Compounder Fund: Shinhan Financial Group Investment Thesis - 22 Jul 2025

Data as of 21 July 2025

Shinhan Financial Group (KSE: 055550)(NYSE: SHG) is a company in Compounder Fund’s portfolio that we invested in for the first time in late-June 2025. This article describes our investment thesis for the company.

Company description

We invested in Shinhan Financial Group (abbreviated as SFG from here on) because we believe it’s currently undergoing a special situation. In Compounder Fund’s website and Owner’s Manual, we described such situations as “stocks where step-changes in regulations or market conditions are likely to benefit their businesses in the future.” We think SFG is in the midst of a regulatory-driven change in its business that makes it a good bargain. Consequently, this investment thesis will not have the same structure as our other theses.

SFG is a financial conglomerate based in the Republic of Korea (South Korea). Its roots can be traced to 1982 with the formation of Shinhan Bank. In 2001, SFG was created. Over the years, the company has made multiple acquisitions of many different types of financial institutions, such as securities firms, investment advisory firms, asset management firms, life insurers, banks, and more. Banking, however, remains a corner-stone for SFG, with assets from banking businesses accounting for 83% of the financial conglomerate’s total assets of ₩746.2 trillion (around US$551.8 billion) as of 31 March 2025. Today, Shinhan Bank is the mainstay of SFG with its 76% share of total assets and it is among the four largest banks in South Korea.

Although SFG has business interests in many parts of the world (including the North American and European continents), South Korea accounts for nearly all of its revenue.

SFG has been listed on the South Korean and US stock markets since September 2001 and September 2003, respectively. The US-listed shares are known as American Depositary Shares (ADS). For convenience, Compounder Fund owns SFG’s ADS instead of the South Korean shares. One SFG ADS is equivalent to one SFG South Korea-listed share and there is currently an immaterial price difference between the two types of shares. As of 21 July 2025, SFG’s South Korea-listed shares had a price of ₩69,000 each, which translates to US$49.90 based on the exchange rate of US$1 to ₩1,383 on the same date; meanwhile, each SFG ADS had a price of US$49.72.

The value we see

On 26 February 2024, South Korea’s government introduced the Corporate Value-Up Program through its financial regulator, the Financial Services Commission. South Korea’s government, including its highest echelons, had become frustrated with the “Korea discount.” The country’s then-President, Yoon Suk Yeol, pledged in January 2024 to solve the problem. Yoon’s successor, Lee Jae Myung, announced in April 2025 before he became President in June, that he too wanted to see the discount eliminated.

What is this “Korea discount” which has South Korea’s leaders up in arms? According to a 2023 report from the Korea Capital Market Institute, titled Analysis of the causes of Korea Discount, the phrase surfaced in the early 2000s and has since stuck. It refers to the phenomenon of stocks in South Korea having low valuations when compared to their global peers. For perspective, the Korea Capital Market Institute’s aforementioned report found that the price-to-book (P/B) ratio of South Korea’s stocks was ranked 41st out of 45 countries.

The South Korea government’s intention with the Corporate Value-Up Program is to improve valuations sustainably among companies listed in the country’s stock market. The program encourages public-listed South Korean companies to raise their valuations through means such as hiking dividends, repurchasing shares, and improving business operations. The initial announcement of the Corporate Value-Up Program also mentioned the creation of the Korea Value-Up Index, which would comprise companies that have best adhered to the reform; South Korea’s stock market operator, Korea Exchange, launched the index in September 2024.

In July 2024, SFG’s management presented the company’s Value-Up Plan, marking the company as one of the first few in South Korea to embrace the Corporate Value-Up Program (the company was included in the Korea Value-Up Index during its inception and remains within). When the plan was formulated, SFG’s management realised that the company’s P/B ratio had shrunk over the years – from a high of 1.65 in 2001 to 0.45 in June 2024 – because of a decline in its return on equity from 13.7% to 8.6% over the same period. Management also realised that they needed to increase SFG’s profitability and return of capital to shareholders in order to raise the company’s P/B ratio to 1 or more. To this end, as part of the Value-Up Plan, management guided for SFG to achieve the following in 2027:

- An increase in the return on equity from 8.6% in 2023 to 10%

- An increase in shareholder return – which refers to share repurchases and dividends as a percentage of net income – from 36% in 2023 to 50%

- A decrease in the number of shares from 513 million in 2023 to 450 million through share buybacks

- 40% growth in tangible book value per share (TBPS) from ₩92,642 in 2023 to ₩130,000

We want to highlight two positive aspects of management’s 2027 targets for SFG:

- Management intends to improve SFG’s return on equity in a sensible way. SFG’s leaders want to maintain a strong balance sheet by keeping the financial conglomerate’s CET1 (Common Equity Tier 1) ratio above 13%. The CET1 ratio is one measure of the leverage, and hence the amount of financial risk, the company is taking on (it’s possible to increase a financial company’s return on equity by increasing its leverage, but doing so increases the financial risk it is exposed to). Management also wants to raise SFG’s return on equity through both structural reforms in the company’s non-banking businesses and returning capital to shareholders (returning capital to shareholders will lower the growth of the denominator in the return on equity equation).

