Compounder Fund: Medpace Investment Thesis - 31 Aug 2022

Data as of 29 August 2022

Medpace Holdings (NASDAQ: MEDP), which is based and listed in the USA, is a company in Compounder Fund’s portfolio that we invested in for the first time in August 2022. This article describes our investment thesis for the company.

Company description

Developing a new drug for commercialisation in the USA requires an arduous journey. According to Pharmaceutical Research and Manufacturers of America’s 2015 Biopharmaceutical Research Industry publication, it takes at least 10 years and around US$2.6 billion to develop a new drug. A long time is needed because a new drug has to undergo an extensive series of tests and reviews that are under the purview of the US Food & Drug Administration (FDA). Among these tests and reviews are clinical trials that are grouped into four different phases, namely, Phase I to IV:

- Phase I trials typically involve 20 to 80 subjects, who are mostly healthy individuals (with the occasional patient), and last a few months to several years. The purpose of a Phase I trial is to investigate the basic safety and metabolism profile of a new drug. If the drug scores well, generally a Phase II trial will be initiated.

- Typically, a few hundred patients will be involved with a Phase II trial and the average trial length is 12 to 18 months. Phase II trials are primarily designed to study a drug’s possible adverse effects, safety risks, dosage, and efficacy. These trials can sometimes be divided into two phases, namely, Phase IIa and Phase IIb. The former evaluates patients’ dose responses to the drug while the latter studies the drug’s efficacy at different doses. If results from a Phase II trial show that a drug may be safe and effective, a Phase III trial generally follows.

- A Phase III trial, which lasts from one to three years on average, generally involves thousands of patients from different geographies. This is when a drug’s overall benefit-to-risk ratio is studied and the basis for regulatory approval is established.

- Lastly, there are Phase IV trials, which are for investigating a drug’s long-term risks and benefits, dosage levels, and more. The patient population for a Phase IV trial is typically in the thousands, and each trial can last anywhere from six months to several years. Drugs that have previously been approved may still be called by the FDA to undergo Phase IV testing and surveillance.

To run these Phase I-IV trials for a drug, a drugmaker will have to perform a wide variety of tasks, such as designing a study plan, running laboratories, monitoring patients, managing the project, communicating with regulators, and more. This is where Medpace can help. Medpace is a contract research organisation (CRO) that provides a full range of services to support a drugmaker’s entire clinical development journey for a drug from Phase I through to Phase IV trials. Some examples of Medpace’s services are:

- A medical department that provides: Advice for the design and planning of a drug study; training of operational staff; cooperating with investigators; medical monitoring of trial participants; and handling meetings with regulatory bodies

- Clinical trial management, where Medpace manages all aspects of a drug study programme

- Feasibility studies for the best countries and sites to use for investigating a drug (a site is a healthcare facility that have doctors who are running clinical trials)

- Study Start-Up services such as submission of study documentation to regulatory bodies and contract negotiations with sites

- Recruiting and retaining patients for trials

- Clinical monitoring, where Medpace’s clinical research associates (CRAs) monitor sites either physically or virtually

- Medical writing where Medpace develops study protocols and clinical and statistical reports, among other documents

- Biometrics and data services which sees Medpace collect, manage, and analyse data related to a drug’s trial

- Pharmacovigilance where Medpace collects, studies, and reports safety information related to a drug’s trial

- Laboratories where Medpace runs medical tests

Drugs can be broadly separated into two groups: Small Molecules, and Biotechnology. Small molecule drugs are made through synthesis of chemicals and this has been the main way drugs were – and still are – discovered and developed. Meanwhile, biotechnology drugs, or biologics, are derived from living organisms and can comprise of sugars, proteins, and/or nucleic acids. Prominent examples of biologics today would be the mRNA vaccines for COVID-19 that were developed by Moderna and BioNTech/Pfizer.

To access Medpace’s services, drugmakers enter into contracts that range from a few months to several years. Under these contracts, Medpace’s customers pay a fixed fee or on a per-unit-of-service basis. It’s worth noting that Medpace’s management team focuses on a full-service model, where a drugmaker effectively outsources the entire process for for a drug’s clinical trial to the company. Medpace classifies its customers into three groups according to size, namely, large pharmaceutical companies (the top 20 by global prescription drug sales), mid-sized biopharma companies (companies with at least US$250 million in annual sales but are not in the top 20), and small biopharma companies (those with less than US$250 million in annual sales).

In 2021, Medpace earned US$1.14 billion in revenue, of which 7% came from large pharma companies. Mid and small biopharma companies accounted for 16% and 77%, respectively, of Medpace’s revenue for the year. From this, it’s clear that Medpace focuses on serving smaller drugmakers. In fact, the lion’s share of Medpace’s customers are currently pre-revenue biologic companies. This is a risk, which we’ll discuss in more depth in the “The risks involved” section of this article. The good news here is that Medpace does not have customer-concentration. No customer accounted for more than 10% of Medpace’s revenue in 2021, and its top 10 customers collectively accounted for just 24% of total revenue.

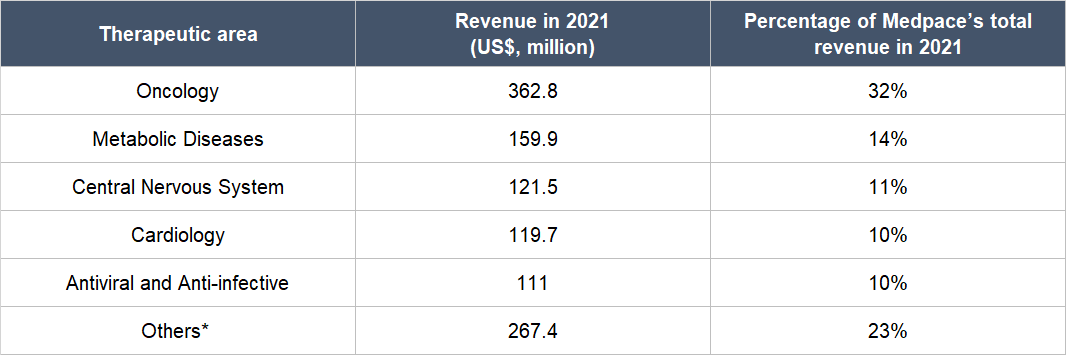

Drugs can also be categorised under different therapeutic areas and the ones Medpace specialises in are Oncology (the study and treatment of cancer), Metabolic Disease (the treatment of issues that disrupt metabolism, which is the process of the human body converting food to energy), Cardiology (the treatment of heart disorders), Antiviral and Anti-infective (the prevention and treatment of infections), and Central Nervous System (the treatment of problems related to the human body’s central nervous system, which is made up of the brain and the spinal cord). Table 1 shows a breakdown of Medpace’s 2021 revenue by therapeutic area:

Table 1; Source: Medpace annual report

*Others primarily includes Nephrology, Rheumatology, Musculoskeletal, Dermatology, Gastroenterology, and Ophthalmology

Although Medpace has operations across the globe (in North America, Europe, Africa, Asia-Pacific, and Latin America), the USA accounts for an overwhelming percentage of its total revenue. In 2021, this was 97%.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Medpace.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

