Compounder Fund: Illumina Investment Thesis - 08 Jan 2021

Data as of 7 January 2021

Illumina Inc (NASDAQ: ILMN), which is listed and headquartered in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

To fully appreciate Illumina’s business, we first need to understand what is genetics and where Illumina fits into the puzzle of the genetics revolution.

The “instruction set” for all living organisms are contained in a molecule called deoxyribonucleic acid, or DNA. It comprises chemical building blocks called nucleotides, which come in four different types of bases, namely: adenine (A), thymine (T), guanine (G), and cytosine (C). The order of how the four bases are arranged determines the different biological instructions that come in a DNA strand, and accounts for the differences among organisms.

The term ”genome” refers to the complete set of DNA for an organism. So, the complete set of DNA for a human would be the human genome. In 1990, the US government launched an ambitious 15-year study to map the entire human genome at an estimated budget of US$3 billion. The Human Genome Project, as the study was called, was eventually completed two years ahead of schedule, and cost US$2.7 billion.

Within the genome are genes, which are the basic physical and functional units of heredity. Genes contain the instructions needed to make proteins, which are the molecules that direct all cellular function. In humans, genes can be as small as a few hundred bases, or as large as over 2 million bases. Results from the Human Genome Project estimate that humans have 20,000 to 25,000 genes.

The human genome consists of 3 billion nucleotides. But only 1% or so of the human genome contain instructions for making proteins. The pieces that contain the instructions are known as exons, and all the exons in a genome are known as the exome.

Genetic variations in humans account for the differences we can physically observe between people, such as hair colour, eye colour, skin tone etc. But more importantly, the genetic variations also have medical consequences, including predisposition to genetic diseases (such as cancer, diabetes, and Alzheimer’s disease, for instance) and variances in responses to drug treatments. Scientists are conducting research on these genetic variations and consequences in humans, animals, plants, and even microorganisms. This is where Illumina, which was founded in 1998, comes in.

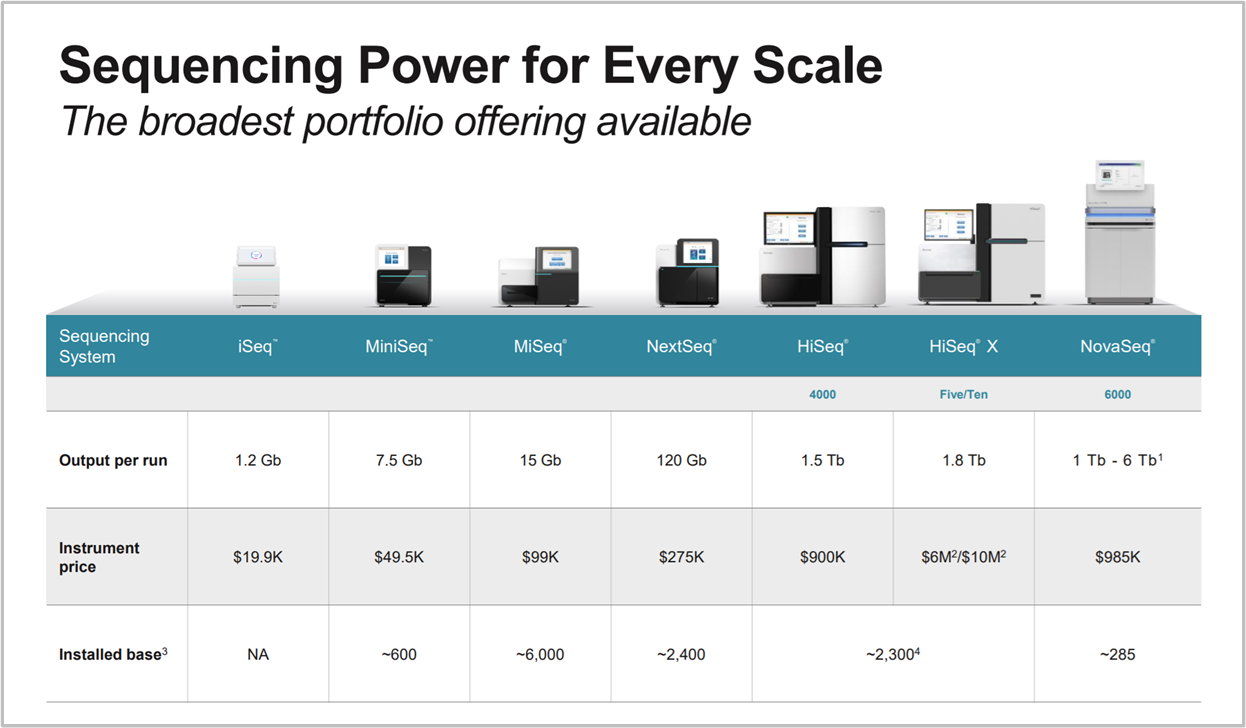

Illumina develops, manufactures and sells machines that analyse the genome at all levels of complexity, from targeted panels to whole-genome sequencing. The chart below, from a May 2018 Illumina investor presentation, provides a good overview of the different machines that Illumina offers. The company’s machines come with a wide variety of price points (ranging from tens of thousands of dollars, to the millions of dollars) and capabilities (in terms of the output for DNA analysis).

Source: Illumina 2018 May investor presentation

In addition, Illumina also sells consumables that are used together with its machines. These consumables include reagents, flow cells (essentially high-tech glass plates that are used to study DNA), and microarrays (a platform for assessing known markers within the human genome).

In the first nine months of FY2020 (the fiscal year ending late-December 2020 or early-January 2021), Illumina earned US$2.29 billion in revenue. Instrument sales accounted for 12.5% of the total, while consumables took up the majority at 70.8%. The remaining 16.7% came from the Service and Other revenue category, which comprises services such as whole-genome sequencing, genotyping, non-invasive prenatal testing, and more.

Illumina’s products are used for life sciences research by universities, research centres, government institutions, and biotechnology and pharmaceutical companies. The company’s products also serve applied markets, such as consumer genomics and agrigenomics. In consumer genomics, Illumina’s customers use its machines to provide personalised genetic data and analysis to individual consumers, for instance. In agrigenomics, customers use Illumina’s products to study crops and livestock. Illumina’s machines are also used in a clinical setting. For example, the company’s customers in the translational and clinical oncology markets use its products for research on cancer. In all, the customers that Illumina serves exposes the company to a wide variety of markets, shown in the chart below:

Source: Illumina 2018 May investor presentation

Source: Illumina 2018 May investor presentation

From a geographical perspective, Illumina is pretty diversified. In the first nine months of FY2020, 54.6% of its revenue came from the USA. The rest were from Greater China (10.8%), Asia-Pacific (8.3%), and Europe, Middle East, and Africa (26.3%).

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Illumina.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

During an Investor Day event in 2014, Illumina shared that its collective opportunity for DNA sequencing – involving all the different markets it is exposed to – was US$20 billion. This is significantly larger than Illumina’s revenue of US$3.24 billion for the 12 months ended 27 September 2020. Although we don’t have more recent data on the size of Illumina’s market, we have good reason to believe that the market opportunity has real potential to be much larger in the years ahead.