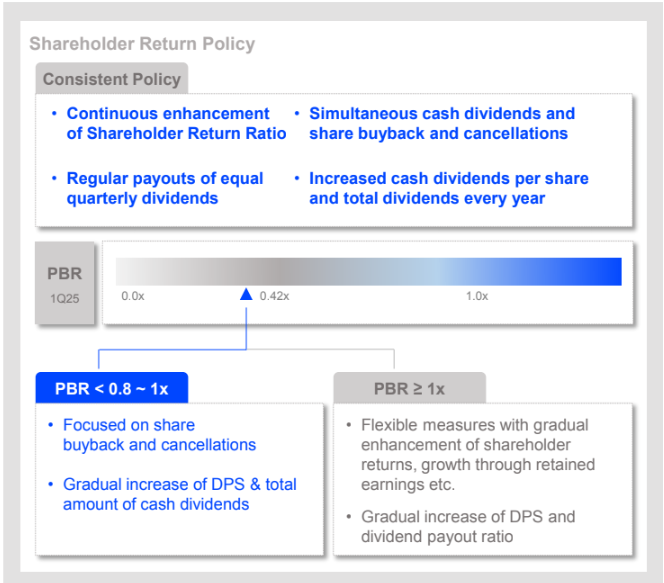

- When it comes to shareholder return, management will be focused on share buybacks only when SFG’s P/B ratio is less than 1, as shown in Figure 1 below. This shows that management has a keen understanding of when it’s appropriate to conduct share buybacks to generate shareholder value, since buying back shares at a P/B ratio of less than 1 will lead to an increase in SFG’s TBPS, ceteris paribus, whereas buybacks that occur when the P/B ratio is above 1 will lead to a decline in TBPS.

Figure 1; Source: SFG 2025 first-quarter earnings presentation

SFG’s management is committed to the Value-Up Plan. In SFG’s 2024 annual report, CEO Jin Okdong wrote:

“To resolve these issues, Korea’s Corporate Value-Up Program must continue—and succeed. Following last year’s 22nd National Assembly election, I met with foreign investors who asked how the program might evolve post-election. My answer was clear: “Korea’s Value-Up program must be understood in light of increasing pressure on the public pension system. With declining birth rates and an aging population, the current replacement rate remains in the low 40% range. Amid underperformance in capital markets, real estate has become the preferred vehicle for retirement savings, fueling price inflation and socioeconomic polarization. Unless Korea revitalizes its capital markets, this dynamic will persist. Therefore, expanding direct financing channels through capital markets for corporates is imperative—and there is broad consensus on this need.” In short, Korea’s commitment to the Value-Up program remains unwavering.

During SFG’s 2025 first-quarter earnings presentation, management provided an update to the Value-Up Plan: The targets for 2027 remained in place while targets for 2025 were given. For this year, SFG’s management will continue with share repurchases to bring the share count down, and is gunning for an ROE of at least 8.9% and a shareholder return of more than 42%.

It’s worth mentioning that President Lee Jae Myung has followed up with his rhetoric on wanting to eliminate the “Korea discount.” South Korea’s parliament revised the law earlier this month to place even more responsibility on a company’s board of directors in safeguarding minority shareholders’ interests.

If SFG meets the 2027 targets under the Value-Up Plan, it would have a TBPS of ₩130,000, which is around US$94 at the exchange rate of US$1 to ₩1,383 as of 21 July 2025. Our average purchase price for SFG’s US-listed shares was US$45. If SFG has a P/B ratio of 1 when its TBPS is at US$94 at the end of 2027, the upside from our average purchase price is more than 100%. SFG’s latest results at the time of our investment, for the first quarter of 2025, has its TBPS at ₩102,966, which translates to US$74 with the aforementioned exchange rate. This gives the company a P/B ratio of 0.6 at our average purchase price. It’s possible that SFG’s P/B ratio starts to rise rapidly from 0.6 to around 1 way before the end of 2027, in which case Compounder Fund would also earn a handsome return. But this raises two important questions: Is it likely for SFG to achieve its 2027 targets, and why should SFG’s P/B ratio rise to 1?