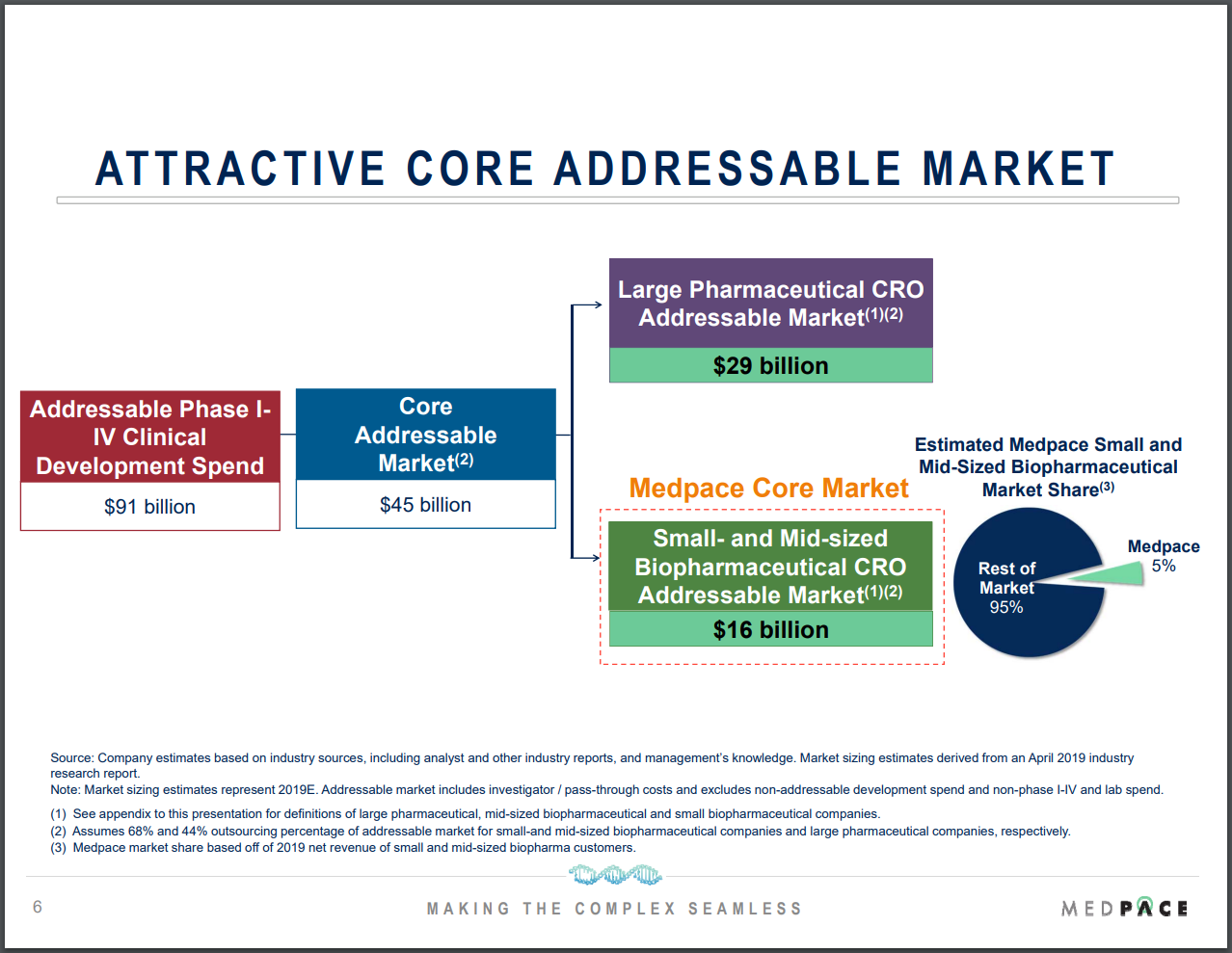

Medpace is tackling a market that we think is both large and growing. In a June 2020 investor presentation (see Figure 1 below) Medpace estimated that its core market of outsourced CRO services for small- and mid-sized biopharma companies was US$16 billion, using data from an April 2019 industry report. For perspective, Medpace’s trailing revenue of US$1.29 billion as of 30 June 2022 is merely 8% of the estimated market opportunity.

Figure 1; Source: Medpace June 2020 investor presentation

We think it’s highly likely that Medpace’s core addressable market would be materially larger in the years ahead. According to Pharmaprojects’ Pharma R&D Annual Review 2022 report, the total number of drugs in the global research and development (R&D) pipeline more than tripled from 5,995 in 2001 to 20,109 in 2022. This is shown in Figure 2.

