many parts of the industry as a cost only.

Vitor Olivier: Yes.

Jörg Friedemann: We always face that as a savings opportunity first and then as a revenue driver, and I think it’s proven right, as PIX financing scales every day.

Vitor Olivier: That’s the best comparison that we can give, which is PIX objectively is good for customers. If you can make a transfer that’s free 24/7, reliable, that changes your relationship with money. It enables businesses that couldn’t exist, it removes and reduces the barrier of entry into the formal economy in a way that no technology has ever done. It’s a transformational technology. And if you just look at it as the first step, the first step is the players that were charging for wire transfers – we never charged for it – but there are players that were charging for it. The first thing they’re going to look at, it’s like, this is a big cut in my revenue line and you fight against it. Or, we’re not going to adopt it, or, this is not going to be good, and so on. And it’s understandable why that’s the gut reaction. But we saw it as, it’s good for customers, great. They’ll come back. They need to love it. They need to love doing it with us. And if they do it with us, then maybe we earn the right to offer something else, other value propositions around it. And I think PIX financing is a great example of that.”

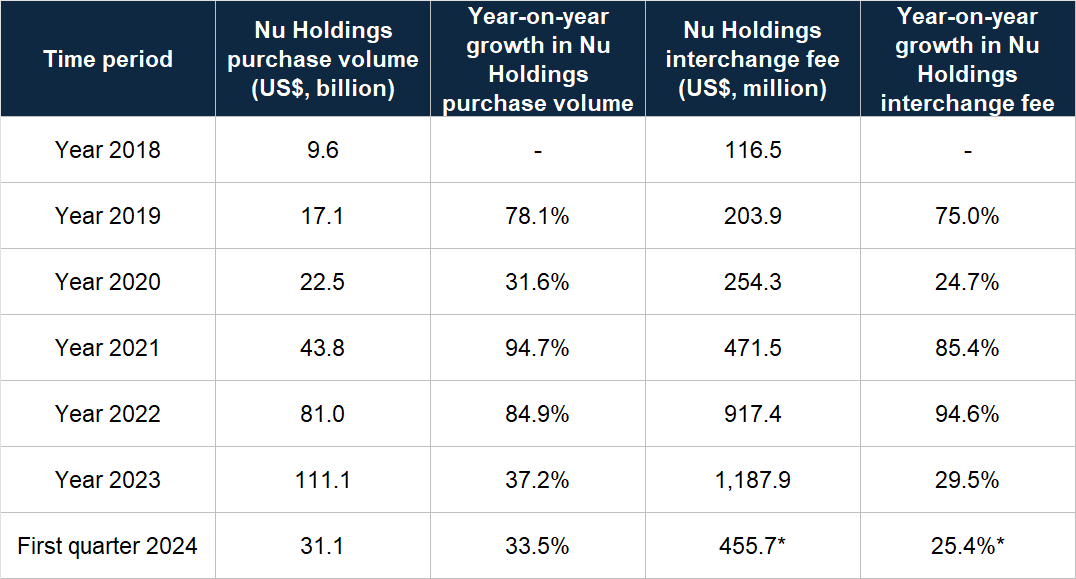

We also want to highlight that embracing PIX has not stopped Nu Holdings from growing its business. PIX was launched by Brazil’s central bank in late-2020 and was integrated by Nu Holdings before the end of the year. Table 6 below contains data on the continued growth of the company’s purchase volume and interchange fee before and after the introduction of PIX to its ecosystem; the purchase volume is the total volume of transactions made with the Nu Credit and Debit card from which Nu Holdings earns interchange fees.

Table 6; Source: Nu Holdings IPO prospectus, annual reports, and earnings updates (*the interchange fee and year-on-year growth rate in interchange fee for the first quarter of 2024 refers to fee and commission income; the growth in fee and commission income in the quarter was driven mainly by interchange fees)

Coming to management’s history with consistent product innovation, here’s a great summary from Nu Holdings’ latest annual report:

Figure 4; Source: Nu Holdings 2023 annual report

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

At the moment, Nu Holdings’ main business is to provide products to individuals and SMEs for the Five Financial Seasons of spending, saving, investing, borrowing, and protection. These are products that we think individuals and businesses in the entire Latin American region require on a frequent basis, sometimes daily. So there should be high levels of recurring business activity for Nu Holdings.

5. A proven ability to grow

In our explanation of this criterion, we mentioned that we’re looking for “big jumps in revenue, net profit, and free cash flow over time.” For Nu Holdings, however, our focus is on its net income per share and book value per share. The latter in particular, is a key measure of a bank’s intrinsic value. The table below shows Nu Holdings’ important financial numbers from 2018 to 2023 (2018 was the earliest year for financial data we could find, given that Nu Holdings’ IPO was only in December 2021).