Meeting the 2027 targets

SFG has so far made promising progress toward the 2027 targets. In 2024:

- SFG’s shareholder return was 40%, up from 36% in 2023

- SFG’s share count declined from 513 million to 499 million

- SFG’s TBPS increased by 8% from ₩92,642 to ₩100,096

- SFG’s return on equity dipped slightly from 8.6% in 2023 to 8.4%, which is the only negative development

Meanwhile, in the first quarter of 2025:

- SFG’s return on equity increased from 10.4% a year ago to 11.4%

- SFG’s share count declined further to 493 million

- SFG’s TBPS stepped up by 3% sequentially, and by around 9% from a year ago, to ₩102,966

We also think that the compensation structure of SFG’s management incentivises them to achieve the 2027 targets. For example, SFG CEO Jin Okdong’s compensation in 2024 had two components, which are ₩1.52 billion (around US$1.1 million) in salary, and a grant of 23,587 performance shares. The performance shares are virtual shares and the total amount of performance shares that will ultimately be awarded to Jin depends on the performance of SFG (this includes the company’s relative stock price performance, its return on equity, and its non-performing loans ratio, among other measures) over a four-year period starting from 2024. Upon determining the performance of SFG for the relevant time period, Jin will receive cash based on the number of performance shares he is awarded and the company’s stock price at that point in time. For perspective, the 23,587 performance shares granted to Jin in 2024 were worth US$1.06 million based on our average purchase price of SFG shares of US$45 and this value is similar to Jin’s salary in 2024. In other words, a material portion of Jin’s compensation is tied to multi-year improvement in the company’s return on equity (among other metrics); changes in SFG’s return on equity, as we mentioned earlier, should have an important influence on the company’s P/B ratio.

There are other aspects to Jin that add to our confidence in SFG’s ability to fulfill its Value-Up Plan. Although he has only been CEO of SFG since March 2023, he likely understands the company’s businesses really well, having joined Shinhan Bank nearly 40 years ago in 1986. In early-February 2024, before the Financial Services Commission announced the Corporate Value-Up Program, he was already publicly discussing the importance of increasing SFG’s dividends and share buybacks in improving the return on equity. These are Jin’s comments on the matter in an 8 February 2024 interview with Bloomberg:

“David Ingles: Do you think your stock is undervalued? And if you think it’s undervalued, it’s undervalued by how much?

Jin Okdong: It’s true that we are very undervalued right now because our PBR is around 0.41. It’s hard to put a number on it, but I think the PBR should go up to a point where it’s recognized by the market. It’s hard to put a number on it though.

David Ingles: I need to ask you now about your plans on boosting shareholder value. What plans do you have to give back money to investors?

Jin Okdong: Our strategy is to continue to increase our total return to shareholders a little bit from 2023 onwards. We did a share buyback every quarter, and if you look at our total shareholder return, including the share buyback, it was about 36%. So this year we’re going to continue our commitment to our shareholders that we made last year, that we’re going to continue to buy back shares and cancel shares every quarter, regardless of how the economy does. If we can do that, our goal for this year is – I don’t know if we’re going to achieve it this year or not – we’re aiming to clear 40% first.

David Ingles: Why buybacks and not dividends?

Jin Okdong: In order to restore the share price resiliency, we need to reduce the share float. First of all we need to continue the treasury stock cancellation so that we can take back some of the outstanding shares. Then we can boost the share price and the ROE will increase, increasing our shareholder value. Our first target is reducing the share float to below 500 million and to about 450 million shares. That’s about 20% cancellation of stocks from the current level. It would take several years but that’s a plan. Regulators are taking a stance that they would not be involved in a big way with shareholder returns, as long as there is sufficient capital. I don’t think our plan would be hard, as the Value-Up program is coming up. The mood is favorable.”

History’s rhymes

South Korea’s Corporate Value-Up Program is inspired by Japan’s corporate reform efforts. Japan has been engaged in corporate reform since 2014 but the intensity ramped up in March 2023. That was when the Tokyo Stock Exchange requested Japanese companies listed on the Prime and Standard Markets to raise their capital efficiency (referring to measures such as the return on equity and return on invested capital) and valuations (referring to measures such as the P/B ratio or price-to-earnings ratio) if they are low, through actions such as conducting share buybacks, hiking dividends, and driving fundamental improvements in profitability. The Tokyo Stock Exchange tightened the screw in early-2024 when it started a monthly list, naming companies that have complied with the request and effectively shaming companies that have not.

Japan’s four largest public-listed banks are Mitsubishi UFJ Financial Group, Sumitomo Mitsui Financial Group, Mizuho Financial Group, and Japan Post Bank. They have all heeded the Tokyo Stock Exchange’s request, as shown in the quotes below from their recent annual reports.