Figure 2; Source: Pharma R&D Annual Review 2022

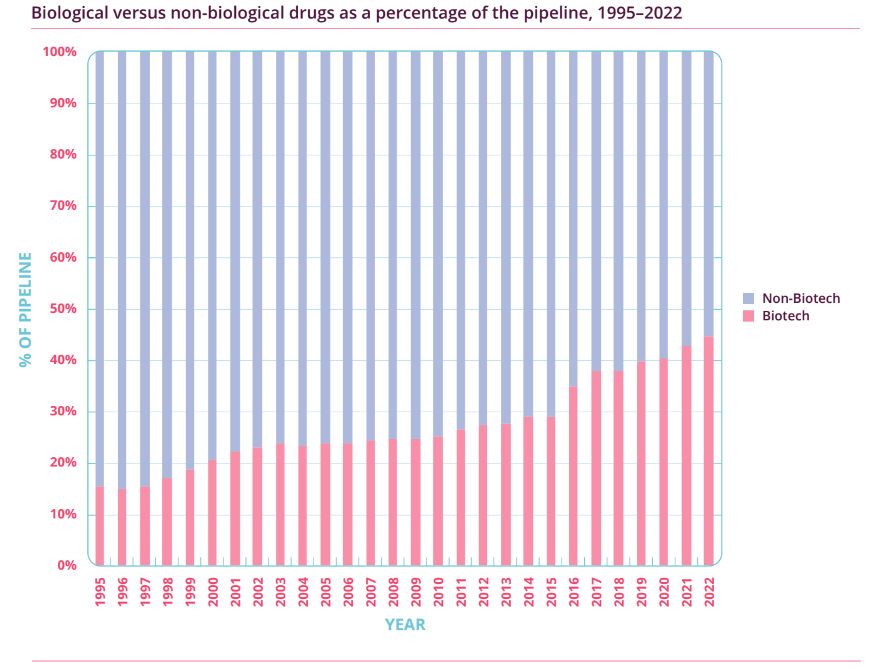

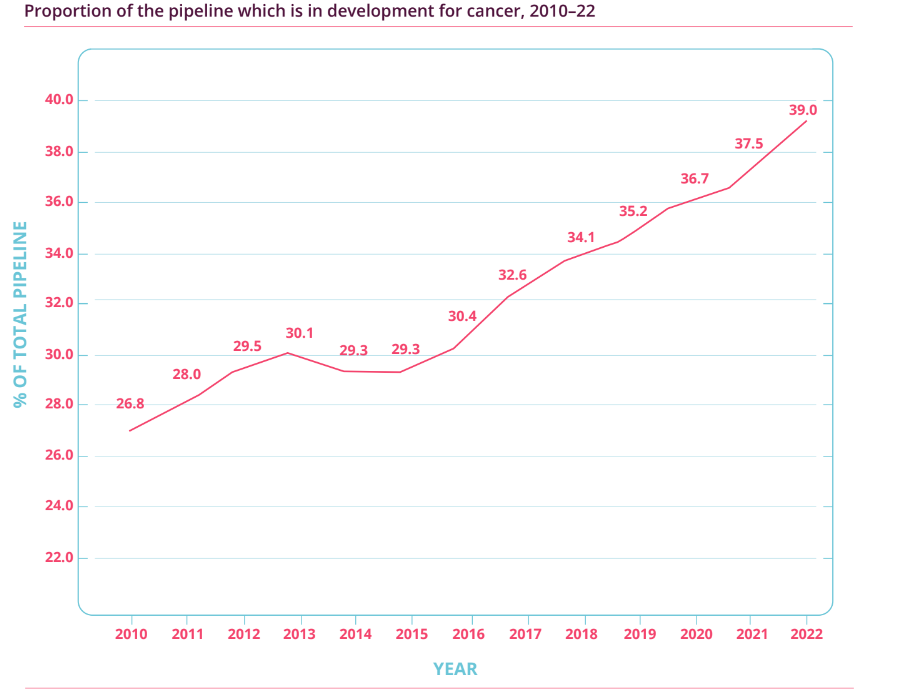

Importantly, as Figure 3 illustrates, the percentage of biotechnology drugs in the overall R&D pipeline has also soared from just over 20% in 2001 to around 45% in 2022. This means that biotechnology drugs, or biologics, have been the key driver for the growth seen in pharmaceutical R&D activity. Meanwhile, Figure 4 shows that the proportion of cancer-related drugs in the overall R&D pipeline has also increased significantly (from 26.8% to 39.0%) over the past dozen years. As a reminder, Medpace’s current core customers are drugmakers that focus on developing biologics, and oncology is the company’s most important therapeutic area. It’s also worth noting that the USA – Medpace’s most important geographical source of revenue – has been dominating the R&D landscape. According to Pharmaprojects, 49% of drugmakers with drugs in the R&D pipeline were based in the USA in 2013; this self-same percentage was 44% in 2022.

Figure 3; Source: Pharma R&D Annual Review 2022

Figure 4; Source: Pharma R&D Annual Review 2022

We also think that recent advances in DNA analysis and the understanding of proteins could be a long-term tailwind for the development of biologics. In our January 2021 investment thesis for Illumina, the global leader in the development of DNA sequencing machines, we wrote:

“Since 2007, Illumina has reduced the cost of sequencing by more than a factor of 10,000, and the time needed for sequencing by a factor of around 12,000. For perspective, Illumina has brought the cost of sequencing one genome down from US$15,000 in 2010 to less than US$1,000 today…

…A few examples of exciting new areas for Illumina are the related fields of population genomics, genetic diseases, and oncology (the study and treatment of cancer). Illumina estimates that today, only 10 million-plus people are in research cohorts for population-wide genomic studies. But greater adoption of DNA sequencing in healthcare systems around the world (involving up to four billion people annually) could be happening in the near future, driven by findings from the research on population genomics. DNA sequencing could become part of routine clinical care and help improve healthcare economics and patient outcomes.

On genetic diseases, DNA sequencing is still rarely used (in less than 1% of cases) and a diagnosis typically takes upwards of five years. Inefficiencies in the management of genetic diseases imposes a US$57 billion cost on society. It makes sense to us that the use of DNA sequencing in managing genetic diseases would become increasingly widespread over time.

Moving to oncology, global spending on cancer drugs was a staggering US$150 billion in 2018 and projected to increase to nearly US$240 billion by 2023, according to IQVIA, a provider of data analytics services to the life sciences industry. DNA sequencing could have a big role to play in humanity’s war on cancer, given that the technology can be used for early screening, therapy selection, and disease-monitoring. To-date, the penetration rates for DNA sequencing in these three use-cases in oncology are still really low (all less than 8%), as shown in the chart below.”

During Illumina’s earnings conference calls for the first and second quarters of 2022, the company’s leaders shared that there’s now a clear line of sight for the company to bring the cost of analysing a genome down to the hundred-dollar range. This could further accelerate society’s grasp of the human genome (the complete DNA of human kind), and thus, the genetic diseases that plague all of us as well as any biologically-derived cures for these ailments.

On the understanding of proteins, Deepmind, a subsidiary of Alphabet that specialises in artificial intelligence (Alphabet is the parent of search engine giant Google), is doing tremendous work. Through its artificial intelligence engine, Deepmind is now able to predict the structure of nearly every protein discovered by scientists thus far – this amounts to more than 200 million structures – and it’s providing this data for free. Proteins are molecules that direct all cellular function in a living organism, including of course, humans. A protein’s structure matters because it is what allows the protein to perform its job within an organism. In fact, diseases in humans can be caused by mis-structured proteins. Understanding the structure of a protein thus means knowing how it could affect the human body. Biologics tend to manipulate proteins, or the production of proteins, within the human body. And as we mentioned in the “Company description” section of this article, biologics can be composed of proteins too.

We believe that Medpace has a good chance of benefiting from the potential growth of its core addressable market over time for two key reasons:

- First, according to expert calls on Medpace and the CRO industry that we have reviewed, smaller biopharmas tend to lack the necessary knowledge required to run drug trials well. This is where Medpace can provide value to its core customer-group. The company, as mentioned in the “Company description” section of this article, provides a full range of services to support all of a drugmaker’s needs during a drug’s clinical trials.

- Second, one of the experts in the calls we reviewed – an ex-senior employee of Medpace who worked at the company for nearly eight years – shared that Medpace’s pricing for its services was never the lowest whenever it was competing with other CROs for contracts. But as we’ll show in the “A management team with integrity, capability, and an innovative mindset” subsection of this article, Medpace has managed to grow its backlog, net new business awards, and revenue substantially over time. This suggests to us that Medpace has a high level of expertise in the services it’s providing, and its customers value this expertise.

2. A strong balance sheet with minimal or a reasonable amount of debt

Medpace ended the second quarter of 2022 with US$42.6 million in cash but total debt of US$249.7 million. On the surface, this looks like a shaky balance sheet, since the amount of debt substantially outweighs the level of cash.

But we think there is a positive reason for the weakness seen in Medpace’s balance sheet: The company had borrowed heavily in recent times to repurchase its shares. For perspective, Medpace ended 2021 with US$461.3 million in cash and zero debt. The net-cash position flipped after the company spent US$800.7 million in the first half of 2022 for share buybacks, which caused its weighted average diluted share count to fall by 10.7% from 37.741 million in the fourth quarter of 2021 to 33.695 million in the second quarter of 2022. Medpace also has a long history of generating strong operating cash flow and free cash flow (see the “A proven ability to grow” subsection of this article) which makes us comfortable with the current debt load.