Table 7; Source: Nu Holdings IPO prospectus and annual reports

A few things to highlight from Nu Holdings’ historical financials:

- Total revenue grew in each year from 2018 to 2023 and compounded at a remarkable annual clip of 90.6%. The growth rate in 2023, while slower, remained strong at 67.5%.

- The two major categories of Nu Holdings’ revenue both grew rapidly too. For the 2018-2023 period, the compound annual growth rates (CAGRs) for interest income and gains or losses on financial instruments and fee and commission income were 109.0% and 58.8%, respectively. In 2023, they grew by 81.1% and 28.5%. Over time, the lending operations of Nu Holdings – represented by the interest income and gains or losses on financial instruments revenue stream – has grown in importance for the company.

- Net profit attributable to Nu Holdings’ shareholders was negative for the most of the period and turned positive only in 2023. But the net profit margin was moving in the right direction from 2020 onwards. There are two important things to highlight here regarding the net profit margin:

- Firstly, Nu Holdings’ net profit margin for 2022 would have been much closer to zero if not for David Vélez’s aforementioned termination of his 2021 CSA. Management expected Nu Holdings to achieve aggregate savings of US$356 million in the seven years following the decision, because the continuous accounting recognition of the potential future grant will no longer be required. But there was also a one-time, non-cash expense of US$356 million in the fourth quarter of 2022 associated with the termination of the 2021 CSA that accounting regulations require to be booked even though there was no actual vesting of the award.

- Secondly, accounting regulations require Nu Holdings to frontload credit losses as soon as a loan is granted even though management expects these loans to still generate revenue over time. This regulation means that Nu Holdings’ profit margins suffer a drag whenever it’s growing its loan book. And grown the loan book it has – Nu Holdings’ credit card receivables and loans to customers have increased nearly 10-fold from US$1.62 billion in 2018 to US$15.62 billion in 2023. Despite the practice of frontloading credit losses, the true profitability of Nu Holdings’ lending business may be overstated if the actual credit losses are greater than what has been provisioned. But in Nu Holdings’ case, the growth in the recovery of credit loss allowances has actually been faster than the growth of its loan book, suggesting that the frontloading of credit losses has been unduly punishing Nu Holdings’ profitability; from 2018 to 2023, the recoveries of credit loss allowances has increased by 14-fold from US$14.1 million to US$203.4 million.

- Nu Holdings’ loan-to-total deposits ratio was very high in 2018 but has since stepped down to a robust level of 65.9% in 2023. The loan-to-deposit ratio is a measure of liquidity risk a financial institution is facing, and the lower it is, the better. The term “loan” here refers to the sum of Nu Holdings’ credit card receivables and loans to customers. We want to highlight that the loan-to-deposit ratio we are presenting somewhat overstates the actual situation. This is because only a portion of the company’s credit card receivables are interest-earning (and so constitutes a loan). But we included the entire credit card receivables in our calculation because Nu Holdings is still on the hook to pay merchants on behalf of its credit card customers even if the customers fail to pay.

- Shareholders’ equity declined in 2020 mostly because of the negative net profit attributable to shareholders for the year. There was a large spike in shareholders’ equity in 2021 because of the company’s IPO. The other big spike, in 2023, happened largely because of the net profit earned during the year.

- Book value per share was not meaningful prior to Nu Holdings’ IPO. In 2022 and 2023, the company’s book value per share was up by 8% and 29%, respectively. The growth in 2022 is also not meaningful because the company still generated a loss, but the strong growth in 2023 is a welcome sight.

- Nu Holdings has largely not taken on undue risk for the timeframe we’re studying because its total assets to shareholders’ equity ratio was less than 11 for all the years we’re looking at, except for 2020, and it was only at 6.8 in 2023.

- Nu Holdings’ return on equity was negative for most of the years under review because it was still generating losses. But in 2023, its return on equity was a respectable 18.2%. There are strong reasons for us to believe that Nu Holdings’ return on equity will improve materially in the future – we’ll discuss this in the “A high likelihood of generating a strong and growing stream of free cash flow in the future” sub-section.

- Nu Holdings’ weighted average diluted share count is not meaningful in the years prior to its IPO as well as in 2021 (the company was listed only in December of the year, so its weighted average diluted share count is much lower than the actual number of shares that existed right after the listing). In 2023, the company’s weighted average diluted share count increased by 3.9%. We would have preferred a lower number, but the company’s outstanding revenue growth over time, and strong growth in book value per share in 2023, more than makes up for it.