From Mitsubishi UFJ Financial Group’s annual report for the financial year ended 31 March 2024 (emphases are ours):

“During the previous MTBP period, we strengthened the earnings power and resilience of our business model. In the final year of the previous MTBP, the ROE reached 8.5%, notably exceeding the 7.5% target.We remain committed to improving the ROE in the new MTBP and aim to achieve around 9% ROE in fiscal 2026…

…Dividend per share for FY2023 was increased to 41 yen from 25 yen in FY2020. In addition, we repurchased a total of 1 trillion yen shares during the previous MTBP period, with the total shareholder return exceeding 2.2 trillion yen. We will continue tostrive for improvement in shareholder value through sustainable improvement of ROE with disciplined capital management and the earnings per share…

…Price Book-value Ratio (PBR) has improved from the 0.4X range and has been trending close to 1.0X since the start of 2024, but still remains under 1X. We believe this is attributable to our ROE falling short of the Cost of Capital. Looking at global banks and the relationship between their PBRs and ROEs, as shown in the diagram below, some U.S. banks whose TSR has remained high over the past decade are appreciated by the market for their robust PBR, which results from ongoing improvement in ROE.”

From Sumitomo Mitsui Financial Group’s annual report for the financial year ended 31 March 2024 (emphases are ours):

“Our share price has risen significantly over the past year, and our PBR (Price to Book Ratio) recovered from 0.58 as of the end of FY2022 to 0.86 as of the end of FY2023. Furthermore, it reached to 1.0 in July 2024. However, as Group CEO, I firmly believe that this is an issue I must continue to improve. While financial institutions’ share prices are quite susceptible to changes in the macro-environment, we will strive to raise both our ROE and PER (Price Earnings Ratio) so that we are able to maintain a PBR over 1.0, even under a challenging business environment…

…To improve PBR, we have to improve PER in addition to boosting ROE. We will further evolve our policy of “Transformation & Growth” which continues from the previous Plan and focus on businesses that will lead to medium- to longterm growth, for example Olive, the global CIB business, and our Multi-Franchise Strategy. Through these efforts we will expand our growth momentum and increase our expected growth rate. In addition, we must control our capital costs to improve our PER and rebuilding our corporate infrastructure is a key part of this initiative…

…The optimal distribution of capital is an important factor in enhancing ROE. We will pay even closer attention to balancing shareholder returns and investment for growth while maintaining financial soundness. Dividends remain our principal approach to shareholder returns and we will maintain our progressive dividend policy and dividend payout ratio target of 40% while realizing an increase in dividend payments by growing our bottom-line profit. We have increased our dividend forecast for FY2024 by ¥60, from ¥270 to ¥330 per share to maintain a dividend payout ratio of 40% based on our bottom-line target over ¥1 trillion. Under a policy of engaging in flexible share buybacks, we announced a buyback program of ¥100 billion in May 2024. We will consider additional share buybacks during the fiscal year based on various factors.”

From Mizuho Financial Group’s annual report for the financial year ended 31 March 2024 (emphases are ours):

“As well, our replacement of low-profit assets and selling off of crossshareholdings, among other initiatives, have improved our capital efficiency and our price-to-book (P/B) ratio. We now have a structure in place for proactively utilizing capital towards further accelerating growth while also enhancing shareholder returns…

…Mizuho’s price-to-book (P/B) ratio has been trending upwards, supported by improvements in ROE and expectations for sustainable growth, but it has still not reached a value of 1. Bringing our P/B ratio above 1 is one of the top priorities of executive management. We take the current situation very seriously and are committed to returning our P/B ratio above 1 as quickly as possible. We are aiming to do this by further improving ROE and reducing the cost of capital. Towards achieving these two aims, we are improving return on risk-weighted assets (RORA), controlling the Common Equity Tier 1 (CET1) Capital Ratio, mitigating volatility, and taking steps to generate growth expectations.”

From Japan Post Bank’s annual report for the financial year ended 31 March 2024 (emphases are ours):

“Our price book-value ratio (PBR) is currently less than 1x which we consider as one of our major issues at the management level. At first, I would like to devote all our efforts to steadily increasing ROE and to increase PBR, it is imperative to improve the expected growth rate.”

“As a typical indicator of market value, the Bank’s price book-value ratio (PBR) stood at 0.61 x (as of March 31, 2024), far below a factor of 1x. Similarly, total shareholder returns (TSR) also stood at a lower level than other major banks. We believe that the major factor behind these shortcomings was the fact that our ROE has continually trended below 5%, the cost of shareholders’ equity as recognized by the Bank. With two years left, we therefore revised the Medium-term Management Plan with the goal of significantly improving ROE.”