3. A management team with integrity, capability, and an innovative mindset

On integrity

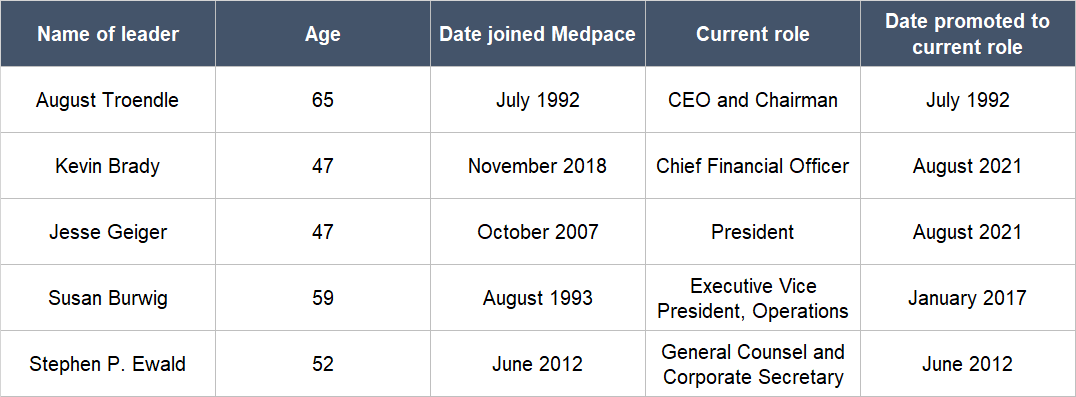

Medpace was founded in July 1992 by Dr. August Troendle as a CRO to help drugmakers with their Phase II to Phase IV trials. Troendle, who has been the CEO and Chairman of Medpace since its founding, has a medical degree. Prior to Medpace, he was a Medical Review Officer for the FDA from 1986 to 1987 and was a senior leader at a pharma company – Sandoz (Novartis) – from 1987 to 1992, where he was helping to develop lipid altering agents. We appreciate Troendle’s long tenure leading Medpace, as well as his education and experience in areas that are related to Medpace’s business.

Table 2 below shows all of Medpace’s key leaders – including Troendle – and a few positive traits about them: (a) They have all been at the company for a number of years, some more than a decade; (b) some of them are relatively young, being only in their late forties; and (c) most of them were promoted to their current roles.

Table 2; Source: Medpace website and regulatory filings

Medpace compensates its key leaders in three ways: Through a base salary (given in cash), an annual cash bonus, and long-term incentive awards (given in shares or options). As far as we can tell, there are no publicly-available details on the performance targets for management that determine the level of the long-term incentive awards they are given in each year. But we think the following traits of the total compensation of Medpace’s key leaders in 2021 help align their interests with the company’s shareholders and thus speak positively to their integrity: (a) The long-term incentive awards for the year made up the majority of the annual compensation for each of Medpace’s key leaders, as shown in Table 3, (b) the awards, which are options, vest in two years for Troendle and Burwig, and four years for Brady, Geiger, and Ewald, and (c) the total compensation for each of Medpace’s key leaders in 2021 is only a small percentage of the company’s free cash flow of US$235.1 million for the year.

Table 3; Source: Medpace annual filings

Another positive sign on management’s integrity is the skin in the game that Troendle has. As of 29 August 2022, Troendle controlled 6.320 million shares of Medpace, which have a market value of US$980.0 million at Medpace’s stock price of US$155 on the same date.

We do note that there were related-party transactions in 2021, amounting to US$13 million, involving Medpace and entities that are related to Troendle:

- Medpace incurred travel expenses of US$1.3 million in 2021 that went to a private aviation company controlled by Troendle.

- Medpace leases a number of buildings – including the company’s headquarters – from entities controlled by Troendle and his family. The lease expenses associated with these properties was US$11.4 million in 2021.

- Medpace spent US$0.3 million in lodging expenses in 2021 on a hotel – The Summit Hotel – that is owned by Troendle and located in Medpace’s headquarters.

We are typically wary of high levels of related-party transactions because their presence could indicate that a company’s leaders are enriching themselves at the expense of the company’s other shareholders. But on balance, we think Medpace’s related-party dealings do not reflect poorly on the integrity of the management team. The related-party transactions were less than 10% of both Medpace’s net income (US$181.8 million) and free cash flow (US$235.1 million) in the same year. Moreover, the company’s net income and free cash flow margins (net income and free cash flow as percentages of revenue) for the year were healthy at 15.9% and 20.6%, respectively.

On capability and innovation

We think Medpace’s management team has an excellent track record in execution and growing the business and there are a number of things we want to discuss.

First, we think August Troendle and his team deserve praise for getting Medpace to (a) target small- and mid-sized biopharma companies and (b) provide excellent service. As we shared in the “Company description” section of this article, 93% of Medpace’s revenue in 2021 came from small- and mid-sized biopharma companies. Based on the earliest data we could find, which goes back to 2015, Medpace has depended on these biopharmas for the lion’s share of its revenue (see Table 4), highlighting that Medpace has long paid significant attention to them.

In contrast, Medpace’s larger competitors have tended to have a weaker focus on smaller biopharma companies. For instance, the percentage of Syneos Health’s total revenue in each year from 2016 to 2021 that came from small- and mid-sized biopharma companies only exceeded 50% in 2021 (see Table 4). In another example, ICON PLC derived less than half of its 2021 revenue from mid and small-sized biopharmas. (The definitions Medpace, Syneos Health, and ICON use to classify the size of their customers are different, but this does not change the essence of the comparison).

Table 4; Source: Medpace and Syneos Health earnings presentations

By targeting smaller biopharma companies, Medpace’s management team has smartly ensured that the company’s attention is on customers who value its services highly. In the “Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market” subsection of this article, we mentioned that smaller biopharmas tend to lack the expertise needed to run Phase I-IV trials well. We also wrote that Medpace was never the lowest bidder for contracts and yet has grown its contract-wins over time, suggesting that the company has been serving its customers well.