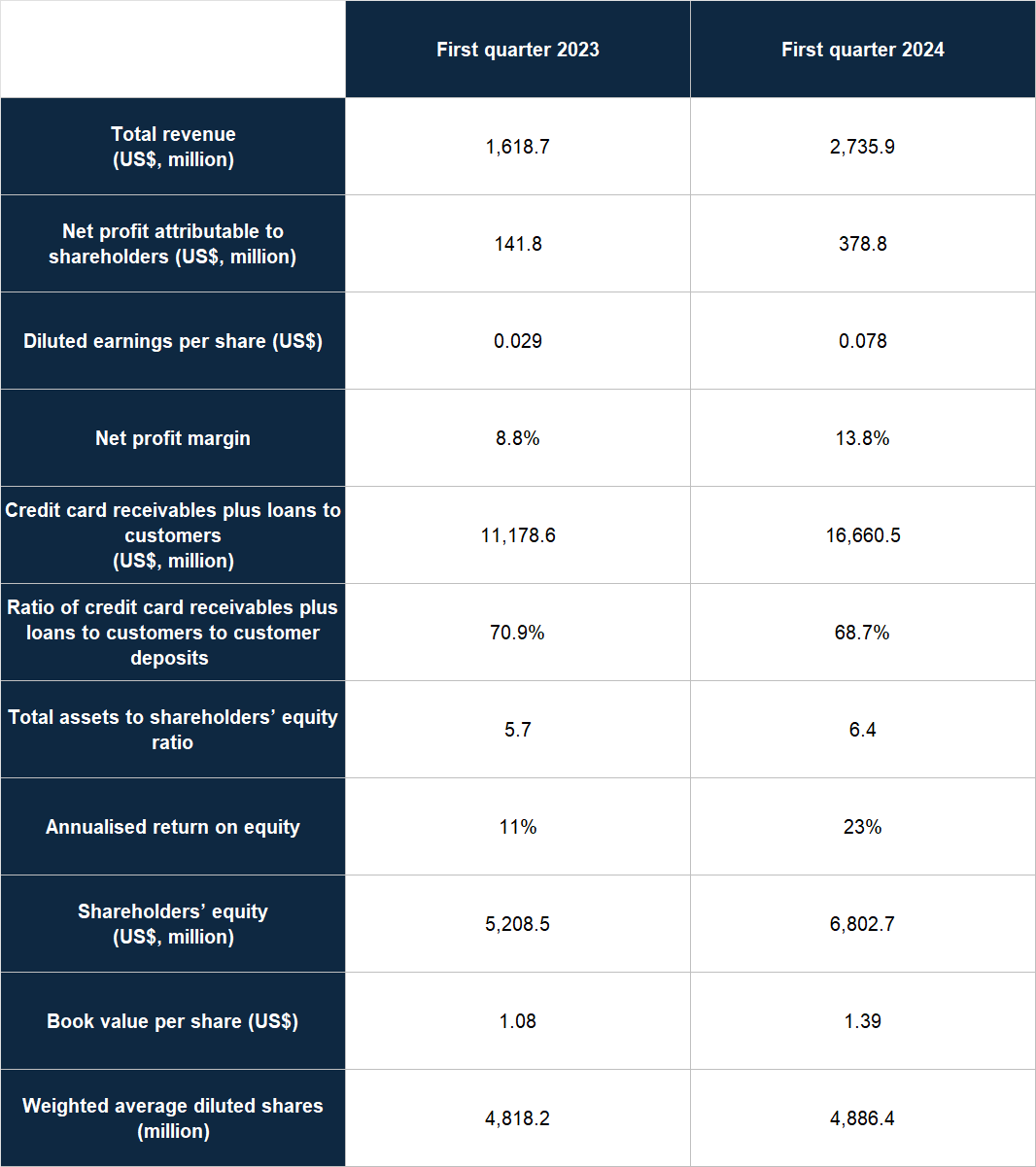

Table 8; Source: Nu Holdings quarterly earnings updates

Nu Holdings has continued to post excellent revenue growth of 69.0% in the first quarter of 2024, as illustrated in Table 8 above. The table also shows a few more things:

- Nu Holdings generated a positive net profit attributable to shareholders, along with impressive growth of 167.2%; earnings per share was similarly up by 163.6%

- There was a healthy increase in the net profit margin (from 8.8% to 13.8%)

- The loan book – consisting of credit card receivables and loans to customers – continues to expand