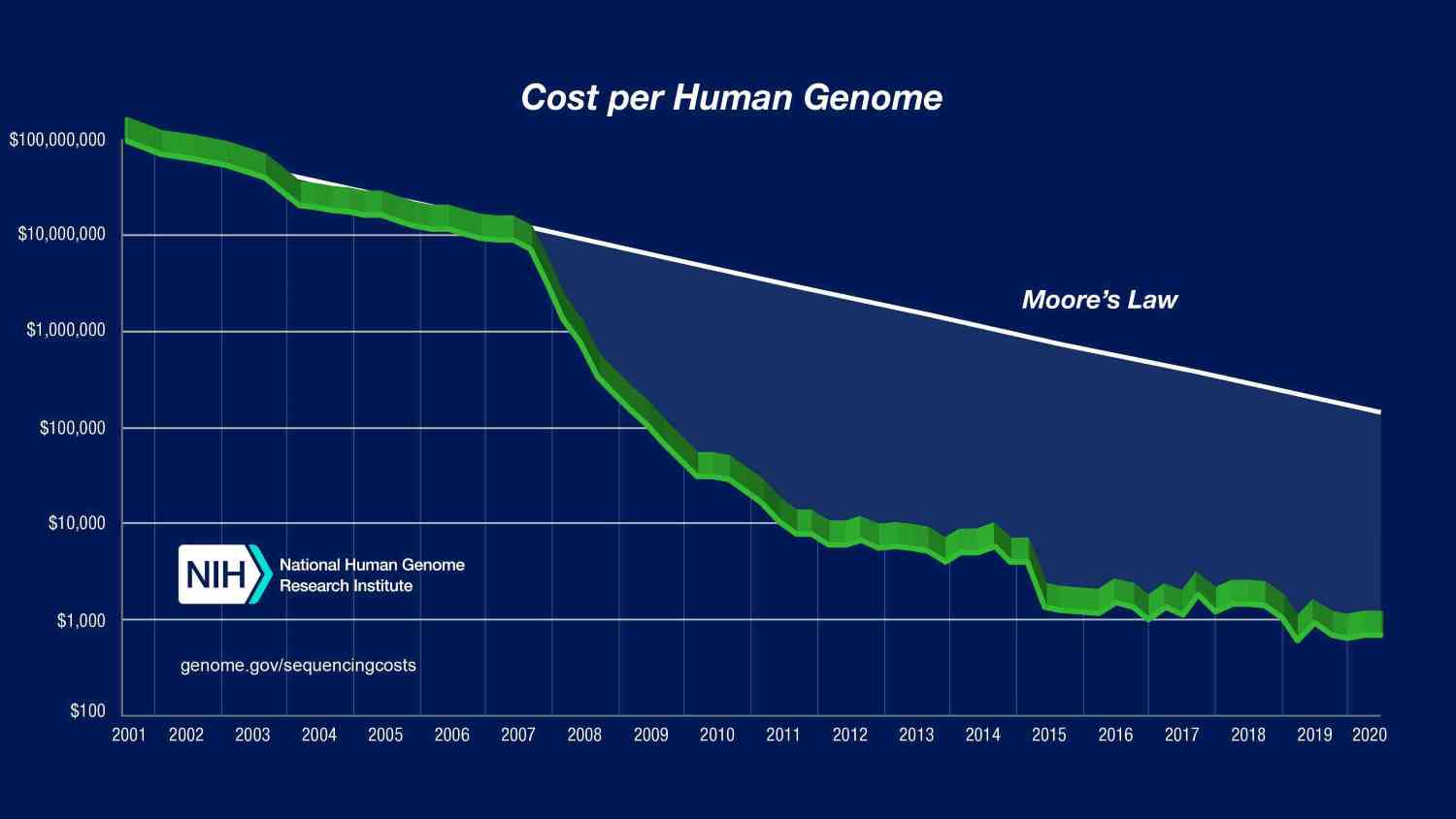

This reason is Illumina’s incessant efforts to make DNA sequencing increasingly affordable and faster. Remember the US$2.7 billion, 13-year Human Genome project to map out the human genome that we brought up earlier? If this project was done today, the cost and time needed would be significantly lower, thanks to Illumina. Prior to 2007, the year Illumina launched its first-ever DNA sequencing system, the cost of sequencing a genome was declining at a rate that closely matched Moore’s Law (for our purposes, Moore’s Law can be loosely interpreted as an improvement in sequencing costs by a factor of two, every two years). Interestingly, after 2007, sequencing costs plummeted faster than the trajectory of Moore’s Law. You can see the cost changes in the chart below:

Source: National Human Genome Research Institute

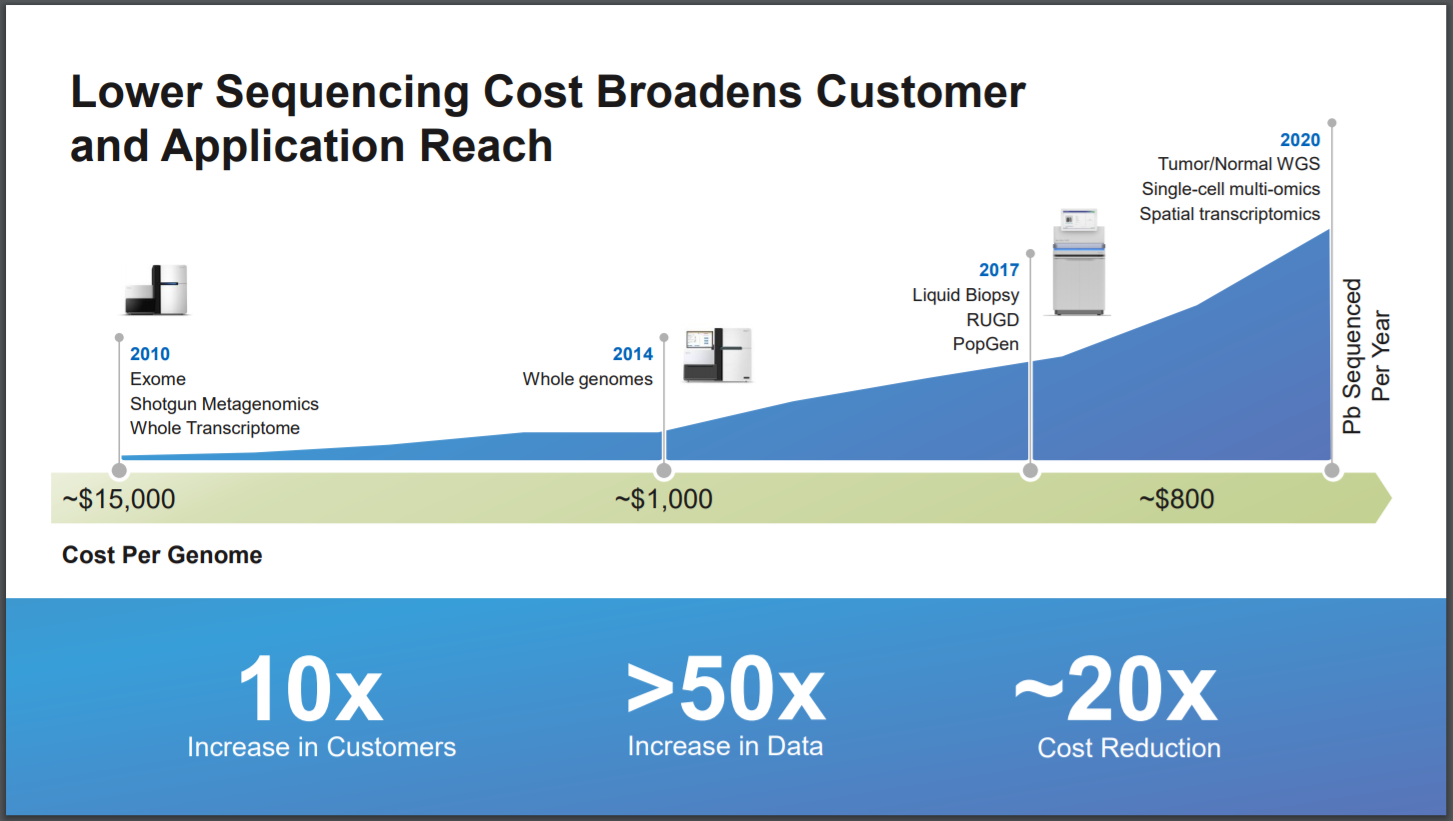

We don’t think the introduction of Illumina’s first sequencing system in 2007, and the drastic decline in sequencing costs that followed, was a mere coincidence. Illumina has been a major driving force in pushing sequencing costs lower. Since 2007, Illumina has reduced the cost of sequencing by more than a factor of 10,000, and the time needed for sequencing by a factor of around 12,000. For perspective, Illumina has brought the cost of sequencing one genome down from US$15,000 in 2010 to less than US$1,000 today – this is illustrated in the following chart:

Source: Illumina 2020 January investor presentation

Far from hurting Illumina’s business, the massive decline in sequencing costs that the company has driven has helped its customer base to grow by more than 10 times over the past decade. And more importantly, revenue growth has followed: Illumina’s top-line surged from US$902.7 million in FY2010 to US$3.5 billion in FY2019. As the costs of DNA sequencing continues its relentless march downward, we believe that more and more use cases will open up, creating new end-markets and applications for Illumina’s products.