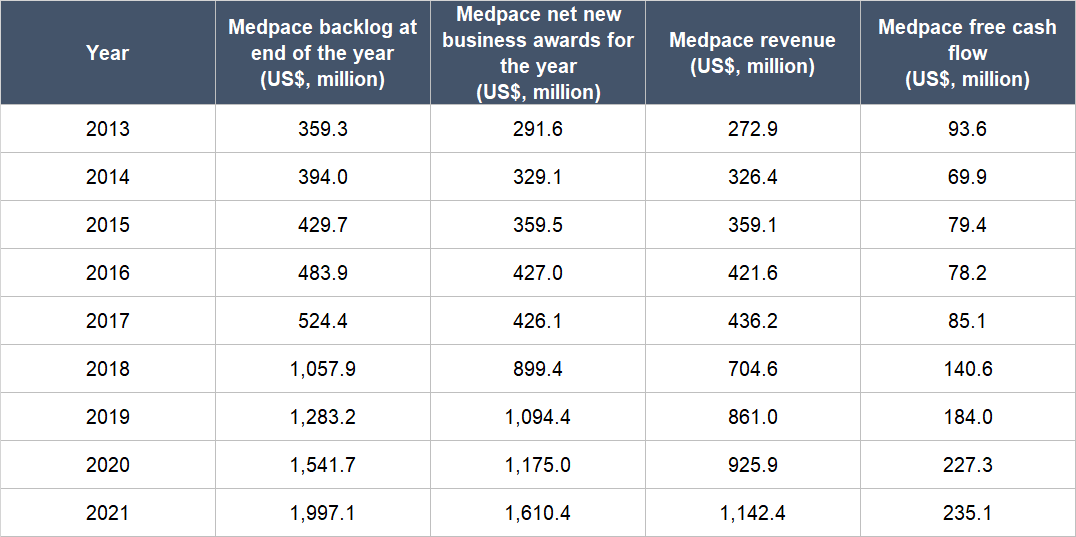

This brings us to the second thing we want to discuss about Medpace’s management team: The company’s strong track record of growing its backlog, net new business awards, revenue, and free cash flow. The backlog is a snapshot in time of Medpace’s anticipated future revenue from net new business awards that have commenced operations but have yet to be completed. Meanwhile, the net new business awards for any given period of time is a cumulative figure showing the anticipated future revenue from new contracts that Medpace has won, net of any contract cancellations. It’s worth noting that before Medpace categorises a new contract within its tallies for backlog and net new business awards, the company would verify a few key aspects of the deal, such as: The possibility that the trial would be cancelled because it has yet to clear regulatory hurdles; whether the biopharma company in question has secured funding for the trial; and the certainty of the trial’s timelines.

From 2013 (the earliest year for data we could find) to 2021, Medpace’s backlog and net new business awards have both more than quintupled, as shown in Table 5. The company’s revenue and free cash flow for those years are also shown and they have quadrupled and more than doubled, respectively. The growth in revenue and free cash flow is noteworthy because most of Medpace’s customers can cancel their contracts with the company for any reason with just 30 days’ notice. Medpace’s ability to grow revenue and free cash flow despite the ease in which customers can tear up contracts is an indication that it’s rare for customers to terminate and it’s another demonstration of the excellent service that the company provides. Another impressive aspect of Medpace’s growth is that it was achieved without any major acquisitions.

Table 5; Source: Medpace annual reports

Third, we want to positively highlight management’s decision to concentrate on being a full-service CRO. Based on what we gathered from the aforementioned expert calls, major pharma companies often have expertise with certain aspects of running drug trials, so they tend to prefer having a CRO perform only parts of a drug trial’s scope of work. This arrangement is known as functional outsourcing and it is something Medpace typically does not engage in.

Instead, Medpace purposefully chooses to collaborate with pharma companies who want to fully outsource the work needed for drug trials. We think this laser-focus has been an important source of Medpace’s growth, as it removes distraction, and also helps to build therapeutic expertise within the company. A CRO’s therapeutic expertise is often a key factor for a pharma company when deciding on a CRO to partner with. There’s another benefit to the focus: It has helped Medpace to secure longer-term partnerships. According to the expert calls, Medpace’s customers that find success with their drug development programmes typically continue their collaboration with Medpace for years. As a reminder, these customers chose Medpace’s full-service offering in the first place because they lack expertise to run clinical trials for their drugs.

Fourth, Medpace’s leaders have built a wide geographical net for its CRO services. This is important because drug trials often have to involve patients from multiple geographies, especially at the later phases. Pharma companies would evaluate a CRO’s geographical coverage as a key factor for awarding a contract, according to the expert calls we’ve reviewed. Medpace currently has more than 4,800 employees spread across 41 countries, up from 2,300 employees across 35 countries at the time of its initial public offering (IPO) in August 2016. Medpace’s presence in a large number of countries provides its customers access to diverse markets, patient populations, and local expertise. The company has not made any major acquisitions throughout its history, as alluded to earlier in this subsection, so the expansion of its geographical reach has happened largely organically too.

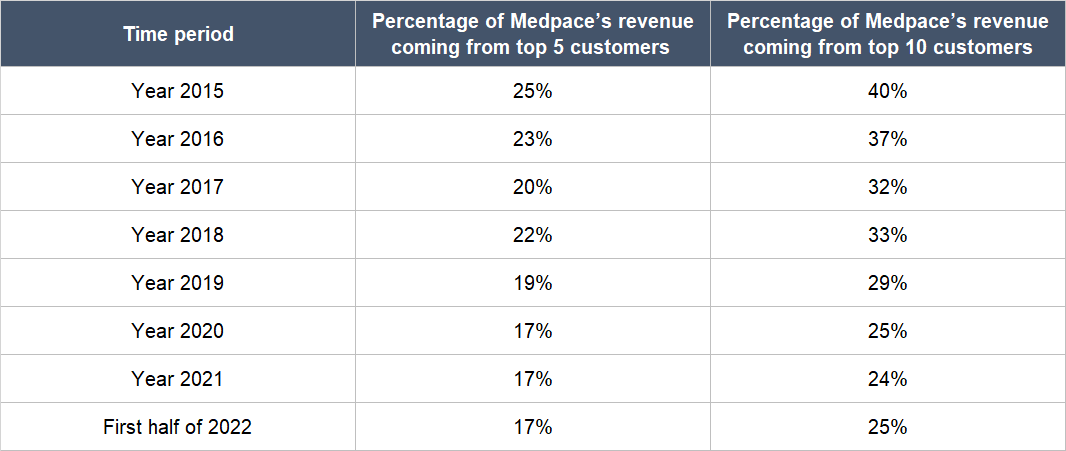

Fifth, we think Troendle and his team have done an admirable job in reducing business risk at Medpace. Table 6 below shows the gradual decline in Medpace’s level of customer concentration from 2015 to the first half of 2022. The fall is important from a risk-management perspective because Medpace’s customers were – and still are – mostly small, pre-revenue biopharmas (we first discussed this trait about Medpace’s customer base in the “Company description” section of this article). Lower customer concentration for Medpace would mean less exposure to the risk of any one customer going bust or running out of capital in the middle of a trial.

Table 6; Source: Medpace annual reports and quarterly earnings presentation

The sixth thing about Medpace’s management team that we want to discuss is not something positive, and it is our observation that there are mixed signals about the quality of the company’s culture. On the negative end, only 60% of Medpace raters on Glassdoor would recommend a friend to work at the company and Troendle only has an approval rating of 50% as CEO, which is far below the average Glassdoor CEO rating of 73% in 2021. Glassdoor is a platform that allows employees to rate their companies anonymously. On the optimistic end, Medpace has a history of promoting from within, as we first mentioned earlier in this subsection. Moreover, the expert calls we’ve reviewed have also highlighted the culture of operational excellence that Troendle has helped foster. Medpace has managed to post impressive business results so far (which we will cover in the “A proven ability to grow” subsection of this article), so we think the company’s culture tilts slightly toward the positive side on the weighing scale. But we’re keeping an eye on things here.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

We see Medpace enjoying recurring revenue in a few ways:

- Drugmakers enter into contracts with Medpace that range from a few months to several years (first mentioned in the “Company description” section of this article). The contracts provide Medpace with recurring revenue if they’re not terminated. It’s unlikely that Medpace’s customers have frequently cancelled their contracts with the company in the past (first mentioned in the “A management team with integrity, capability, and an innovative mindset” subsection of this article), so this positive aspect of Medpace’s business could continue in the future.

