Compounder Fund: Datadog Investment Thesis - 16 Feb 2021

Data as of 12 February 2021

Datadog Inc (NASDAQ: DDOG), which is based and listed in the USA, is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

With the world transitioning online, companies increasingly require sophisticated cloud software infrastructure to support their digital transformation. But the more sophisticated the infrastructure, the harder it is to monitor and analyse. To make matters worse, companies may house their technology stack in isolated data silos, exacerbating the challenge for companies’ software engineers.

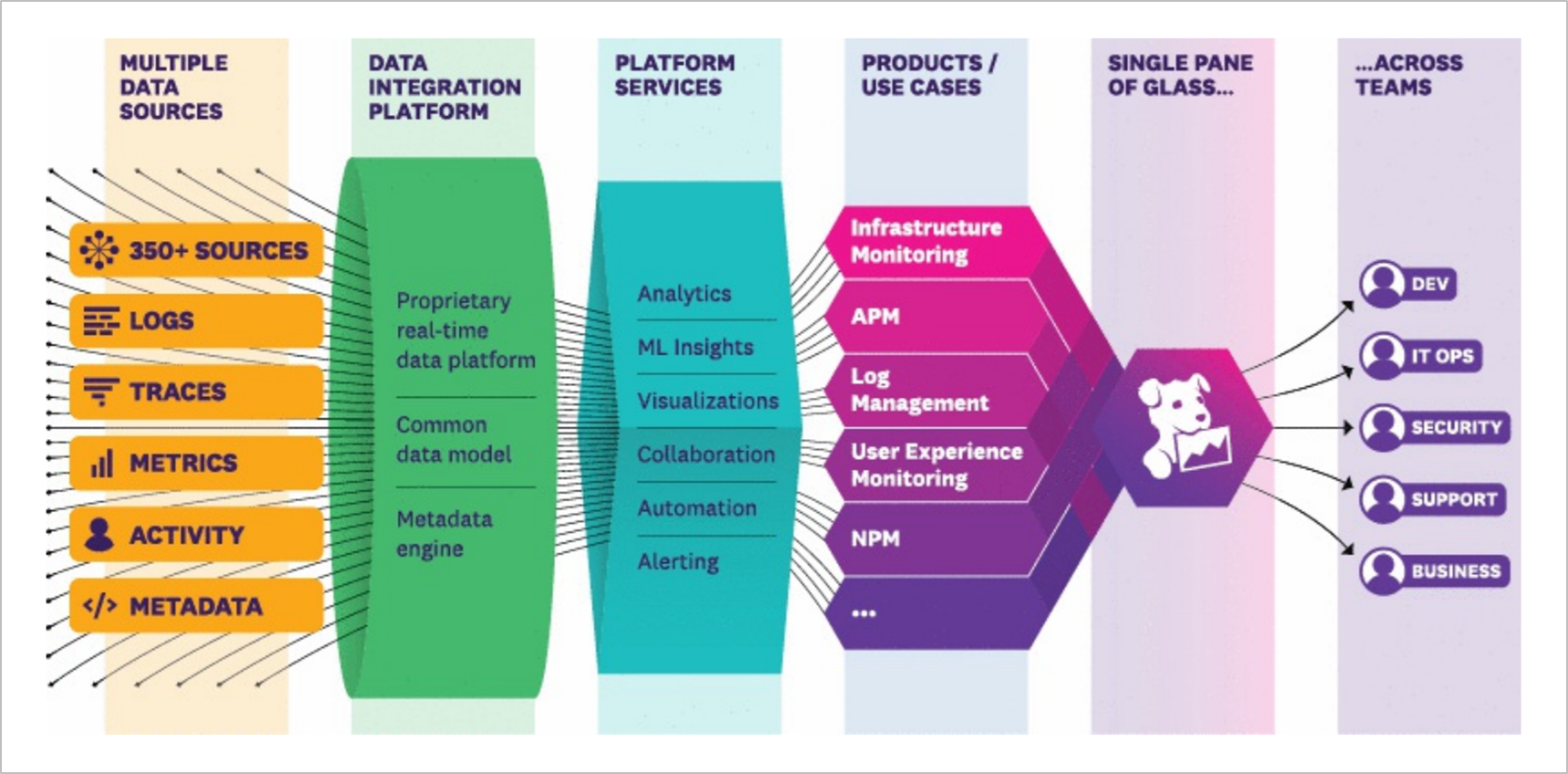

Enter Datadog, which provides a proprietary software platform to monitor and analyse the performance of software applications and IT (information technology) infrastructure that companies are using. In the words of Datadog’s management, the company was founded in 2010 with the goal to “build a real-time data integration platform to turn chaos from disparate sources into digestible and actionable insights.” Datadog’s platform gives users a “single pane of glass” view for key areas in their technology stack that requires observation. The platform is also modular, meaning that users can choose to purchase different combinations of products, depending on their needs.

Source: Datadog IPO prospectus

For a geographical perspective, 75% of Datadog’s total revenue of US$425.9 million in the first nine months of 2020 came from the North America region. The remaining 25% was under the “International” category. (At the time of writing, we do have some of Datadog’s financial numbers for the whole of 2020, but the geographical breakdown is still unavailable. So we used the next best available information, which was the geographical revenue breakdown for the first nine months of 2020.)