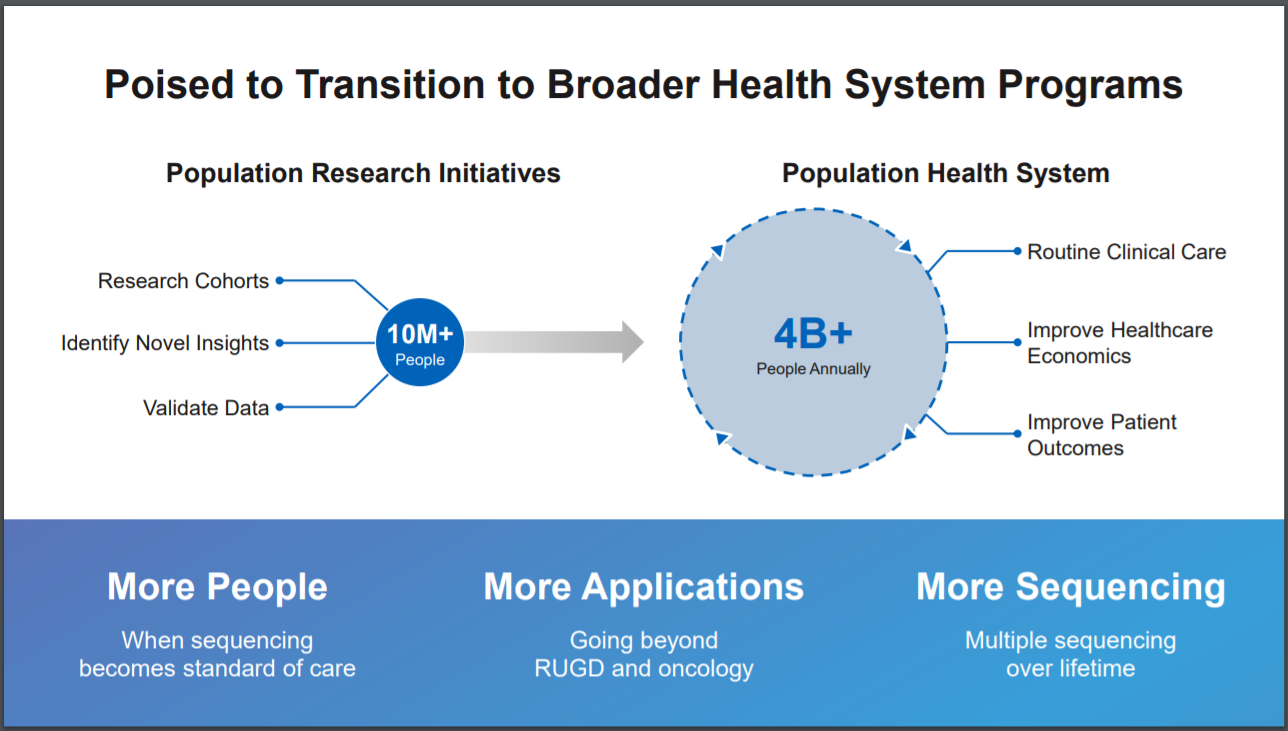

A few examples of exciting new areas for Illumina are the related fields of population genomics, genetic diseases, and oncology (the study and treatment of cancer). Illumina estimates that today, only 10 million-plus people are in research cohorts for population-wide genomic studies. But greater adoption of DNA sequencing in healthcare systems around the world (involving up to four billion people annually) could be happening in the near future, driven by findings from the research on population genomics. DNA sequencing could become part of routine clinical care and help improve healthcare economics and patient outcomes.

Source: Illumina 2020 January investor presentation

On genetic diseases, DNA sequencing is still rarely used (in less than 1% of cases) and a diagnosis typically takes upwards of five years. Inefficiencies in the management of genetic diseases imposes a US$57 billion cost on society. It makes sense to us that the use of DNA sequencing in managing genetic diseases would become increasingly widespread over time.

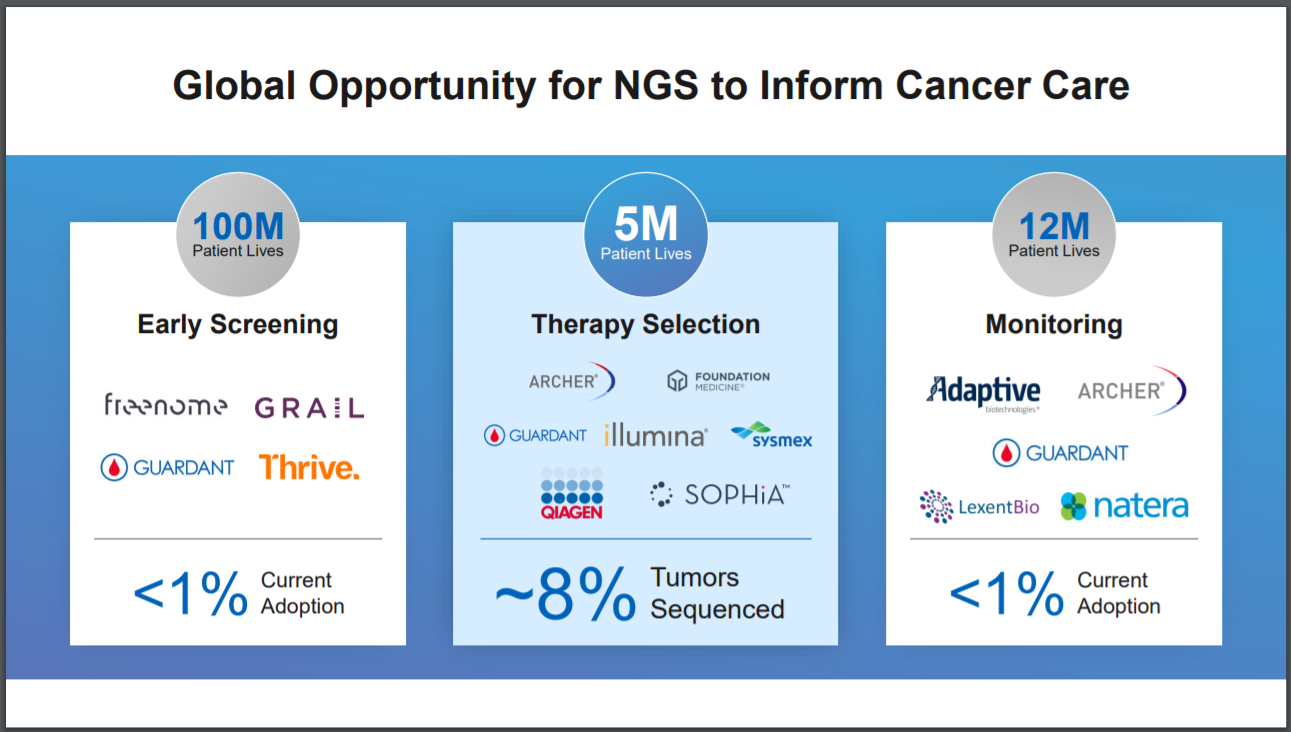

Moving to oncology, global spending on cancer drugs was a staggering US$150 billion in 2018 and projected to increase to nearly US$240 billion by 2023, according to IQVIA, a provider of data analytics services to the life sciences industry. DNA sequencing could have a big role to play in humanity’s war on cancer, given that the technology can be used for early screening, therapy selection, and disease-monitoring. To-date, the penetration rates for DNA sequencing in these three use-cases in oncology are still really low (all less than 8%), as shown in the chart below.