- Pharma companies that successfully developed drugs with Medpace’s help typically continue working with the company for new drugs (first mentioned in the “A management team with integrity, capability, and an innovative mindset” subsection of this article).

- In our view, it’s a high probability event that drug-development activity, especially in the realm of biologics, would (a) continue taking place for a long time, and (b) be even more vibrant in the years ahead. Each new biologic that a pharma company wants to develop is an opportunity for Medpace to win new business.

5. A proven ability to grow

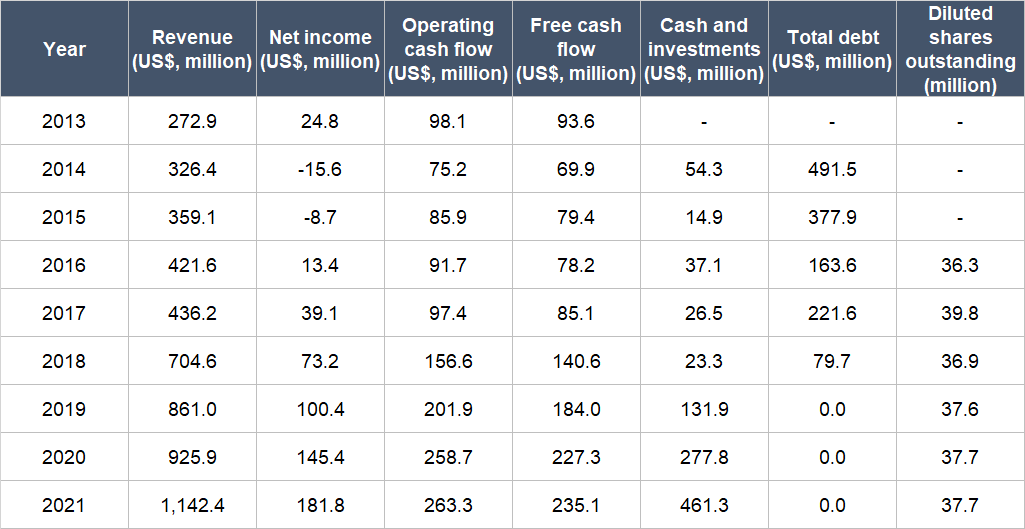

Table 7 below shows Medpace’s key financial figures from 2013 (the earliest data we could find) to 2021:

Table 7; Source: Medpace IPO prospectus and annual reports

A few important things to highlight from Medpace’s historical financials:

- Net revenue grew in each year for the entire time period and had compounded at a respectable annual rate of 19.6%. Growth in 2021 did not slow down – and in fact, accelerated – coming in at 23.4%.

- Medpace’s net income grew by 28.3% per year from 2013 to 2021, and in 2021, the growth rate was still outstanding at 25.1%. For the entire time period we’re looking at, Medpace’s net profit margin also increased from 9.1% in 2013 to 15.9% in 2021.

- The company’s net income picture looked messy from 2014 to 2016, as net income was either negative or the margin was really low. The reason for this is explained at the end of this subsection.

- From 2013 to 2021, Medpace’s operating cash flow and free cash flow both compounded at healthy annual rates of 13.1% and 12.2%, respectively. Moreover, both metrics were positive throughout the time frame we’re looking at and the free cash flow margin was robust throughout, averaging at 22.5% and coming in between 18.5% and 34.3%. The growth of Medpace’s operating cash flow and free cash flow in 2021 was weak at just 1.8% and 3.4%, respectively. But we’re not concerned as the free cash flow margin was still healthy at 20.6% and, as we’ll show soon, the company’s free cash flow resumed double-digit percentage growth in the first half of 2022.

- Medpace’s balance sheet started off weak in 2014 with a high net-debt position. But the situation improved rapidly each year and by the end of 2021, Medpace was sporting a rock-solid balance sheet with US$461.3 million in cash and zero debt.

- Dilution has not been a problem at Medpace as its weighted average diluted share count had barely budged from 2016 (the year of its IPO) to 2021, increasing by a mere 0.7% annually.

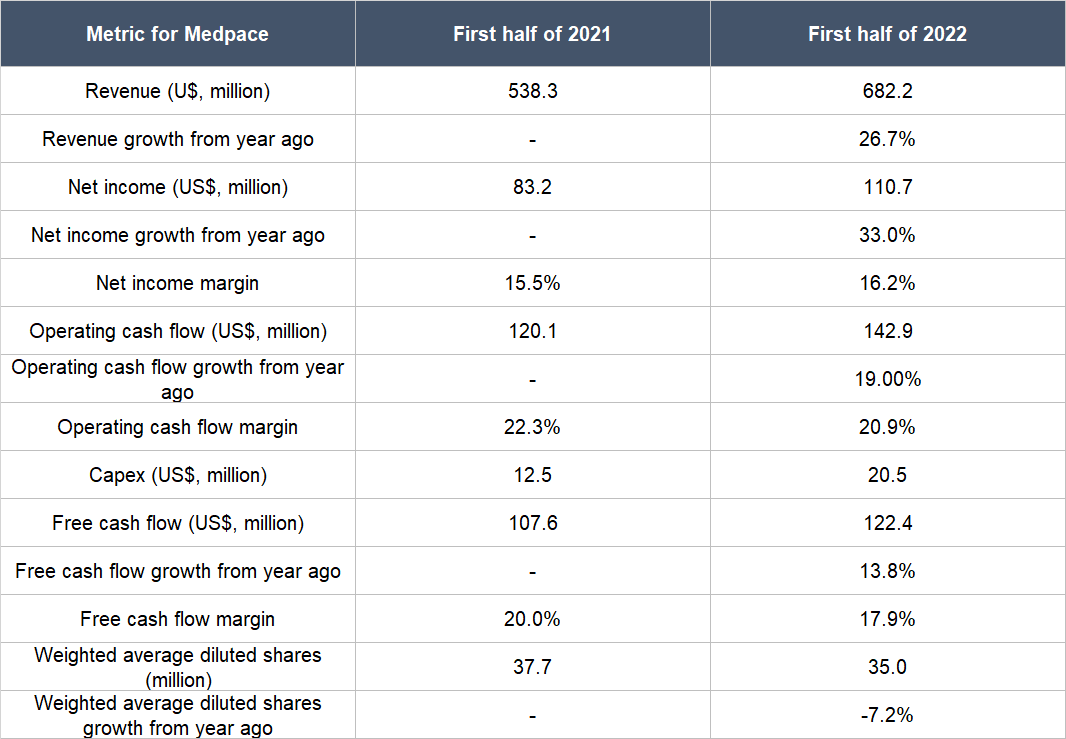

Medpace has continued to post good revenue growth in the first half of 2022, as illustrated in Table 8 below. The table also shows a few more things: (a) Medpace’s net income, operating cash flow, and free cash flow all grew by healthy double-digit percentages; (b) the net income margin improved; (c) the operating cash flow margin and free cash flow margin were both still at robust levels despite declining from a year ago; and (d) Medpace’s weighted average diluted share count fell appreciably, an event that was first alluded to in the “A strong balance sheet with minimal or a reasonable amount of debt” subsection of this article. And as a reminder, we also mentioned in the same subsection that although Medpace’s balance sheet had weakened significantly from the end of 2021 to the first half of 2022, we’re not concerned.