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Datadog.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Without the ability to monitor their software applications and IT infrastructure, companies become effectively blind to factors that could affect the performance, reliability, scalability, and availability of their technology systems. So, monitoring software can be thought of as the foundation for a company’s technology stack.

Yet, many companies currently do not employ sufficient monitoring. Datadog said in its 2019 IPO prospectus (the company was listed in September 2019) that only 5% of software applications were monitored as of 2018, according to Gartner. In addition, there are throngs of companies that are shifting to cloud-based IT infrastructure from legacy on-premise ones. With the migration to the cloud, the need for a specialised tool for monitoring increases.

Given all these positive trends, Datadog believes that it is addressing a huge market opportunity. We agree. In its IPO prospectus, Datadog estimated its addressable market to be US$35 billion. Datadog came to the estimate based on (1) the total number of global companies with a headcount of 200-999, (2) the total number of global companies with a headcount of at least 1,000, and (3) its average annual recurring revenue back then for both cohort of customers for each of its platform’s products. The IPO prospectus also provided a reality check on Datadog’s estimates: Datadog’s platform addresses a significant portion of the IT Operations Management market, which research outfit Gartner estimates will be US$37 billion in 2023. With revenue of merely US$603.5 million in 2020, Datadog has plenty of room to run, in our opinion.