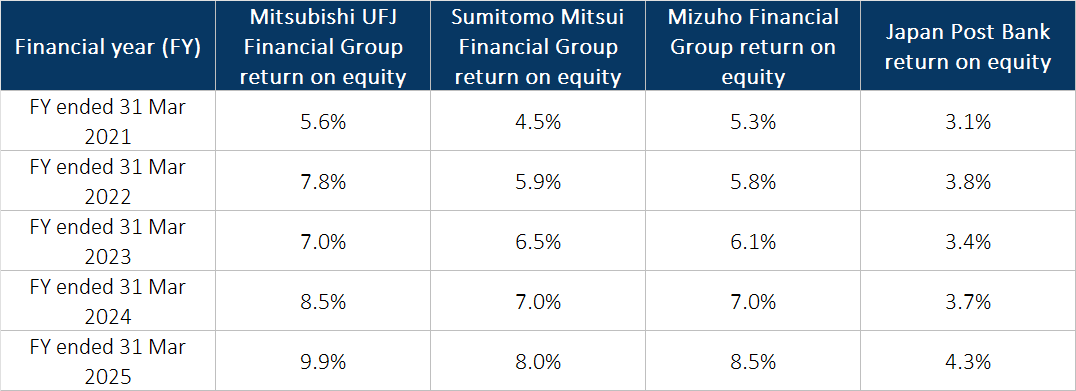

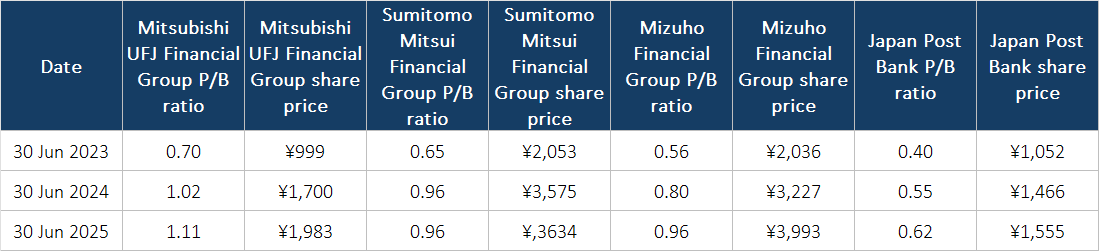

Table 1 below shows the clear upward trend in the Japanese banks’ returns on equity in the past few years, especially after the Tokyo Stock Exchange requested for corporate reforms (this would refer to the financial years ended 31 March 2024 and 31 March 2025). In particular, Mitsubishi UFJ Financial Group’s return on equity is now a hair’s breadth below 10% while Sumitomo Mitsui Financial Group and Mizuho Financial Group’s returns on equity have reached the high single-digit percentage range. Table 2 shows the four Japanese banks’ P/B ratios and share prices in June 2023 (shortly after the Tokyo Stock Exchange issued its reform request), June 2024, and June 2025.

Table 1; Source: Banks’ earnings presentations and annual reports

Table 2; Source: Banks’ quarterly earnings reports and Yahoo Finance

As it turns out, the Japanese banks’ P/B ratios in June 2023 are similar to SFG’s P/B ratio at the time of our investment. By June 2024, the P/B ratios of the Japanese banks had largely approached or exceeded 1 and were maintained at a similar level in June 2025. The exception was Japan Post Bank, whose P/B ratio was still far from 1, but had nonetheless increased by more than 50% from 0.40 to 0.62. The big gap from 1 in Japan Post Bank’s P/B ratio makes sense to us. Japan Post Bank’s return on equity, despite having improved, remains low, unlike the other three Japanese banks. The increases in the four Japanese banks’ P/B ratios between June 2023 and June 2025 also drove healthy gains in their share prices over the same time period, with the lion’s share of the share price gains occurring between June 2023 and June 2024.

There is no guarantee, but we think the recent experience of the large public-listed Japanese banks is instructive for what could happen with SFG. It’s likely, in our view, that SFG’s P/B ratio can trace a similar arc as what the Japanese banks’ P/B ratios have done in the recent past if the Korean financial conglomerate’s return on equity improves according to the Value-Up Plan.

The risks involved

Real estate project financing (PF) is a longstanding problem in South Korea’s economy. It is a financing method where a real estate developer borrows nearly all the capital needed for a real estate project and where the repayment of the debt is based on the expected future cash flows of the project. According to research published in June 2024 by the Korea Development Institute (KDI), a think-tank related to the South Korean government that focuses on analysing the country’s economy, a real estate developer in South Korea utilising PF for a project typically borrows 97% of the entire capital needed, unlike in major developed economies where only 60%-70% of a project’s cost is borrowed. The KDI research report also laid out the size of the PF exposure in South Korea* and how numerous economic crises in the country have been triggered by this risky form of financing over the years:

“In four years, PF exposure, encompassing both loans and guarantees, surged to approximately 160 trillion Korean won, up from below 100 trillion won in 2019… When quasi-PF loans, such as those collateralized by land and loans from the Community Credit Cooperatives, or Saemaul Geumgo, are included, the total exposure climbs to a staggering 230 trillion won…

…PF insolvency is at the heart of the 2011 savings bank crisis, which led to bank runs that triggered the collapse of about 30 savings banks, affecting over 100,000 customers. In 2013, alarming growth in PF exposure, especially in the nonbanking sector, raised calls for interventions to mitigate risk. By 2019, large-scale debt guarantees provided by securities firms to PF projects became a notable concern. In 2022, the Legoland crisis set off a credit crunch in the bond market.”