Table 8; Source: Medpace quarterly earnings updates

The reason for Medpace’s net income looking bad from 2014 to 2016 can be traced to its acquisition by a private equity investment firm, Cinven, in April 2014. As part of the acquisition, US$275 million in intangible assets were identified and some of these assets had to be amortised by Medpace in only a few years. Table 9 shows Medpace’s annual amortisation expense from 2013 to 2021 and there was a significant jump in the expense in the 2014-2016 period, which affected Medpace’s net incomes for the period. In our opinion, Medpace’s amortisation expenses that are related to the acquisition by Cinven are an accounting necessity. So the negative or low net income posted by Medpace for the affected years is not an indication of any severe downturn back then in the economic characteristics of the company’s business.

Table 9; Medpace IPO prospectus and annual reports

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

There are two reasons why we think Medpace excels in this criterion:

- First, the company already has a multi-year track record of producing strong free cash flow and robust free cash flow margins, as we discussed in the subsection above. Moreover, in the 15 years prior to Medpace’s IPO in August 2016, the company had maintained impressive average adjusted EBITDA (earnings before interest, taxes, depreciation, amortisation) margins of 34%; the adjusted EBITDA margin can be loosely associated with the free cash flow margin.

- Second, we think there’s plenty of room for Medpace to grow in the CRO market. The company has low market share at the moment and its full-service offering is valuable for the customers it’s targeting, the smaller biopharmas. Moreover, we think the CRO market is likely to expand in the future, which gives Medpace even more potential contracts to win. These factors should lead to higher revenue for Medpace over time. If the free cash flow margin stays healthy, that will mean even more free cash flow for Medpace in the future.

Valuation

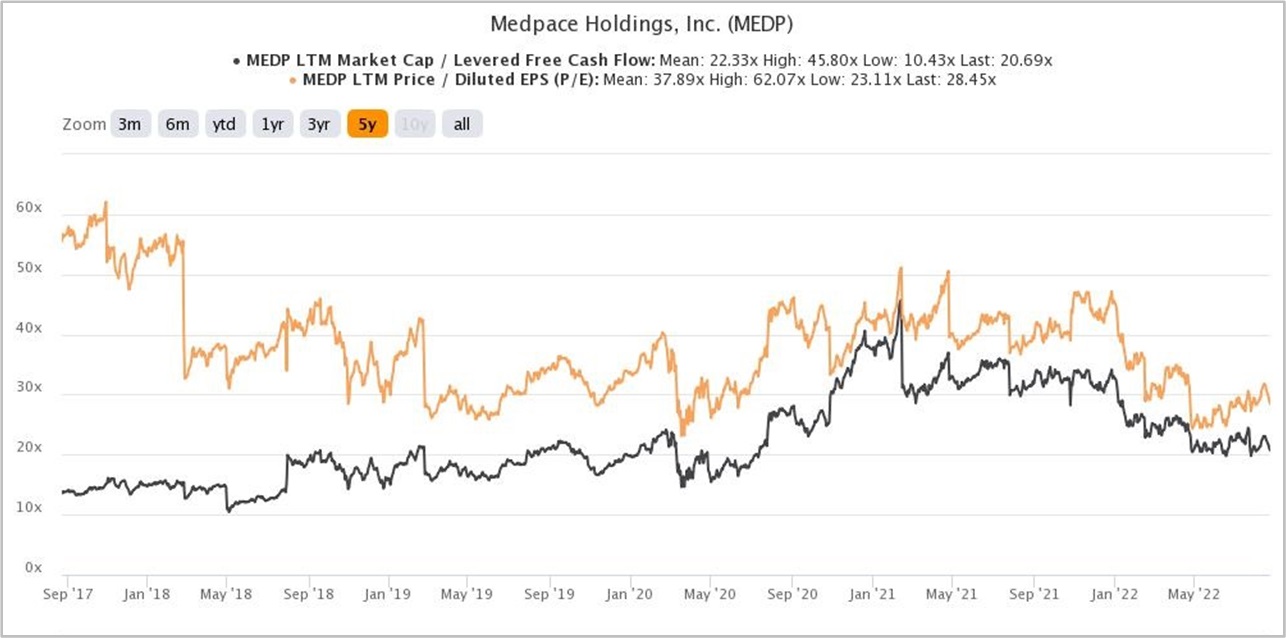

We like to keep things simple in the valuation process. In Medpace’s case, we think the price-to-earnings (P/E) ratio and price-to-free cash flow (P/FCF) ratio are suitable gauges for the company’s value. This is because the company has been adept at producing positive and growing profit as well as free cash flow since its IPO in August 2016.

We completed our initial purchases of Medpace shares around the middle of August 2022. Our average purchase price was US$180 per share. At our average price and on the day we completed our purchases, Medpace’s shares had trailing P/E and P/FCF ratios of around 31 and 26, respectively. We don’t think these ratios are high when compared to the company’s growth prospects and past accomplishments. These ratios are also not high relative to their histories. Here’s a chart showing Medpace’s P/E and P/FCF ratios over the five years ended 22 August 2022:

Figure 5; Source: TIKR

For perspective, Medpace carried P/E and P/FCF ratios of around 27 and 22, respectively, at the 29 August 2022 share price of US$155.

The risks involved

There are five key risks we’re watching that could cause the health of Medpace’s business to deteriorate.

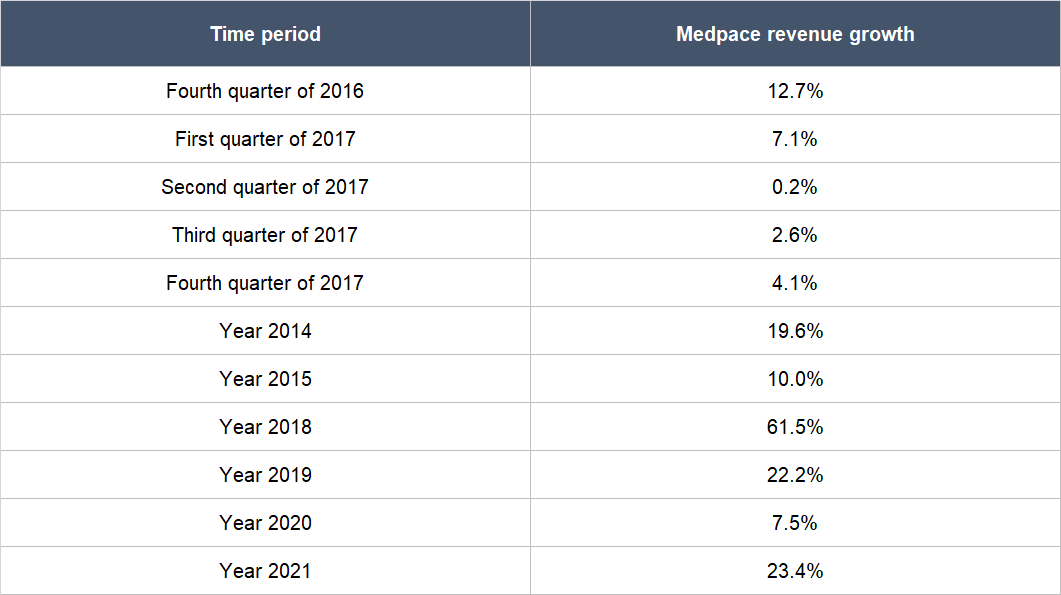

The first is the availability of funding in the biotechnology space. We first mentioned in the “Company description” section of this article that most of Medpace’s customers are small, pre-revenue biopharma companies. These are companies that depend solely on capital provided by investors and/or lenders to run their drug development programs. As such, the ability and willingness of these biopharma companies to undertake new – and continue ongoing – drug trials rests on the availability of funding. In the fourth quarter of 2016 and the first quarter of 2017, there were funding difficulties in the biotechnology space. As a result, Medpace’s revenue growth rates around these time periods were materially lower compared to most other time periods, as shown in Table 10.