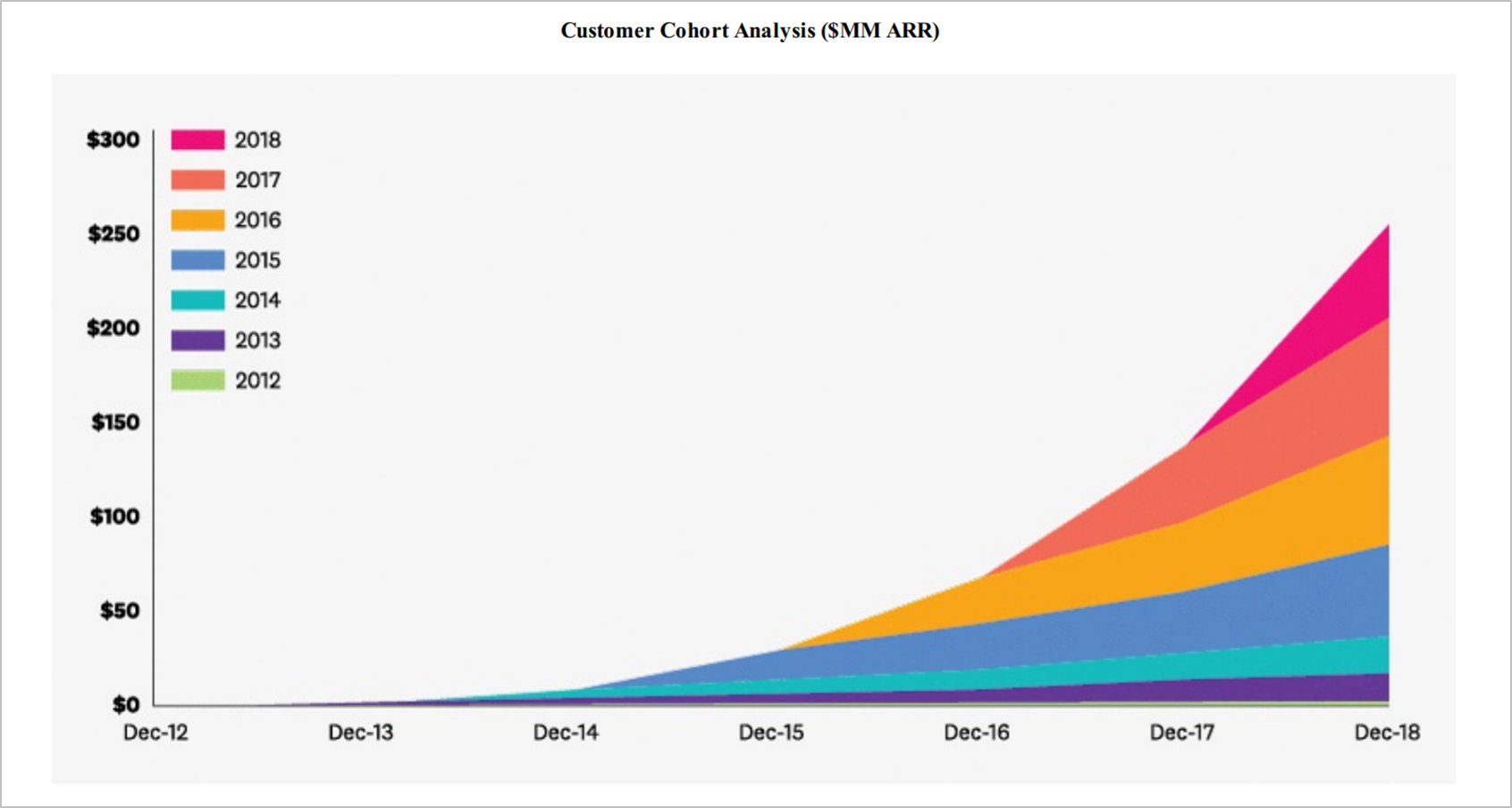

But what’s really exciting to us about Datadog’s market opportunity is this: The annual recurring revenue (ARR) generated by Datadog’s customers have historically increased over time. The chart below shows the growth in total ARR for each of Datadog’s customer-cohorts from 2012 to 2018. Each coloured band represents a yearly customer cohort and it’s clear that each band has thickened over time, indicating an increase in the total ARR generated by each cohort as the years progress. In our opinion, what this signifies for Datadog is that its market opportunity is likely to expand over time.

Source: Datadog IPO prospectus

2. A strong balance sheet with minimal or a reasonable amount of debt

Datadog went public in September 2019, raising US$705.9 million, net of all fees. This helped improve what was already a robust balance sheet – at 30 June 2019, the latest data available prior to Datadog’s IPO, the company held zero debt and US$52.3 million in cash and investments.

Datadog’s latest financials are as of 31 December 2020 and the company’s balance sheet has strengthened since the IPO when it had net cash of around US$760 million. The company exited 2020 with US$1.52 billion in cash and investments and just US$575.9 million in debt (all are convertible notes), which give rise to a net cash position of US$941.6 million. For the sake of conservatism, we note that Datadog does have operating lease liabilities of US$67.8 million. But the sum of the operating lease liabilities and debt is still far outweighed by the cash and investments that Datadog has on hand.

3. A management team with integrity, capability, and an innovative mindset

On integrity

Datadog is led by its co-founders Olivier Pomel and Alexis Lê-Quôc. Pomel, 44, is Datadog’s CEO while Lê-Quôc, 46, serves as Chief Technology Officer. Both men have been in their roles since the company’s founding in 2010. We appreciate the fact that Datadog’s co-founders are both young but yet already have more than a decade of experience each leading the company.