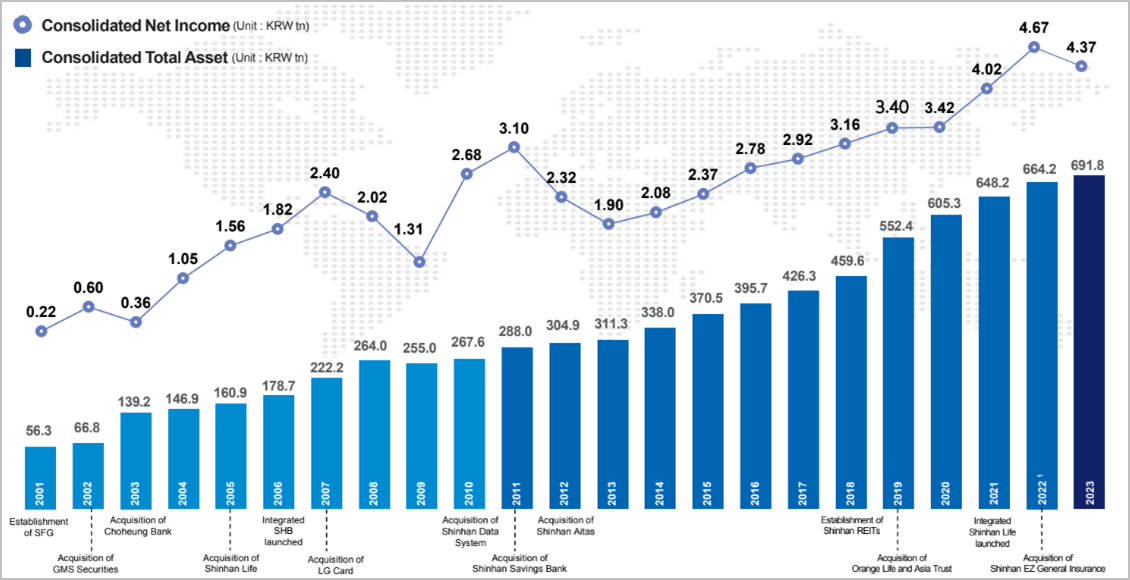

Any future blowups related to real estate PF in South Korea could negatively impact SFG both directly and indirectly. For the direct impact, SFG had material PF exposure of ₩9.6 trillion as of end-2024, but it is not an overwhelming amount when compared to the company’s total assets and shareholders’ equity of ₩739.8 trillion and ₩56.1 trillion, respectively, at the same point in time. For the indirect impact, South Korea’s economy might experience setbacks if there are any troubles with real estate PF, which would then likely lead to a downturn in business for the country’s banks. But we’re comforted by the fact that since 2001, SFG’s net income has been positive every year and has been growing, albeit slowly; these are shown in Figure 2 below (Figure 2 extends only to 2023, but SFG’s net income was ₩4.52 trillion in 2024). It’s worth noting that South Korea’s economy had endured some difficult moments in this time period, especially in 2008, when the country experienced a 5.1% decline in economic output in the fourth quarter of the year, and in 2009, when the country’s GDP (gross domestic product) experienced a meagre increase of just 0.9% for the year. SFG’s net income fell by 16% and 35% in 2008 and 2009, respectively, but the net income in both years were still significant.