Source: Illumina 2020 January investor presentation (NGS stands for next generation sequencing)

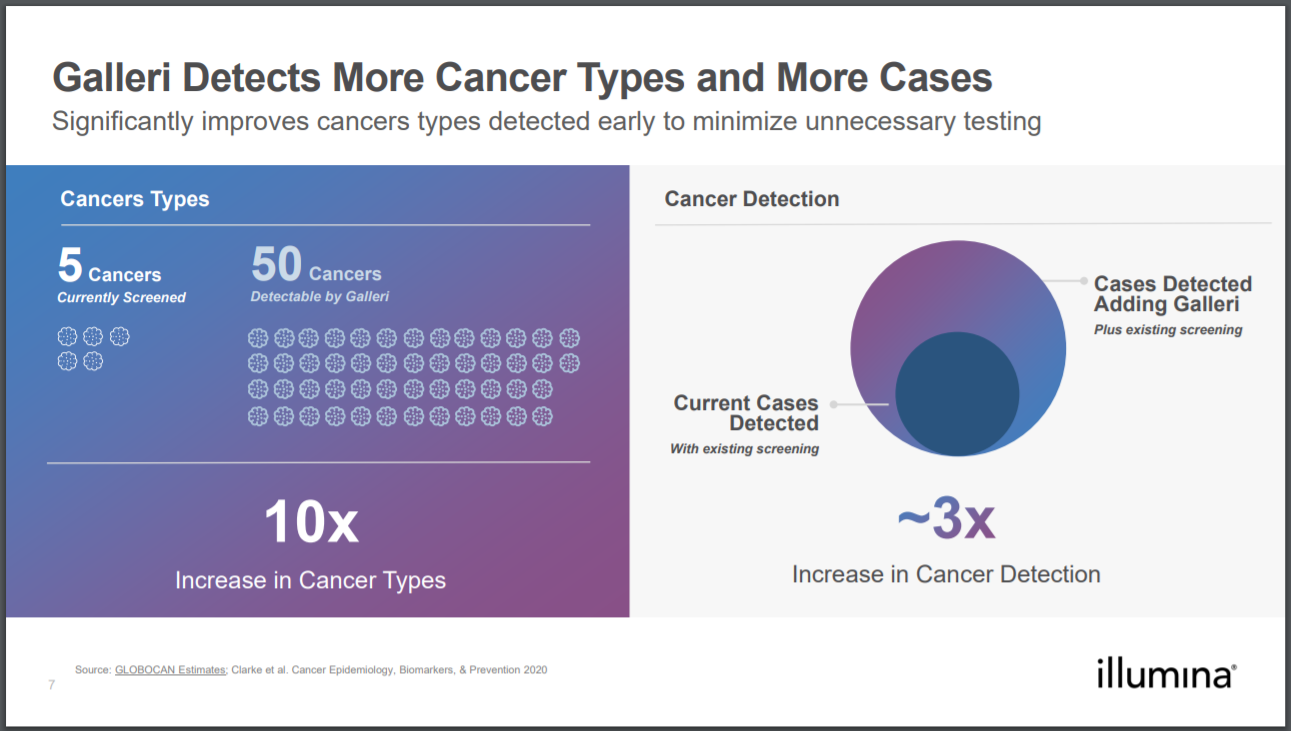

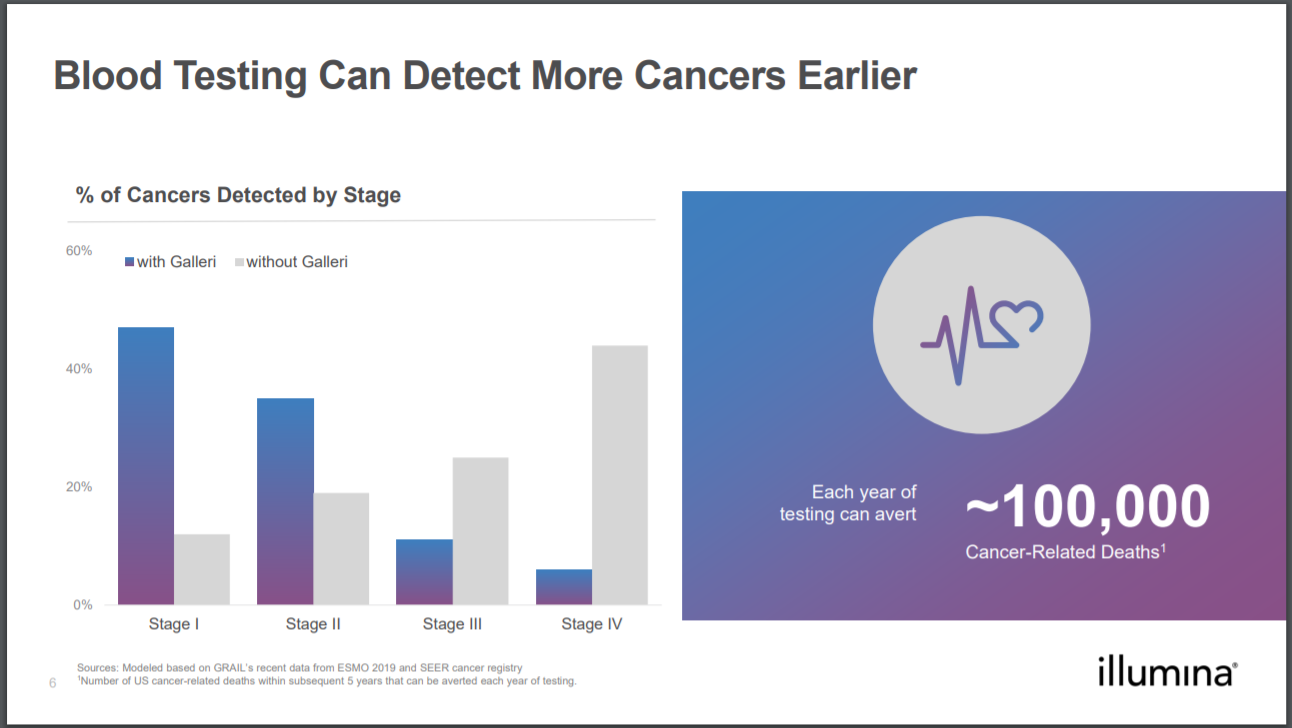

Sticking with oncology, Illumina announced in September 2020 that it would be acquiring GRAIL for US$8 billion (US$3.5 billion in cash and US$4.5 billion in Illumina shares). GRAIL, which participates in the liquid biopsy market (the company develops blood tests for early-cancer detection using DNA sequencing technology), was once under Illumina’s umbrella when it was established in 2016 but was spun off in early 2017. The opportunity could be huge as there is massive value in early cancer detection. The mortality rate for late detection is 79% compared to the mortality rate of just 11% for early detection. But at least half of cancer cases in the USA are currently detected only when they are in Stage III or IV. GRAIL’s first product, called Galleri, is expected to be launched some time this year and trial data show that it improves cancer-detection significantly, as the two slides below illustrate.

Source: Illumina 2020 September presentation on GRAIL

2. A strong balance sheet with minimal or a reasonable amount of debt

The gene sequencing giant has a robust balance sheet,with US$3.32 billion in cash and short-term investments, and just US$1.17 billion in debt, as of 27 September 2020.

Moreover, Illumina also has a long track record of generating free cash flow and is likely to continue doing so in the years ahead (more on these later). For perspective, Illumina’s average free cash flow in FY2019, FY2018, and FY2017 was US$750 million. Even in the first nine months of FY2020, a period of time when the company’s business faced pressure because of COVID-19, there was still free cash flow of US$547 million.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Illumina is led by Francis deSouza, who’s only 49 this year. deSouza joined Illumina as president in 2013 and was promoted to CEO in mid-2016 as a successor to Jay Flatley. From 1999 to 2016, Flatley was Illumina’s CEO and helped grow the company’s revenue from US$1.3 million in 2000 to US$2.2 billion in 2015. After stepping down as CEO, Flatley transitioned to the execution chairman role and was in the seat till 2019, when he then became chairman of Illumina’s board. We appreciate the multi-year tenures that both deSouza and Flatley have with Illumina, and also the fact that deSouza can still tap on Flatley for advice if needed.