In 2019, both Pomel and Lê-Quôc received handsome total compensation of US$18.58 million and US$11.33 million, respectively. These are large sums when compared to the scale of Datadog’s business, which is something we do not appreciate. For perspective, the company’s revenue in the same year was US$362.8 million. The saving grace is that the lion’s share of their total compensation (97.6% for Pomel and 96.0% for Lê-Quôc) came from stock option awards which vest over a three-year period that started from September 2020. In our opinion, the multi-year vesting period helps align the interests of Pomel and Lê-Quôc with those of Datadog’s other shareholders. This is because a multi-year vesting period means that the value of the stock option awards are linked to multi-year changes in Datadog’s share price, which is in turn connected to the company’s business performance.

And speaking of alignment of interests, Pomel and Lê-Quôc controlled a total of 26.27 million Datadog Class A and Class B shares based on their latest regulatory filings (see table below). There are differences between the Class A and Class B shares in terms of their voting power and listing status (the Class A shares are publicly traded and hold just 1 vote per share while the Class B shares are not publicly traded and hold 10 voting rights per share), but they are economically identical. At Datadog’s share price of US$118 on 12 February 2021, Pomel and Lê-Quôc’s total Datadog shares are worth US$3.09 billion, which we think represents significant skin in the game for both men.

Source: Oliver Pomel and Alexis Lê-Quôc SEC filings (based on latest filings as of 12 February 2021)

We want to highlight that nearly all of Pomel and Lê-Quôc’s Datadog shares are of the Class B variety. As a result, both men collectively controlled 38.2% of Datadog’s voting power (as of 31 March 2020) despite holding only 21.4% of Datadog’s total shares (also as of 31 March 2020). Managers having significant control over a company can potentially be bad for shareholders. This concentration of Datadog’s voting power in the hands of Pomel and Lê-Quôc means that we need to be comfortable with them at the company’s helm. We are.

On capability and ability to innovate

We rate Oliver Pomel and Alexis Lê-Quôc highly in this area. There are a few things we want to discuss.