Figure 2; Source: SFG 2024 Value-Up Presentation

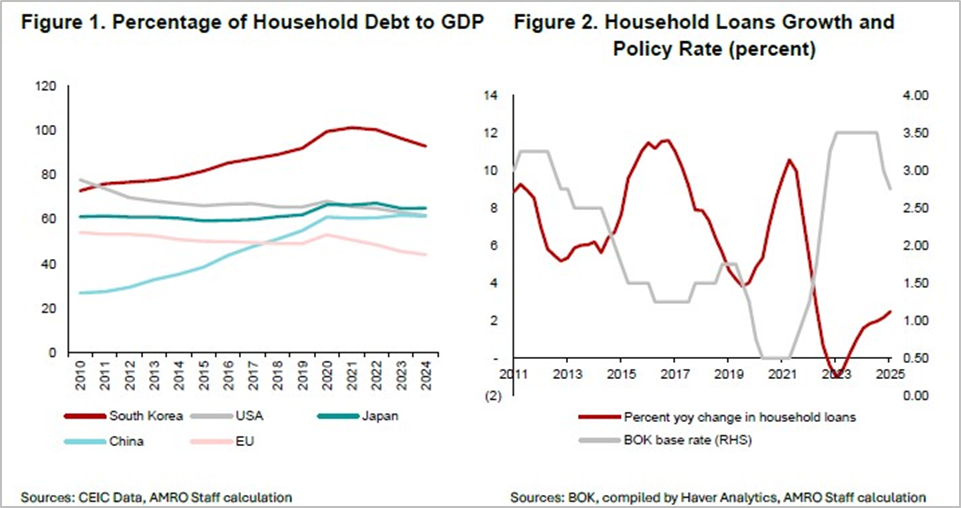

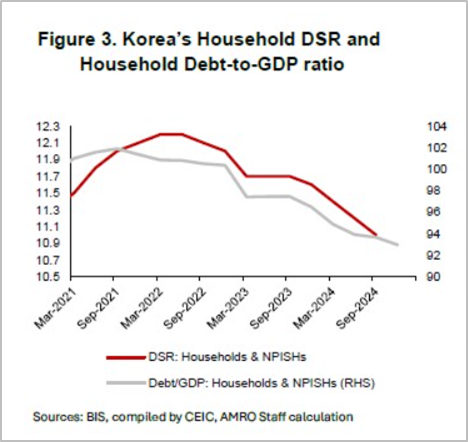

Apart from real estate PF, South Korea’s economy has other problems related to the use of debt. In particular, South Korea’s household-debt-to-GDP ratio is one of the highest among developed economies, according to the ASEAN+3 Macroeconomic Research Office (AMRO), a research organisation focused on macroeconomics that was established in 2011 by the finance ministries of China, Japan, Korea, and the 10 member states of ASEAN. This can be seen in Figure 3 below. The good thing here is that South Korea’s household-debt-to-GDP ratio, as well as the debt service ratio, have both declined in recent years, as illustrated in Figure 4.