In FY2019, deSouza’s total compensation was just US$1.52 million, but this was because there was no equity compensation that was given. The company had decided to move its annual equity grants to the first quarter of 2020. These equity grants consist of two components: Restricted stock units (RSUs) that vest over four years; and performance stock units (PSUs) that vest over three years, with the amount dependent on Illumina’s earnings per share. The equity grants look well-structured to us because they tether the compensation of Illumina’s management team to the long-term business performance of the company (the multi-year vesting of the RSUs mean that it is linked to Illumina’s long-term share price movement, which is in turn driven by the company’s business performance), thus aligning their interests with those of the company’s other shareholders.

Importantly, the sheer majority of deSouza’s compensation in the future is likely to come from these equity grants too. In FY2018, deSouza’s total compensation was a reasonable US$11.07 million, of which 76.8% came from equity grants with the exact same structure as described above. We also want to positively highlight that the lion’s share of the total compensation for Illumina’s other key leaders in FY2018 also came from the same type of equity grants.

Speaking of alignment of interests, deSouza also owns 69,294 Illumina shares as of 30 March 2020, a stake that’s worth US$26.1 million at Illumina’s 7 January 2021 share price of US$377. Flatley controlled 257,970 shares, which have a market value of over US$97 million.

On capability and ability to innovate

We rate Illumina’s management team highly when it comes to execution and innovation. There are a few things we want to discuss.

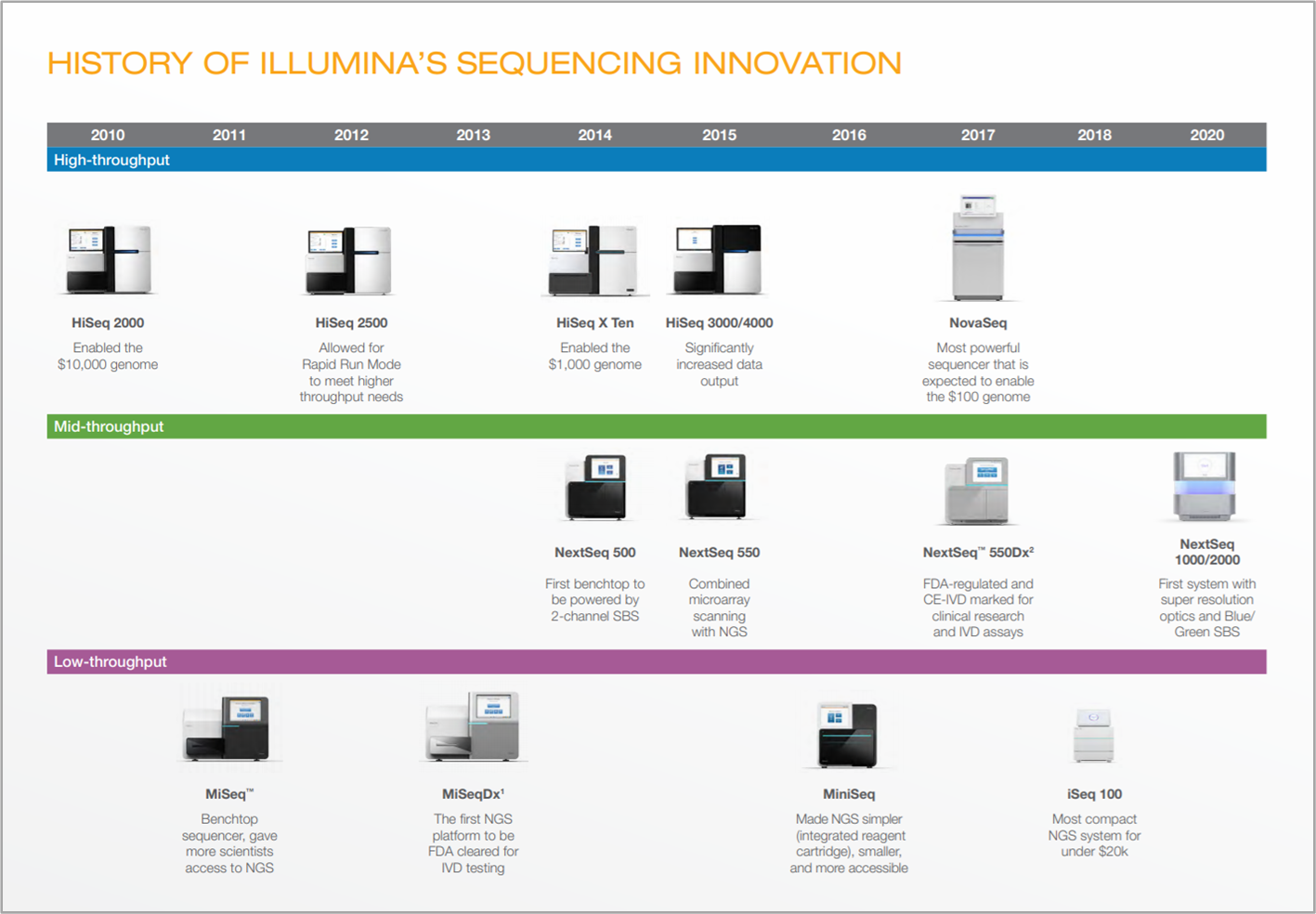

The first is something we mentioned earlier: The incredible decline in DNA sequencing costs that Illumina has produced since 2007. This came about because of consistent product innovation on the part of Illumina, which is the second thing we want to highlight. As the chart below shows, Illumina has been introducing new DNA sequencing systems frequently over the past decade, with improvements made in both costs and throughput (the amount of sequencing that can be done per unit of time). The intensity of product innovation does not seem to have diminished in any way too since Francis deSouza became CEO in mid-2016. In particular, Illumina launched one of its newer-generation sequencing systems, the NovaSeq, in early 2017. The NovaSeq promises to usher in the era of the $100 genome, which if possible, could really open up new cases for DNA analysis at a much greater scale than before.