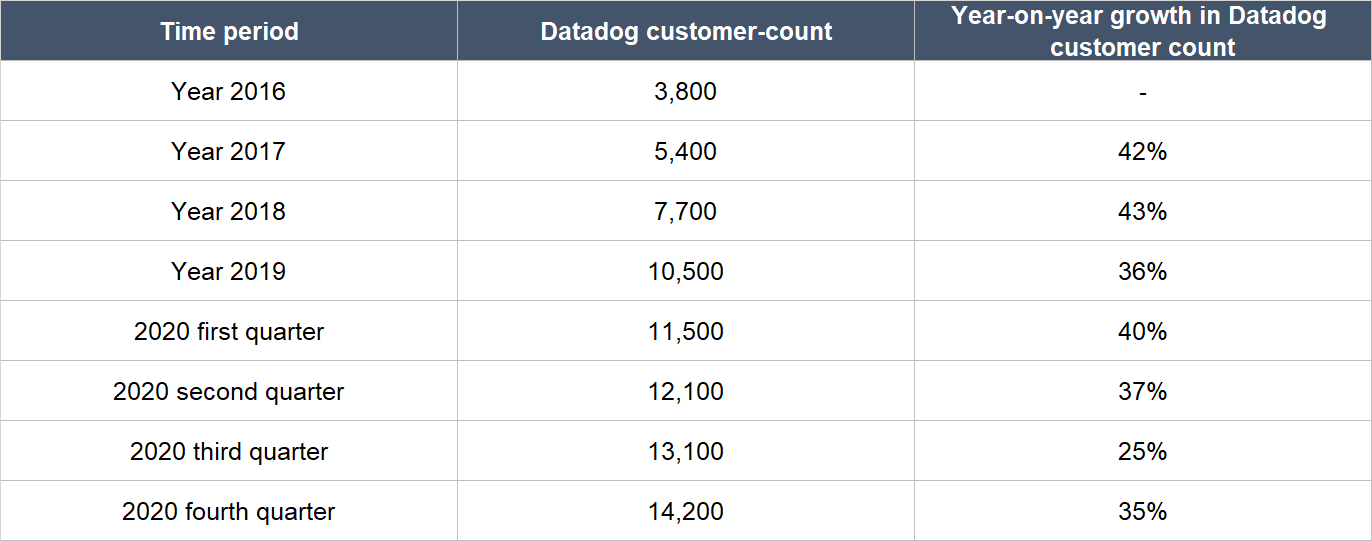

First, Datadog has executed brilliantly with its land-and-expand strategy. The strategy starts with the company initially landing a customer with a product on its platform, and then expanding its relationship with the customer through heavier usage of the product and/or more products. The success can be illustrated through (1) Datadog’s impressive growth in its customer-count, and (2) the strong dollar-based net retention rate enjoyed by the company. The dollar-based net retention rate (DBNRR) is a very important gauge of the health of Datadog’s business. It effectively measures the change in revenue from the entire cohort of Datadog’s customers from a year ago compared to today; the DBNRR includes positive effects from upsells as well as negative effects from customers who leave or downgrade. Anything more than 100% indicates that Datadog’s customers, as a group, are spending more. Impressively, Datadog’s DBNRR has exceeded 130% for 14 consecutive quarters (that’s more than three years!) as of the fourth quarter of 2020. The table below shows the growth in Datadog’s customer count since 2016:

Source: Datadog annual reports and quarterly earnings conference calls

Second, Datadog’s platform has a self-service installation process and users can deploy it quickly (often within minutes) and easily, wth no need for any specialised training, heavy implementation, or customisation. We credit Pomel, Lê-Quôc, and their team for building these traits into Datadog’s platform – we believe that the low friction involved with the use of the company’s products has been one of the key factors for Datadog’s strong DBNRRs and growth in customer-count that we mentioned earlier.

Third, Pomel and Lê-Quôc have an impressive history of using capital efficiently at Datadog. From its founding in 2010 to its listing in 2019, Datadog had raised only US$92.0 million in capital; we also shared earlier that the company had zero debt and held US$52.3 million in cash and investments just prior to its listing.