Figure 3; Source: AMRO research

Figure 4; Source: AMRO research

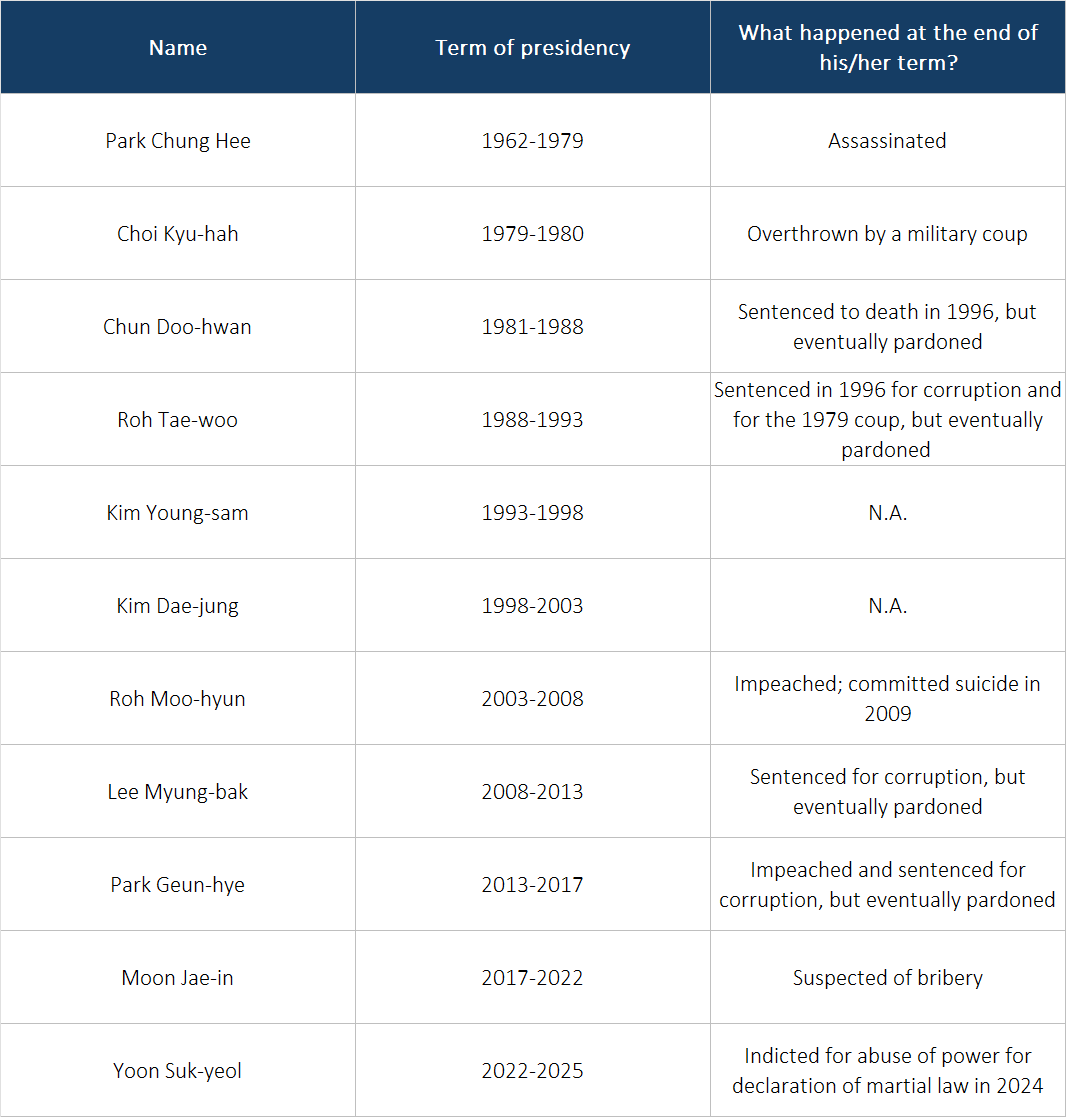

Political instability in South Korea is another risk that we see with our investment in SFG. Many of the country’s past presidents have been plagued with scandals, with one of them even being assassinated, as shown in Table 3 below.

Table 3; Source: Al Jazeera and Channel News Asia

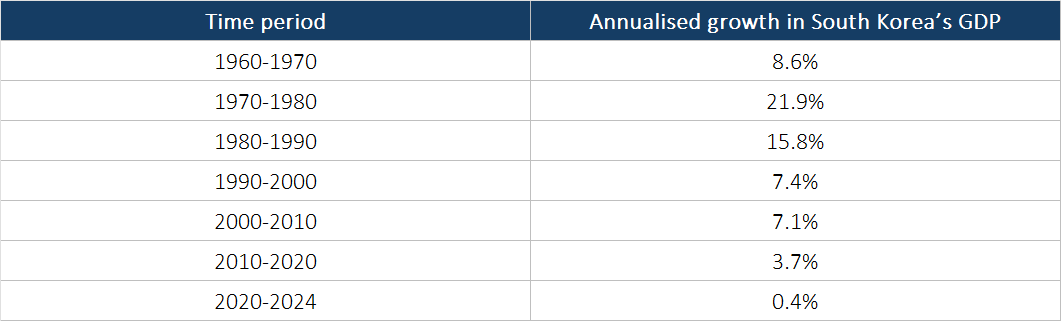

Yoon Suk-yeol, who was South Korea’s President when the Corporate Value-Up Program was launched, was indicted for abuse of power earlier this month for his declaration of martial law in 2024. Table 4 shows that South Korea’s economy has managed to grow over the years despite the political instability. But any future shakeups in the country’s seat of highest power may spill over into the economy.

Table 4; Source: World Bank

Uncertainty over the USA’s tariff policies under the Trump administration is a risk we’re watching too. The Trump administration’s tariffs have so far appeared to be implemented haphazardly and erratically. If the finalised tariffs for all of the USA’s major trading partners ends up causing a global economic slowdown, South Korea may not be spared. And specifically for South Korea, the country’s exports to the USA was US$128 billion in 2024, according to Trading Economics, with the USA being the Asian nation’s second-largest export market for the year, accounting for 20% of total exports. If the Trump administration ends up setting a huge tariff on South Korean imports into the USA, South Korea’s economy could suffer, in turn leading to pain for SFG’s business.

*PF and financing structures of similar ilk in South Korea had ballooned to ₩230 trillion according to research from the KDI published in June 2024; for perspective, the country’s GDP was ₩2,236 trillion in 2023 according to the Asian Development Bank.

Summary and allocation commentary

We invested in SFG because we think it is in the midst of a regulatory-driven change that makes it a good bargain. South Korea’s government wants to see the country’s public-listed companies improve their valuations sustainably and SFG has heeded the call with its Value-Up Plan that was first announced in July 2024. Our average purchase price of US$45 for SFG’s shares is significantly lower than what the stock price could be if SFG’s P/B ratio reaches 1 in the event its TBPS for 2027 reaches the Value-Up Plan target of ₩130,000 (or around US$94 at the exchange rate of US$1 to ₩1,383 as of 21 July 2025). Moreover, SFG’s shares had a P/B ratio of merely 0.6 at the time of our investment, which creates potential for a healthy return if the company’s P/B ratio rises close to 1 in the near future before 2027.

There are risks to note with SFG, such as the various aspects of high leverage lurking in South Korea’s economy, frequent political instability in the country, and the potential effects from the USA’s tariffs.

On the back of all this information, we decided to allocate around 3% of Compounder Fund’s portfolio into SFG at our initial investment. We made SFG a medium-sized position because the valuation of the company looks compelling to us but we are mindful of the risks involved.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Besides Shinhan Financial Group, Compounder Fund does not own shares in any other companies mentioned. Holdings are subject to change at any time.