Source: Illumina 2020 April report

Source: Illumina 2020 April report

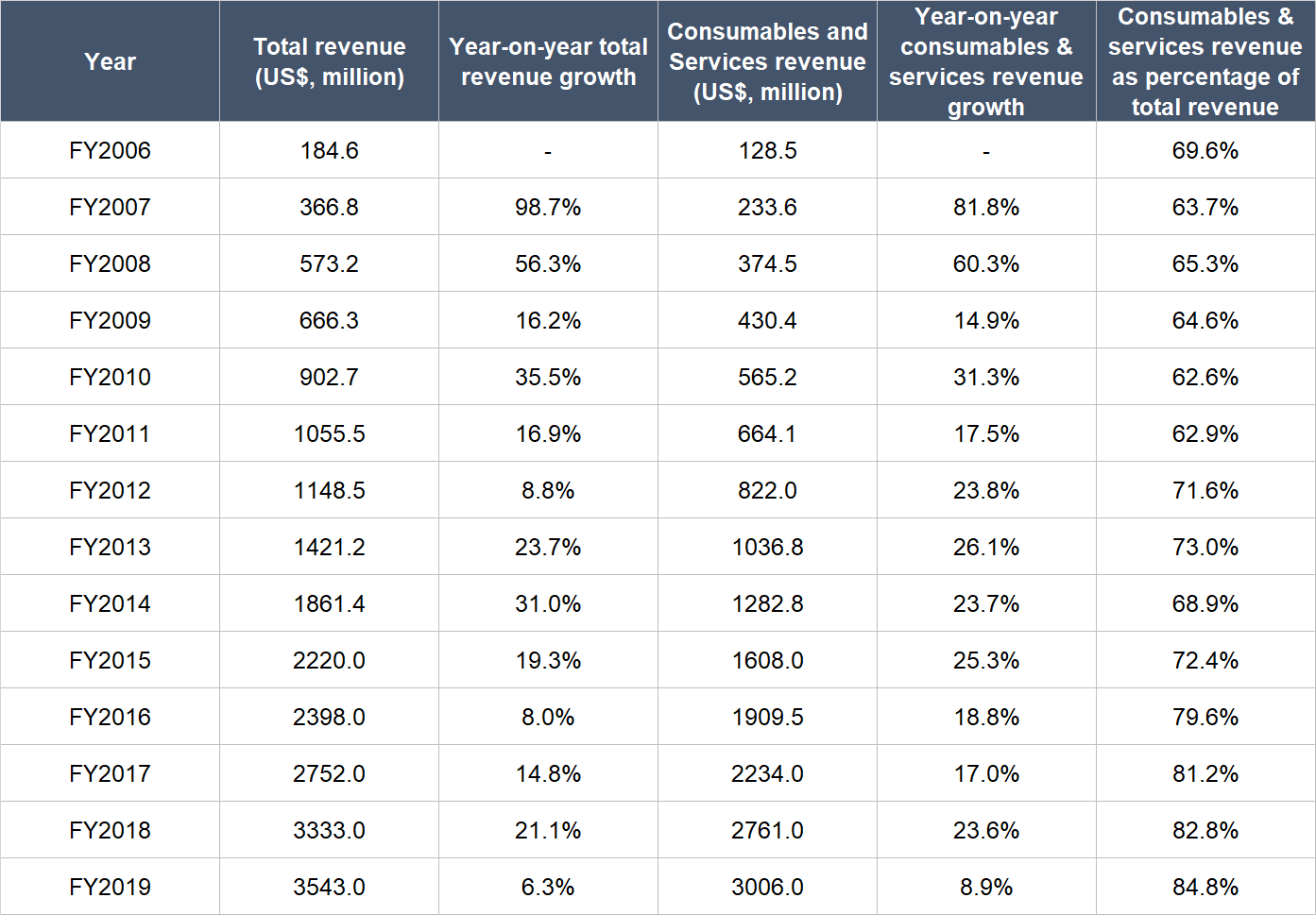

Thirdly, Illumina has grown its consumables and services revenue at a faster clip than its overall revenue over the years, as shown in the table below. To us, this is a sign of management’s ability to improve the adoption and demand for Illumina’s products over time.

Source: Illumina annual reports

Fourth, we’ve been impressed with management’s insistence on investing for innovation despite business headwinds for Illumina during the current COVID-19 pandemic. In Illumina’s earnings conference call for the second quarter of FY2020, Chief Financial Officer Sam Samad said:

“While we expect operating expenses to grow sequentially in the third quarter, we remain thoughtful and deliberate about where we invest. This means continuing to invest in R&D projects and utilizing our balance sheet to pursue growth opportunities. As a genomic technology leader, we believe we have an obligation to invest in innovation regardless of short-term revenue headwinds. But at the same time, we’ll balance this in other areas by pausing or delaying certain capital expenditures and limiting other discretionary spend.”

The fifth thing we want to highlight is Illumina’s clever move of establishing Illumina Ventures together with Nick Naclerio, who was previously a member of Illumina’s senior leadership team. Illumina Ventures, which was set up in April 2016 during Jay Flatley’s run as CEO, is a venture capital firm that seeds early-stage startups that are in the fields of precision medicine and genomics. Illumina Ventures’ first fund is US$230 million in size and Illumina committed US$100 million to it.

Lastly, deSouza and his team appear to have built a fantastic corporate culture at Illumina. Reviews from the Great Place To Work website show that 87% of Illumina’s employees say that the company is a great place to work, compared to just 59% for the average company. Meanwhile, employees have given Illumina a four-star rating on Glassdoor, a website that allows a company’s employees to rate it anonymously. Meanwhile, 74% of Illumina-raters on Glassdoor currently will recommend the company to a friend and deSouza has a 92% approval rating as CEO, far higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Illumina’s DNA sequencing machines are not cheap. We mentioned earlier that they range from the tens of thousands of dollars, to the millions. As you can imagine, due to the large capital outlay Illumina’s machines require, the company’s customers may purchase just a few machines at a time and purchases are based on capital expenditure budgets, which may vary from year to year. This is clearly not recurring revenue.

But Illumina’s machines do bring with them recurring revenues through a classic razor-and-blades business model. In this case, the sequencing machines are the razors while the consumables and services that we brought up in the “Company Description” section of this article are the blades. The sale of sequencing machines only made up 12.5% of Illumina’s total revenue in the first nine months of FY2020, so the majority of the company’s revenue comes from recurring elements in the form of the consumables and services. A similar dynamic also existed in FY2019, FY0218, and FY2017 – consumables and services were on average 83% of Illumina’s total revenues in these three fiscal years. Given the high percentage of Illumina’s revenue that is derived from consumables and services, we believe that a large part of Illumina’s business can be considered as recurring in nature.

This said, the current COVID-19 pandemic has hurt Illumina. For instance, in the second quarter of FY2020, Illumina’s revenue fell 24.5% as the virus had disrupted many of its research customers’ operations. But we see this as just a short-term bump on the road. The long run trends for DNA sequencing technology are firmly in Illumina’s favour, in our opinion. Lending weight to our view are comments that Illumina’s CEO Francis deSouza shared during the company’s earnings conference calls for the second and third quarters of FY2020:

“[Second quarter of FY2020]

While the near-term disruption is challenging as we continue to navigate the pandemic, we remain as bullish as ever on the opportunity ahead for Illumina. The long-term opportunity for sequencing is expanding as the need for more infectious disease research and surveillance capabilities comes into focus. Innovation remains our North Star, and we will continue to partner with our customers as well as innovate internally to ensure that sequencing-based applications are contributing to global efforts to combat this pandemic and whatever combination of research, diagnostics, screening and surveillance applications is the most impactful.[Third quarter of FY2020]

To conclude, the recovery of our business accelerated in the third quarter with significant sequencing consumables revenue growth compared to the second quarter of 2020 and we expect continued consumables growth in the fourth quarter. Importantly, we’re also making good progress incorporating genomics into the standard of care in oncology therapy selection, NIPT [non-invasive prenatal testing] and genetic disease testing. And most importantly, we believe that we’re laying a strong foundation for Illumina’s near- and long-term growth.”