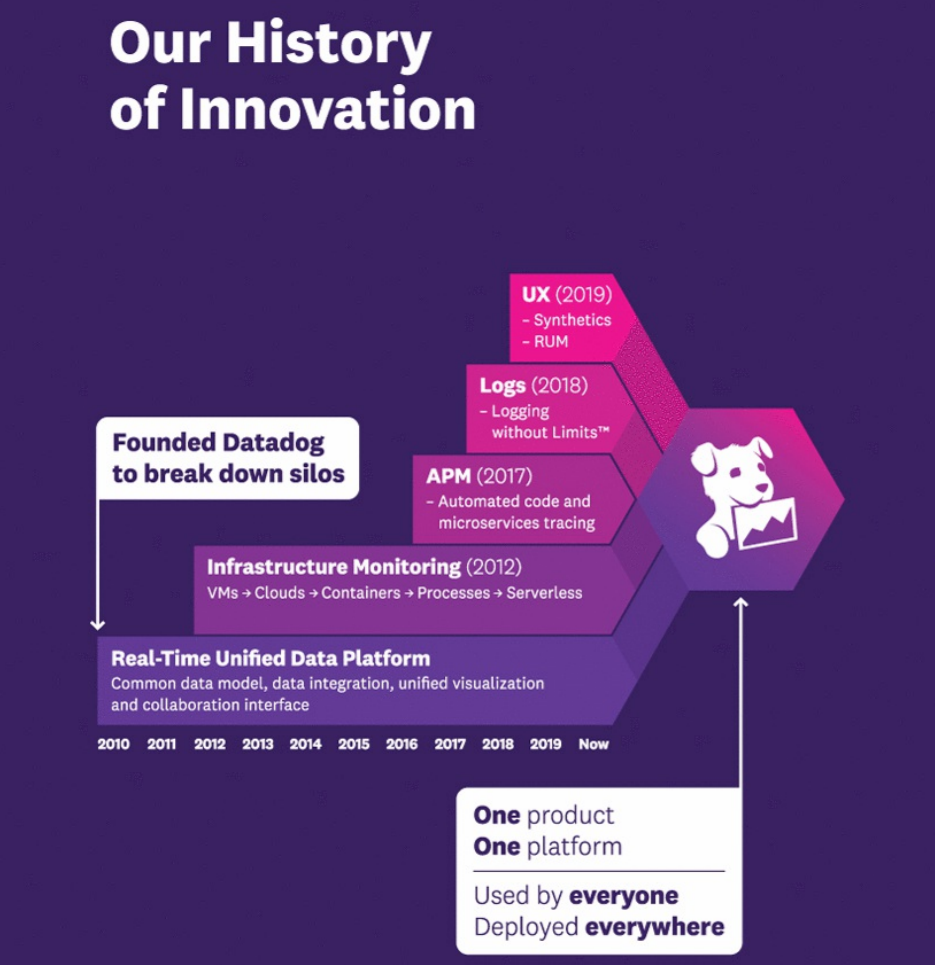

Fourth, Datadog has a history of constant innovation. The diagram below gives a good overview of the new features that Datadog has added to its platform over time from 2010 to 2019. In particular, Datadog combined the “three pillars of observability” for monitoring a company’s technology stack – logs, metrics, and traces – with the introduction of its log management solution in 2018. This is noteworthy because no company before Datadog could bring together these three observability pillars into a single pane view. As you can imagine, it can be a challenge to identify any errors in a company’s technology stack by having to go through each observability-pillar on different platforms.

Source: Datadog IPO prospectus

Some of Datadog’s more recent product innovations in 2020 include:

- Datadog Marketplace, which allows Datadog’s partners to build applications on top of its platform

- General availability of Continuous Profiler, which measures code performance

- The beta launch of Compliance Monitoring, which proactively notifies users on misconfigurations and compliance-drift

Fifth, Datadog’s co-founders appear to have built a solid corporate culture at the company. Glassdoor is a platform for employees to rate their companies anonymously. Datadog is currently rated 4.2 stars on Glassdoor (out of 5). Meanwhile, 83% of Datadog-raters on Glassdoor will recommend the company to a friend, and Pomel has an excellent 95% approval rating as CEO, which is far higher than the average Glassdoor CEO rating of 69% in 2019.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Datadog is a software-as-a-service (SaaS) company that sells subscriptions – with mostly monthly and annual terms – to its IT-monitoring software platform. Virtually all of the company’s revenue, since its founding, have come from subscriptions.

Even though subscriptions are recurring in nature, just having a subscription-based business alone does not mean that a company actually has recurring revenues. If the business has a high churn rate (the rate of customers leaving), the company is constantly filling a leaky bucket. That’s not recurring revenue.

There are four reasons why we think Datadog does not have to deal with a leaky bucket. First, we mentioned earlier that Datadog’s yearly customer cohorts tend to increase their total ARR (annual recurring revenue) with the company over time. Second, when we discussed Datadog’s management, we shared the company’s mightily impressive record of producing a dollar-based net retention rate of more than 130% for 14 straight quarters. Third, we think that the monitoring of an organisation’s technology stack is likely to be mission-critical; this means that Datadog’s platform is a highly important service for its customers, so subscriptions to the platform will tend to be very sticky. Fourth, there’s no customer-concentration at Datadog, with no single customer accounting for more than 10% of total revenue in each of 2017, 2018, and 2019.