- The loan-to-deposit ratio remains healthy at 68.7%

- The total assets to shareholders’ equity ratio, or leverage ratio, is still at a low level of 6.4 (a good thing!), as mentioned earlier in the “A strong balance sheet with minimal or a reasonable amount of debt” subsection

- The annualised return on equity improved significantly from 11% to 23%

- Book value per share was up by an excellent 28.7%

- Dilution remains acceptable, with the weighted average diluted share count increasing by just 1.4% year-on-year

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Because Nu Holdings’ main business is currently to run a digital bank, the concept of free cash flow is not as important. What we’re concerned with is the future growth in its earnings per share and book value per share. We believe Nu Holdings is well-positioned to achieve substantial growth in both financial metrics in the coming years, driven by a few factors:

- The potential for significant market-share gains in the financial services markets in Brazil, Mexico, and Colombia. This was detailed in the “Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market” subsection

- David Vélez and his team have demonstrated integrity and a strong track record of successful innovation and business growth, as we established in the “A management team with integrity, capability, and an innovative mindset” subsection.

- A high possibility for the company’s economics to improve in the future:

- Nu Holdings had excess capital of US$2.4 billion at the holding level in the first quarter of 2024 when its shareholders’ equity was US$6.8 billion.

- The company’s annualised return on equity in the first quarter of 2024 was 23% despite its operations in Mexico and Colombia currently still being loss-making; the return on equity of the Brazil business alone was “well above 40%.”

- In a May 2024 interview with Bloomberg, Vélez said that around 50% of the company’s employees “today are working on products that are generating zero revenue.” If any of these products succeed in becoming profitable, it likely would improve Nu Holdings’ overall profitability.

- In the “A management team with integrity, capability, and an innovative mindset” subsection, we mentioned that Nu Holdings has maintained a low monthly average cost-to-serve per active customer while growing its monthly ARPAC significantly over time. Moreover, mature customer cohorts have a monthly ARPAC of around US$27 per month, more than twice that of the company-wide monthly ARPAC of US$11.40 per month.

- When only the interest-earnings portion of Nu Holdings’ credit card receivables and loans to customers are considered, the company’s loan-to-deposit ratio was just 40% in the first quarter of 2024. Nu Holdings’ excess deposits are invested in public bonds, which have much lower yields than its lending products. As management puts more of the deposits to work in Nu Holdings’ lending products, the company’s profitability should trend upwards.

Valuation

We like to keep things simple in the valuation process. In Nu Holdings’ case, we think the price-to-book (P/B) and price-to-earnings (P/E) ratios are suitable gauges for the company’s value. We completed the initial purchase of Nu Holdings’ shares for Compounder Fund in late-June 2024. Our average purchase price was US$12.71 per share. At our average price and on the day we completed our purchase, Nu Holdings’ shares had trailing P/B and P/E ratios of 9.1 and 48.9, respectively. These valuation ratios look high optically. But we think they are reasonable for a high-ROE digital bank that is likely to compound its book value per share and earnings per share at a rapid rate in the coming years.

For perspective, Nu Holdings carried trailing P/B and P/E ratios of 9.3 and 49.9 at the 22 July 2024 share price of US$12.99.

The risks involved

All investments carry risk and Nu Holdings is no exception. A few important ones we’re watching include:

- Key-man risk: We think David Vélez, the brainchild behind Nu Holdings and its long-time CEO, has been a key architect of the company’s past successes. If he should leave the company for any reason, we’ll be watching the leadership transition. The good thing is he’s still young at 42, so he’s likely to still have plenty of gas left in the tank to lead Nu Holdings in its quest to provide better financial products for the people of Latin America.

- Political and economic volatility in Latin America: Nu Holdings’ key geographical markets are not the most stable countries in the world, in both the political and economic realms. Over the past five years, the Brazilian real and the Colombian peso – two of the company’s three main operational currencies – have depreciated significantly against the US dollar, by roughly 30% and 20%, respectively. Over the past decade, the depreciations are even more pronounced at around 60% and 50%. Political instability can be seen in the unfortunate murders of at least 256 Brazilian politicians from 2017 to 2020; in another instance, Reuters reported that “From September [2023] to May [2024], across Mexico, 34 candidates or aspiring candidates have been assassinated.” Despite these challenges, Nu Holdings has thrived, with its revenue surging five fold from US$1.7 billion in 2021 to US$9.2 billion in the 12 months ended 31 March 2024. But this increased scale may leave the company more strongly tethered to any future economic and political turmoil in its key markets.

- Low-hanging fruits may already be harvested: Nu Holdings had 91.8 million customers in Brazil as of the first quarter of 2024. This was 54% of the country’s adult population. There’s a possibility that Nu Holdings has already signed up the majority of adults in Brazil who are good customers (customers who would not default on their loans en masse). If this is true, Nu Holdings’ future growth would be stunted at best, while credit losses could pile up in the future, threatening the company’s survival, at worst.