5. A proven ability to grow

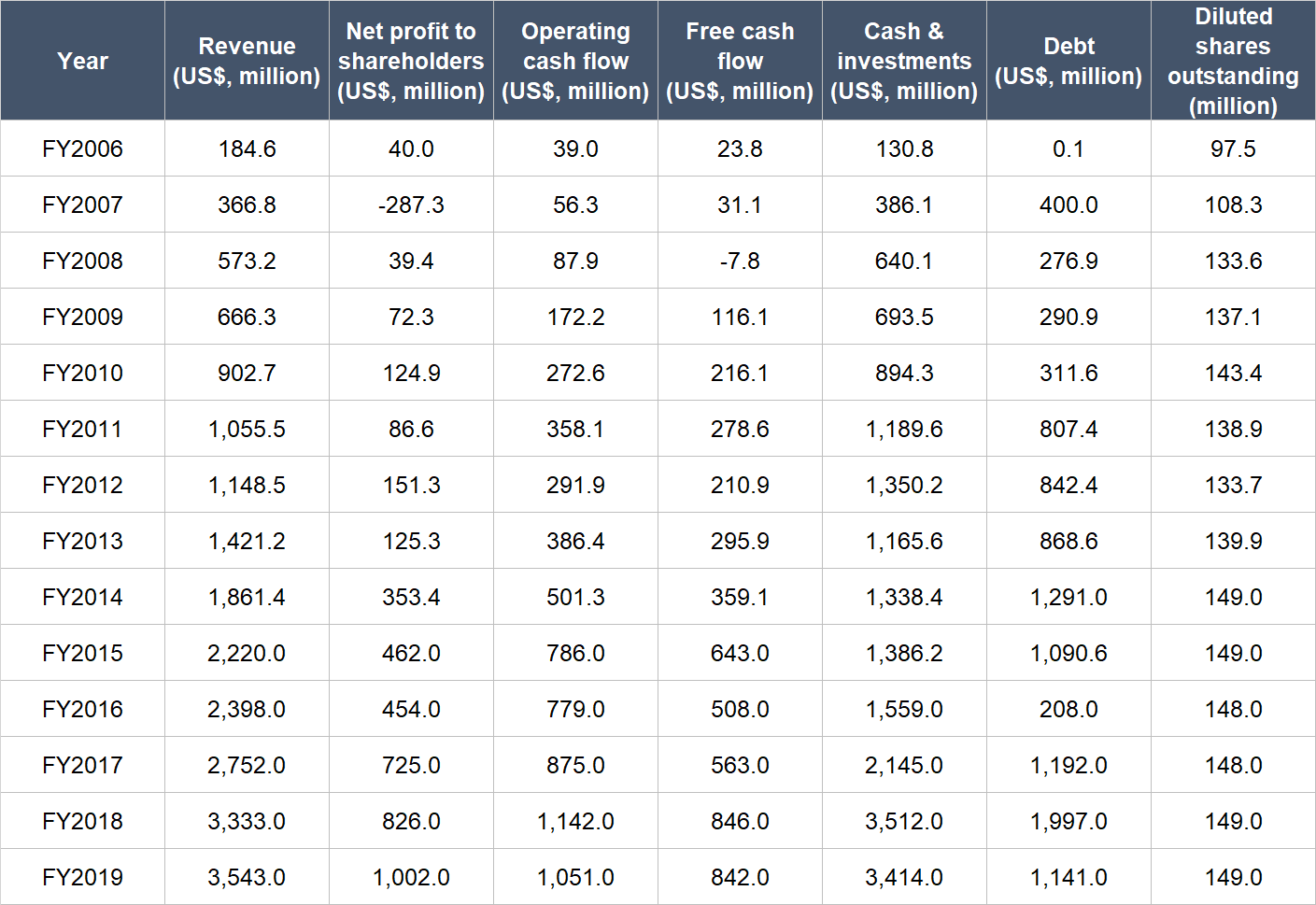

The table below shows Illumina’s important financial data going back to FY2006 (we picked FY2006 as the starting point to observe how the company fared during the 2008-09 Great Financial Crisis):

Source: Illumina annual reports

A few things we noted for Illumina’s financials:

- The company’s revenue growth has been consistent, with growth in every year for the entire time period we’re looking at. From FY2006 to FY2019, Illumina’s revenue compounded at an impressive annual rate of 25.5%; over the past five years from FY2014 to FY2019, the company’s top-line growth was still decent at 13.7% per year.

- Illumina was solidly profitable for the entire period we’re looking at (save for FY2007). The annual growth rates for net profit for the FY2006-FY2019 and FY2014-FY2019 time frames were both strong at 28.1% and 23.2%, respectively.

- Since FY2006, operating cash flow has been consistently positive and growing steadily. From FY2006 to FY2019, Illumina’s operating cash flow increased by an impressive 28.8% per year and the annual growth rate from FY2014 to FY2019 was still robust at 16.0%. Similar dynamics are there for free cash flow too, with FY2007 being the only year where free cash flow was negative. The annual growth rate in free cash flow for the two time periods were also excellent at 31.6% (FY2006-FY2019) and 18.6% (FY2014-FY2019).

- Illumina’s balance sheet was rock-solid for nearly the entire time frame under study. With the exception of FY2007, the amount of debt was lower than the amount of cash and investments in each year.

- Dilution has not been a problem at Illumina. The increase in the number of shares was sharp in FY2008 (up 23.3% from FY2007) but since then, Illumina’s share count has climbed at a glacial pace of just 1% per year. In fact, there has been no effective change in Illumina’s share count since FY2014.

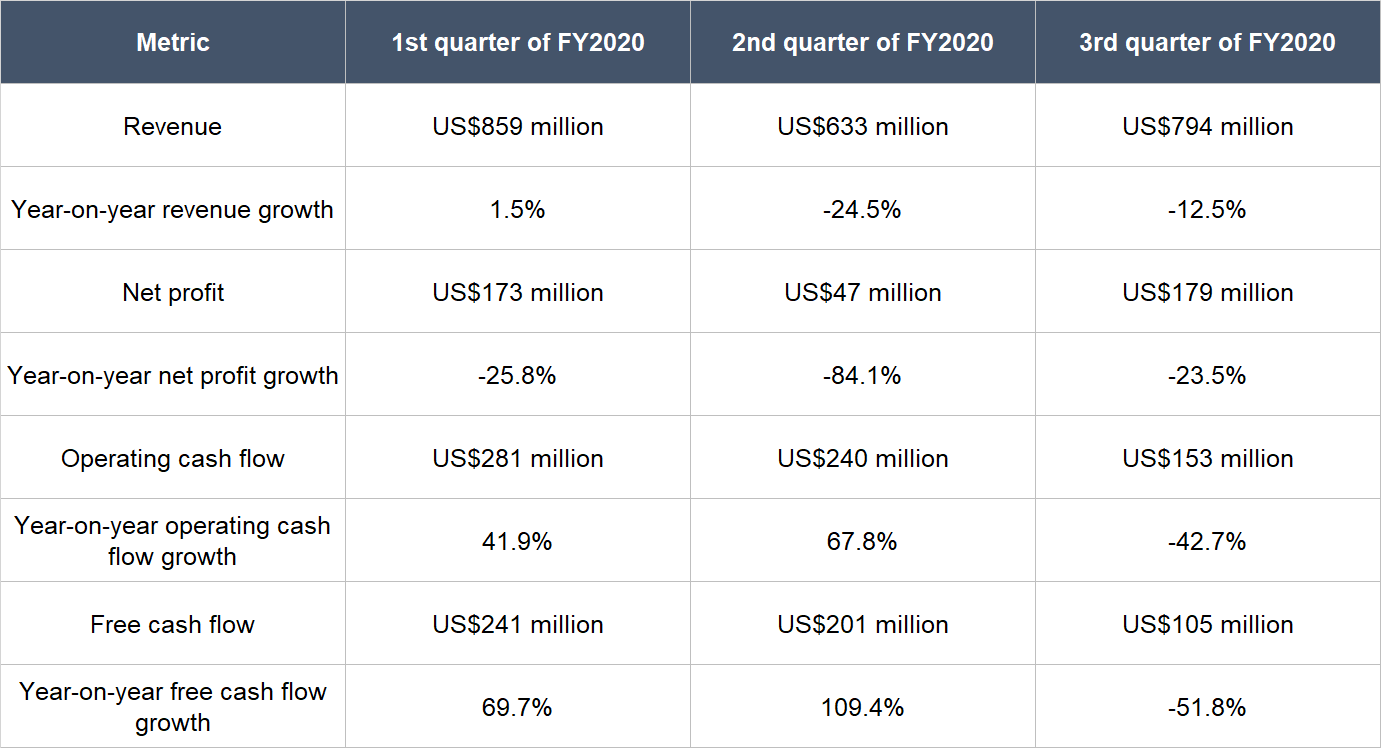

Illumina’s business performance in FY2020 has so far been impacted by COVID-19 as we mentioned earlier. The table below shows the changes in Illumina’s revenue, net profit, operating cash flow and free cash flow in the first three quarters of FY2020. But as we explained earlier, we’re looking at the long run here with Illumina and we think COVID-19 is merely a short-term hiccup for the company.