5. A proven ability to grow

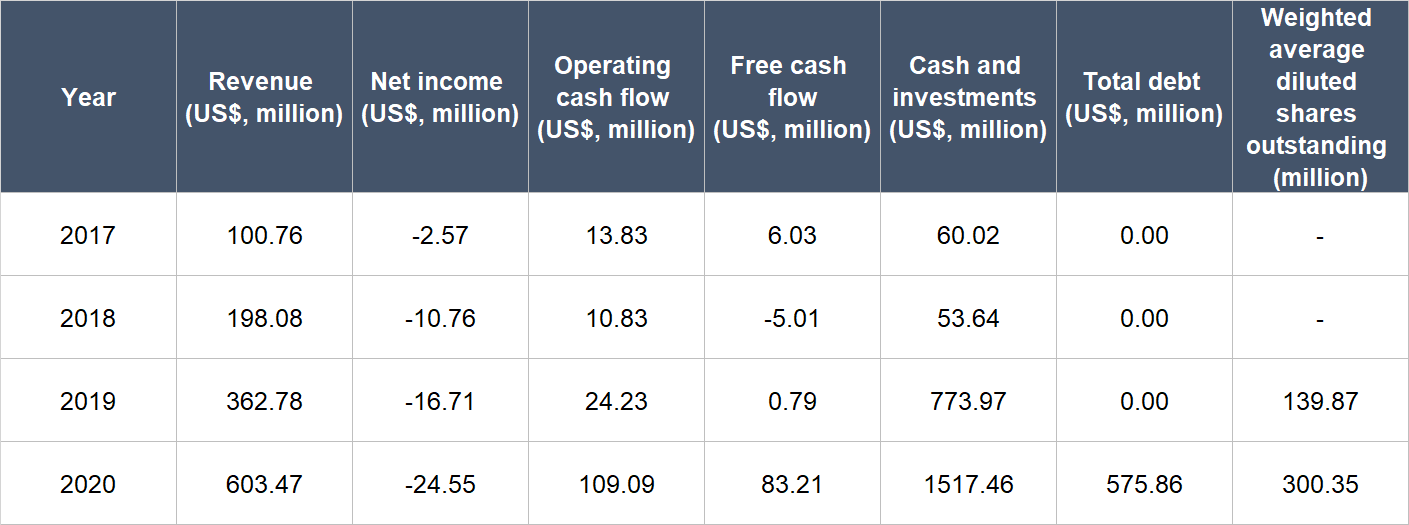

Datadog has a short history as a public-listed company (its IPO was only in September 2019) so we don’t have much financial data to study for the company. But we like what we see. The table below shows Datadog’s important financial numbers from 2017 to 2020:

Source: Datadog annual report and IPO prospectus

A few key things to highlight from Datadog’s financials:

- Datadog’s revenue has compounded at an incredible annual rate of 81.6% from 2017 to 2020. The growth rate in 2020 was a little slower at 66.3%, but is still excellent.

- The loss increased for 2017-2020 but we’re not concerned.

- Datadog generated positive operating cash flow in each year for the time frame we’re studying and the financial metric increased markedly in 2020. Free cash flow (net of capitalised software development costs) was either positive or only slightly negative for 2017-2020 and came in strong in 2020. In particular, Datadog’s free cash flow margin (free cash flow as a percentage of revenue) for 2020 was a respectable 13.8%.

- Even before Datadog’s IPO in the third quarter of 2019, the company’s balance sheet was already strong with millions in cash and investments and zero debt.

- We only started looking at Datadog’s share count in 2019 since it was listed in the third quarter of the year. At first glance, Datadog’s share count appears to have increased tremendously from 2019 to 2020 (a 115% jump). But the number we’re using is the weighted average diluted share count. Right after Datadog got listed in September 2019, it had a share count of around 290 million. This means that the increase in 2020 was much milder (in the low-single digit percentage range) and at an acceptable level given the robust growth in Datadog’s business. We will be keeping an eye on Datadog’s dilution.

The biggest economic story in 2020 is COVID-19, which was officially designated as a pandemic by the World Health Organisation in March of the year. The pandemic had some slight negative impacts to Datadog’s business, particularly in the second quarter of 2020, as the company has customers in industries such as hospitality and travel that are heavily affected. But by and large, Datadog has managed to shrug off COVID-19 to continue posting pleasing growth numbers in 2020.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Datadog has not consistently generated positive free cash flow in the past, but we think it has the ability to do so in the future.