- High valuation: We have confidence in Nu Holdings’ ability to grow its business at a rapid clip for many years. But it has a high valuation. So if there are any hiccups in its business – even temporary ones – there could be a painful fall in the share price. This is a risk we’re comfortable taking as long-term investors.

- Changes to the digital payments landscape: We established in the “Company description” section that the Nu Credit and Debit Card is a core product for the company. The Central Bank of Brazil is working on advancements for PIX while Mexico has launched two PIX-equivalent systems in recent years, with CoDi in 2019, which did not catch on, and DiMo in 2023. Meanwhile, Colombia’s central bank introduced new rules in late-2023 that set the stage for a similar system to PIX. These developments may become severe obstacles in Nu Holdings’ pursuit of future growth. So far, the company has held its own admirably. There’s also the risk of Nu Holdings’ business being hurt by future changes in regulations that lower the interchange fees and/or interest rates on credit card debt that financial institutions in Latin America can charge. In 2022, the Central Bank of Brazil lowered the limits on interchange fees for debit cards and the change came into effect in April 2023. But Nu Holdings has continued to produce good growth in its interchange fees, as we showed in the “A management team with integrity, capability, and an innovative mindset” subsection. As for changes in interest rates on credit card debt, the Central Bank of Brazil introduced a new regulation in October 2023, with an effective date of 3 January 2024, that capped the total amount of interest and charges on credit card debt at the original debt value; as far as we can tell, there have so far been no material impacts to Nu Holdings’ business from this change. Brazil’s finance regulators also held a meeting in April this year with banking executives, including those from Nu Holdings, to discuss placing a limit on the monthly interest rate charged on credit card debt. No decision has been made yet, but any new limits on credit card interest rates could be a negative development for Nu Holdings in the short term at least. We’re watching how the situation unfolds, but the good thing is management has successfully reduced Nu Holdings’ reliance on the Nu Credit and Debit Card product over time.

Although it is not necessarily a risk, we acknowledge the fact that Nu Holdings’ principal office is in the Cayman Islands, which is a completely different jurisdiction from the Brazilian city of São Paulo where its main operational headquarters are located. To be clear, we believe that Nu Holdings’ situation is different from that of Chinese technology companies that use a variable interest entities (VIE) shareholder structure. Under the VIE structure, shareholders of a Chinese technology company do not own the China businesses directly, but rather, own entities domiciled in the Cayman Islands that receive economic benefits from the China business through a series of contracts. In contrast, Nu Holdings’ operations in Brazil, Mexico, and Colombia that we have been discussing throughout this thesis are run directly by subsidiaries owned by the company. We currently don’t see any potential problems in the horizon for Nu Holdings because of the different geographies its principal office (Cayman Islands), main operational headquarters (Brazil), and the stock market where its shares are traded (USA), are in. But we cannot rule out the possibility of any complications popping up in the future because of this.

Summary and allocation commentary

To sum up Nu Holdings, the Latin American digital banking powerhouse has:

- Massive growth opportunities, in the form of Brazil, Mexico, and Colombia’s combined US$200 billion financial services market

- A robust balance sheet with its total assets to shareholders’ equity ratio of just 6.4 in the first quarter of 2024

- A management team, led by David Vélez, with significant skin-in-the-game, a decade-long track record of excellent execution and innovation, and a refreshingly long-term approach to running the business

- Recurring business from the nature of the products it provides for the Five Financial Seasons of spending, saving, investing, borrowing, and protection

- A relatively short but excellent history of revenue growth, coupled with material improvement in profitability

- A high likelihood of growing its book value per share and earnings per share rapidly in the coming years.

As it is with every company, there are risks to note for Nu Holdings. The main ones we’re watching include: Key-man risk; political and economic instability in Latin America; the possibility that the supply of desirable customers has been exhausted; valuation risk; and potential negative changes to the digital payments landscape in Brazil, Mexico, and Colombia.

After weighing the pros and cons, we decided to initiate a position of around 1.9% in Nu Holdings in late-June 2024. Our initial position in Nu Holdings can be considered to be a mid-sized allocation. We appreciate the strengths we see in Nu Holdings’ business, especially the quality of the management team and the advantages the company holds over incumbent banks. But we’re also wary of the high valuation and the risks that come with operating in a volatile climate such as Latin America.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all other companies mentioned in this article, Compounder Fund also owns shares in Adyen and Amazon. Holdings are subject to change at any time.