Source: Illumina quarterly earnings updates

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

We believe Illumina excels here for a few reasons:

- The company’s current revenue is already significantly lower than its market opportunity at the moment, but the market is likely to expand over time – this means that there’s ample room for Illumina’s revenue to grow in the future.

- Illumina has already been generating free cash flow for many years and even managed to do so in the first nine months of FY2020 despite COVID-19-related headwinds to its business. Moreover, Illumina’s free cash flow margin (free cash flow as a percentage of revenue) has averaged at an impressive 23.2% for FY2017-FY2019. In the first nine months of FY2020, Illumina managed a free cash flow margin of 23.9%.

Valuation

We like to keep things simple in the valuation process. In Illumina’s case, we think the price-to-earnings (P/E) and price-to-free cash flow (P/FCF) ratios are appropriate metrics to gauge the value of the company. This is because Illumina has been adept at producing both for many years.

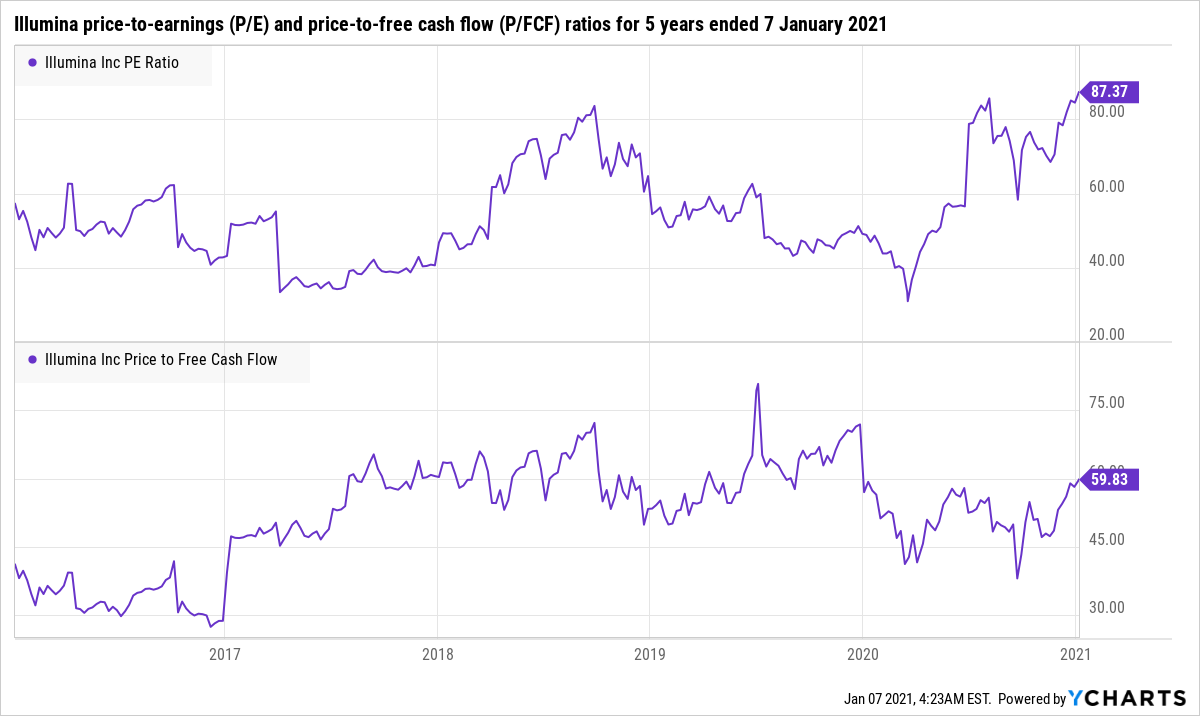

We completed our purchases of Illumina shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$387 per Illumina share. At our average price and on the day we completed our purchases, the company’s shares had trailing P/E and P/FCF ratios of around 61 for both. Here’s a chart showing Illumina’s P/E and P/FCF ratios over the five years ended 7 January 2021:

It turns out that the P/E and P/FCF ratios that Illumina had when we made our investments were not particularly high relative to their histories. This said, they are pretty high in and of themselves. But we’re happy to pay up for a highly innovative company that has a long history of impressive growth and significant runway to expand its business.

For perspective, Illumina carried P/E and P/FCF ratios of 87 and 60, respectively, at the 7 January 2021 share price of US$377.

The risks involved

There are five main risks we see for Illumina.

1. Competition: Illumina currently has a market share of around 70% in the DNA sequencing space, but there’s a risk that it could be leap-frogged technologically by competitors. Illumina’s machines currently excel in short-read sequencing, which is a method that involves the division of a DNA sequence into a few hundred base pairs before reading the sequence. It is more accurate than long-read sequencing, which sequences more than 10,000 base pairs in one single read. But short-read sequencing has its limitations, because crucial information about a strand of DNA could be hard to obtain after the initial sequence is divided for short-reads. There are at least three companies that are working on long-read DNA sequencing technology, namely, Pacific Biosciences, Oxford Nanopore, and Thermo Fisher, and each of them have the potential to develop DNA sequencing machines that are even better than Illumina’s. In late 2018, Illumina entered into an agreement to acquire Pacific Biosciences for US$1.2 billion. But in January 2020, both companies scrapped the deal because of regulatory pressure from the UK Competition and Markets Authority and the US Federal Trade Commission. We are keeping an eye on Illumina’s competitive landscape.

2. An inability to continue lowering sequencing costs: Having low DNA sequencing costs is a key enabler to unlock new use cases for the technology. Illumina will need to be able to continue doing so to grow its market opportunity. If not, new use cases could be difficult to emerge. Illumina was the first company to bring in the era of the $1,000 genome (it did so in 2014), and it was heartening that management talked about the $600 genome during the company’s second-quarter earnings conference call for FY2020. But the rate of the cost-decline appears to be slowing (there was ‘only’ a 40% fall between 2014 and 2020), so we want to watch developments in this area.

3. New use cases fail to become meaningful: Our thesis on the growth in Illumina’s market opportunity is built around the potential for a significant increase in the use cases for DNA sequencing. But these new use cases may not become commercially sustainable markets for Illumina, even if the company manages to bring down the cost for DNA sequencing. There’s an element of a leap-of-faith required with Illumina in this regard. But the chances of new use cases growing into important markets for the company appear high to us.

4. Economic slowdowns: We have already seen the impact that COVID-19 has had on the company’s revenue in FY2020 so far because the operations of research institutions have been affected. If there’s an extended economic slowdown (because of COVID-19 in the current context, or for other reasons in the future), governments and universities may also choose to cut funding on life sciences research – this could hurt Illumina’s business since the company is reliant on researchers spending more on its machines and consumables.

5. A high valuation: We’re comfortable with paying up for Illumina’s shares. But if the company’s growth falters – even if it’s temporary in nature – there could be painful falls in its share price.

Summary and allocation commentary

To summarise, Illumina is a company that:

- Is operating in a large and important market (DNA sequencing) that is also likely to be expanding in the future

- Has a strong balance sheet with significantly more cash & investments than debt

- Has a management team with a strong history of execution and innovation, and a sensible compensation structure with incentives that are well-aligned with those of the company’s shareholders

- Earns most of its revenue from consumables and services, which tend to be recurring in nature

- Has a good long-term track record of growth in revenue, profit, and free cash flow

- Is likely to produce a strong and growing stream of free cash flow in the future

There are risks to note, such as the threat of competition; the chance of meaningful new use cases for DNA analysis failing to appear; the chance that Illumina is unable to continue lowering costs for DNA sequencing; an economic slowdown pressuring research budgets of the company’s customers; and the company’s current high valuation.

But after weighing the pros and cons, we initiated a 2.5% position – a medium-sized allocation – in Illumina with Compounder Fund’s initial capital. While we appreciate the positives found in Illumina’s business, we’re also concerned with the company’s high valuation and the chance that the company could be overtaken in its market by competitors that specialise in long-read DNA sequencing technology.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article besides Illumina, Compounder Fund does not own shares in any of them. Holdings are subject to change at any time.