We believe that Datadog has strong unit-economics. This can be seen from the company’s high dollar-based net retention rate that we mentioned earlier, and it should aid the company in producing strong free cash flow eventually. We’ve already caught a glimpse of Datadog’s free cash flow prowess with its respectable free cash flow margin of 13.8% in 2020. SaaS companies, when in a more mature growth phase, tend to carry free cash flow margins of 25% or more. We see no reason why Datadog can’t achieve this in the years ahead, especially since its gross margin has been consistently above 75% from 2017 to 2020.

Valuation

We completed our purchases of Datadog shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$90 per Datadog share. At our average price and on the day we completed our purchases, Datadog shares had a trailing price-to-sales (P/S) ratio of around 69. We like to keep things simple in the valuation process. In Datadog’s case, we think the P/S ratio is currently an appropriate metric to gauge the value of the company, since the company does not have a long history yet of generating free cash flow.

There’s no need to consult any historical valuation chart to know that the P/S ratio of 69 is high – and that’s a risk. For perspective, if we assume that Datadog has a 25% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 276 (69 divided by 25%). But we think Datadog is an excellent company that has years of rapid growth ahead of it. This makes us comfortable with paying up for Datadog’s shares, since we think the company has a good chance of being able to grow into its valuation.

For perspective, Datadog carried a P/S ratio of around 58 at its 12 February 2021 share price of US$118. Interestingly, this P/S ratio is lower despite the share price being higher than our average purchase price.

The risks involved

There are a few risks that we see with our Datadog investment:

1. Key-men risk: We think that Oliver Pomel and Alexis Lê-Quôc have been instrumental in Datadog’s success thus far. Both of them appear to be technical leaders who were and are able to see how they could add value to companies that are transitioning their technology infrastructure to the cloud. Under their leadership, Datadog has also been remarkably efficient with its use of capital – as mentioned earlier, the company had raised only US$92.0 million in capital from its founding to its IPO, a period of around nine years. Should any of them leave, we’ll be keeping an eye on the leadership transition. The good thing is that both Pomel and Lê-Quôc are still young, so they should still have plenty of gas left in the tank to continue leading the company in the years ahead.

2. Competition: Datadog operates in a market that we think is huge and growing. But the company has, well, company. In its 2019 annual report, Datadog name-dropped 12 competitors across its different product categories. Some of these are technology heavyweights with much higher revenues – and thus financial firepower – than Datadog and they include Amazon, Cisco Systems, Google (whose parent is Alphabet), IBM, and Microsoft. Datadog has so far been holding the fort admirably, given its excellent dollar-based net retention rate and growth in customer-count over the past few years. But the situation could change in the future. We will be keeping an eye on Datadog’s competitive landscape.

3. High valuation: High growth-expectations are baked into Datadog’s share price. We’re comfortable paying up for the company’s shares, but if Datadog’s growth falters – even if it’s temporary in nature – there could be painful falls in its share price.

Summary and allocation commentary

To sum up Datadog, it has:

- A large and growing addressable market

- A robust balance sheet with significantly more cash and investments than debt

- A management team with significant skin in the game and a good track record of innovation and solid execution

- High levels of recurring revenues that come from subscriptions to its platform

- An excellent – albeit short – track record of revenue growth

- A high probability of being able to generate strong free cash flow in the future, given its strong unit economics.

There are risks to note, such as key-men risk; competition from deep-pocketed technology heavyweights; and a high valuation.

After weighing the pros and cons, we decided to initiate a 1% position in Datadog – a small-sized allocation – with Compounder Fund’s initial capital. We’re attracted to the growth prospects offered by Datadog, but when we initially invested in July 2020, the company’s free cash flow was not as strong as today (we only had the financial numbers for the first quarter of 2020 to work with), so our enthusiasm was tempered. Another factor that influenced our allocation sizing with Datadog was the company’s high valuation.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned, Compounder Fund also owns shares in Alphabet, Amazon, and Microsoft. Holdings are subject to change at any time.