Table 10; Source: Medpace quarterly earnings updates and annual reports

During Medpace’s earnings conference calls for the first-half of 2022, management warned that there was softness in the biotech funding environment. The weakness did not stop Medpace from producing 26.7% revenue growth in the first half of 2022 – as we discussed in the “A proven ability to grow” subsection of this article – and from guiding for revenue growth of at least 23% for the whole of the year. But we’re keeping an eye on things here.

Ultimately, we think it’s sensible to expect the financial market’s appetite for funding biotech companies to wax and wane over time. And when conditions are lean in the future, Medpace’s growth could be affected. But we would not be overly concerned if any future weakness in the biotech funding environment is temporary. Where we will be worried is if there’s a long winter for biotech funding, since it could cause the growth of Medpace’s business to flatline for a long time.

The second risk involves Medpace’s CEO and founder, August Troendle. We see him as the architect of Medpace’s growth over the years, so there’s key-man risk. Even when Medpace was owned by Cinven and CCMP, he was still at the helm (CCMP is a private equity firm that acquired Medpace in 2011 and subsequently sold the company to Cinven in 2014). But Troendle may not have much gas left in the tank to serve Medpace, since he’s already 65 this year. If he should step away from Medpace, we’ll be watching the leadership transition. The good thing is that Medpace appears to have a succession plan in place by promoting the 47-year-old Jesse Geiger to the role of President in August 2021.

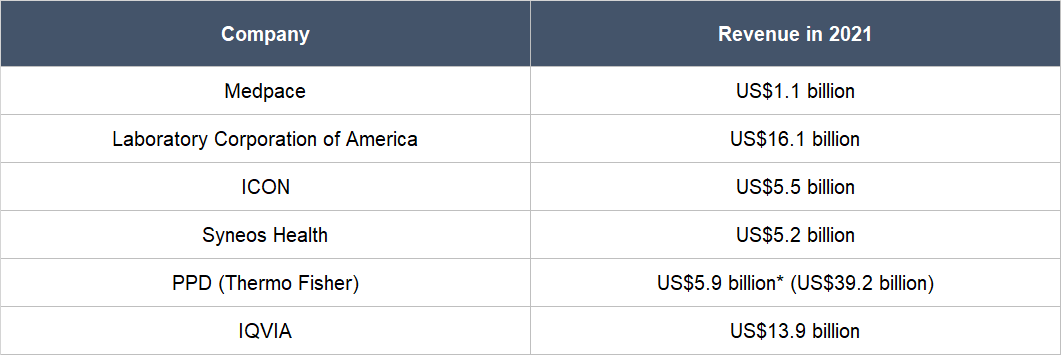

Thirdly, we see a key risk that relates to competition. The CRO industry is fragmented, with hundreds of companies within. But there are also large firms in the space that have significantly more financial resources than Medpace. In the company’s 2021 annual report, it name-dropped five publicly-listed competitors, all of whom have revenues for the year that are multiples of what Medpace earned, as Table 11 highlights. These competitors are Laboratory Corporation of America, ICON, Syneos Health, PPD (recently acquired by Thermo Fisher), and IQVIA. Medpace has so far excelled against its competitors, but there’s no guarantee that it will continue to win.

Table 11; Source: TIKR and Medpace annual report

*PPD’s revenue is for the 12 months ended 30 September 2021

The fourth risk we’re keeping an eye on concerns the regulatory environment. The development of drugs is unsurprisingly a highly regulated activity in the USA and other countries, since the lives and health of people are at stake. If Medpace were to botch any drug trial it’s managing for a customer, the resultant reputational damage could cause irreparable harm to the company’s future growth prospects, since a pharma company would probably think thrice about outsourcing drug trials to a CRO with a spotty history.

Lastly, there’s the risk that involves acquisitions in the biotechnology industry. Smaller biopharma companies who are successful in Phase I or II trials with their drugs could at times be acquired by larger pharma companies. Even smaller biopharma companies with drugs that are successfully commercialised could also be acquired by larger peers. If these events happen to Medpace’s customers en masse, Medpace could lose the opportunity for long-term partnerships with them, thus stunting the company’s growth prospects.

Summary and allocation commentary

To sum up Medpace, it’s a company:

- That is operating in the large and growing CRO market, and that is providing services that are highly valuable to its core group of small biopharma customers

- With a weak balance sheet with more debt than cash, but it’s not a worry for us because the company has a long history of generating substantial free cash flow

- With an excellent leader in August Troendle, who has demonstrated integrity and an excellent long-term track record of execution and unique thinking

- With high levels of recurring revenues because of customer loyalty and the dynamics of drug-development activity in the biologics space

- That has produced a multi-year track record of double-digit percentage growth in revenue, net income, operating cash flow, and free cash flow, as well as robust free cash flow margins

- With a high likelihood of producing a growing stream of free cash flow in the future

There’s one more trait we appreciate about Medpace that we’ve yet to discuss: We see the company as a picks-and-shovels entity to ride on the potential growth of the biologics market. It’s worth noting that small pharma companies have increasingly been the driving innovative force in the pharma industry – they accounted for 63% of all new prescription drug approvals in the USA in the five years prior to 2020. As a reminder, Medpace’s core customers are small- to mid-sized biopharmas. There were over 5,400 pharma companies with active drug-development pipelines as of January 2022, according to Pharmaprojects’ Pharma R&D Annual Review 2022 report. Given this, and the fact that only 24% of Medpace’s total revenue in 2021 came from its top 10 customers, we think it’s safe to assume that the company’s customer-count is in the hundreds. Medpace thus already covers a good amount of surface area, but we think it is likely to increase over time as the company grows.

There are risks to note with Medpace, such as changes in the biotech funding environment; key-man risk; a highly competitive landscape in the CRO market; the possibility of a crippling loss of reputation if the company messes up a drug trial; and the chance of losing long-term customers if they get acquired.

After considering the pros and cons, we decided to initiate a position of around 1.2% in Medpace. We appreciate all the strengths we see in Medpace’s business, but our enthusiasm is currently tempered by the fact that the company is relatively new to us. We’d like to spend more time observing Medpace’s progress before deciding if it warrants a higher weight within the portfolio.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the other companies mentioned in this article, Compounder Fund also owns shares in Alphabet. Holdings are subject to change at any time