Compounder Fund: Twilio Investment Thesis - 07 Nov 2020

Data as of 5 November 2020

Twilio (NYSE: TWLO) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Based and listed in the USA, Twilio provides APIs that act as building blocks for developers to build communication capabilities – in the form of voice, messaging, video, and email – within their organisations’ software applications. APIs stand for application programming interfaces, and they are essentially software code that can be easily integrated with other software.

Twilio’s APIs save developers a significant amount of time and effort. Developers can use Twilio’s software to easily embed communication capabilities into their own apps instead of having to develop them from scratch. Here are some examples of what Twilio’s software can help its customers achieve:

- Allow drivers and riders of ride-hailing services, and users of online dating services, to communicate directly without having to reveal their private phone numbers.

- Alert diners when a table is ready, travellers when flights are delayed, or consumers when a package is shipped.

- Allow customer support teams to communicate directly with callers through voice, messages, or video.

- Send targeted and highly-contextualised marketing content to consumers in an automated way through messaging and/or email.

- Validate log-ins or transactions through two-factor authentication.

- Allow non-profit organisations to run SMS hotlines to fight human trafficking, emergency volunteer dispatch systems, and appointment reminders for medical visits in developing nations.

Twilio groups its software products under two categories. One category is Channel APIs, where Twilio provides APIs that act as flexible building blocks for developers to build the communication capabilities they require. It consists of the following sub-categories:

- Programmable Voice: Software products that enable developers to build voice communications functions (such as text-to-speech, conferencing, recording, transcriptions, and the ability to make and receive phone calls globally) into their applications.

- Programmable Messaging: This set of APIs enable developers to build solutions for users to send and receive messages (the messages can be in localised languages and include emojis and pictures) globally via SMS, WhatsApp, Facebook Messenger, and more.

- Programmable Video: Provides the building blocks to add voice and video to web and mobile applications.

- Email: Enable businesses to engage with customers, for transactional and marketing purposes, via email.

- Super Network: The products in the Channel APIs category are built on top of Twilio’s global software layer that is called the Super Network. The Super Network interfaces with communications networks globally. As of end 2019, Twilio had more than 25 cloud data centers in nine geographically distinct regions as part of the Super Network. These data centers serve as interconnection points between network service providers and Twilio’s users, enabling the users to connect with their customers around the world. The Super Network also helps Twilio’s users to deliver their communications at optimum quality and cost.

The other category of Twilio’s software products is Solutions APIs. This is where Twilio builds on its software in the Channel APIs category to offer software products with more fully-implemented functionality for the most commonly-found use cases and/or most challenging workflows. Solutions APIs has two sub-categories:

- Flex: Flex is a fully programmable cloud contact center platform. With Flex, developers can quickly setup a contact centre that has omnichannel capabilities and customizable elements, including the interface, communication channels, agent routing, and reporting.

- Account Security: This is where Twilio provides two-factor authentication APIs for developers to easily send second-factor passwords to users via SMS, voice, email, or push notifications.

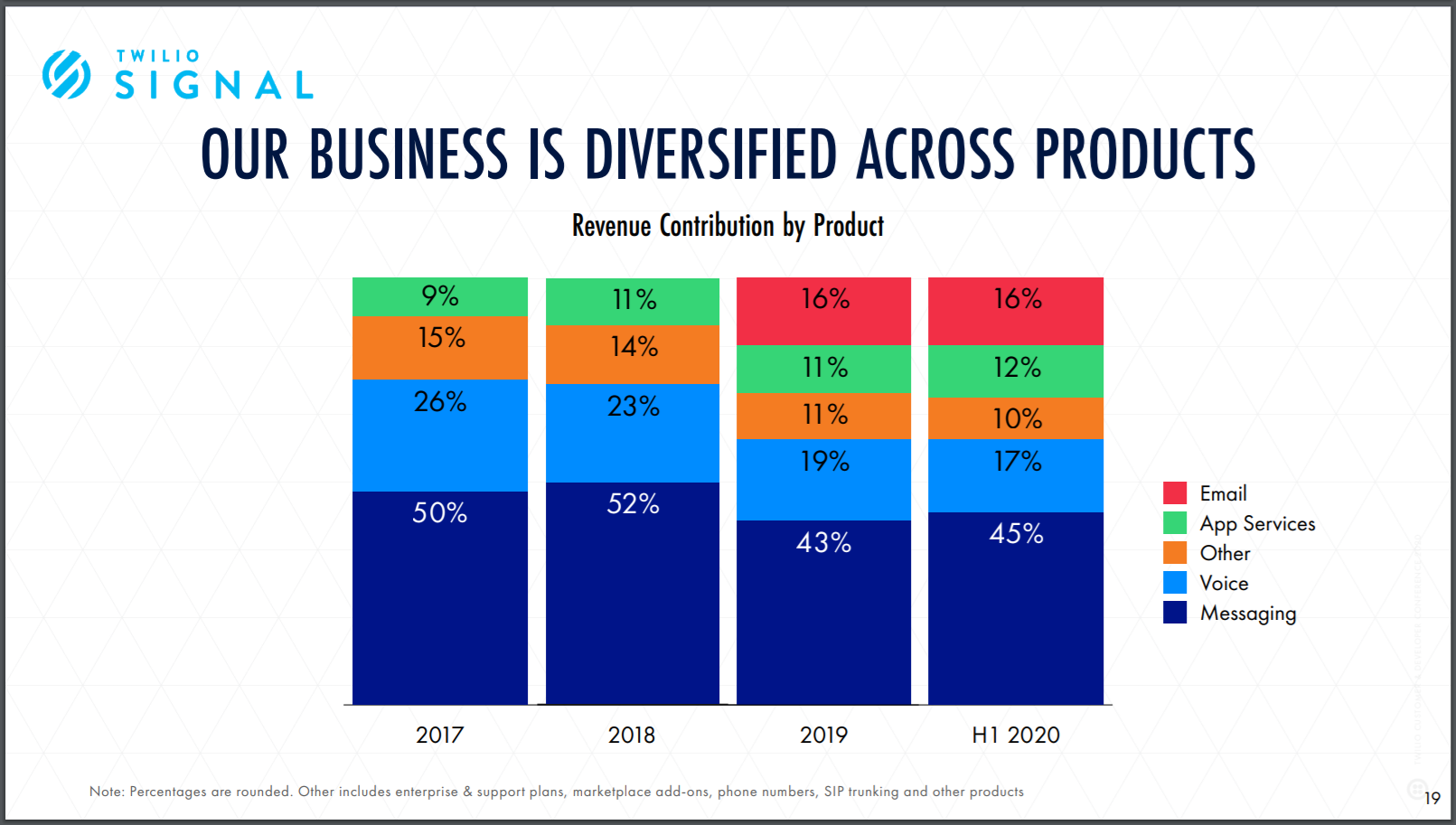

The chart below shows Twilio’s revenue, broken down by products, from 2017 to the first half of 2020. Messaging and Voice APIs are currently the most important products for Twilio; in the first half of this year, the two product sub-categories accounted for 62% of the company’s total revenue. (In the chart, App Services include products from the Solution APIs category, the Video sub-category from Channel APIs, and more.)

Source: Twilio 2020 Investor Day presentation

From a geographical perspective, Twilio’s business is concentrated in the USA. The company pulled in revenue of US$1.21 billion in the first nine months of 2020 and 73% of it was derived from customers with US IP addresses. The remaining 27% of Twilio’s revenue came from other countries across the world.

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Twilio.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

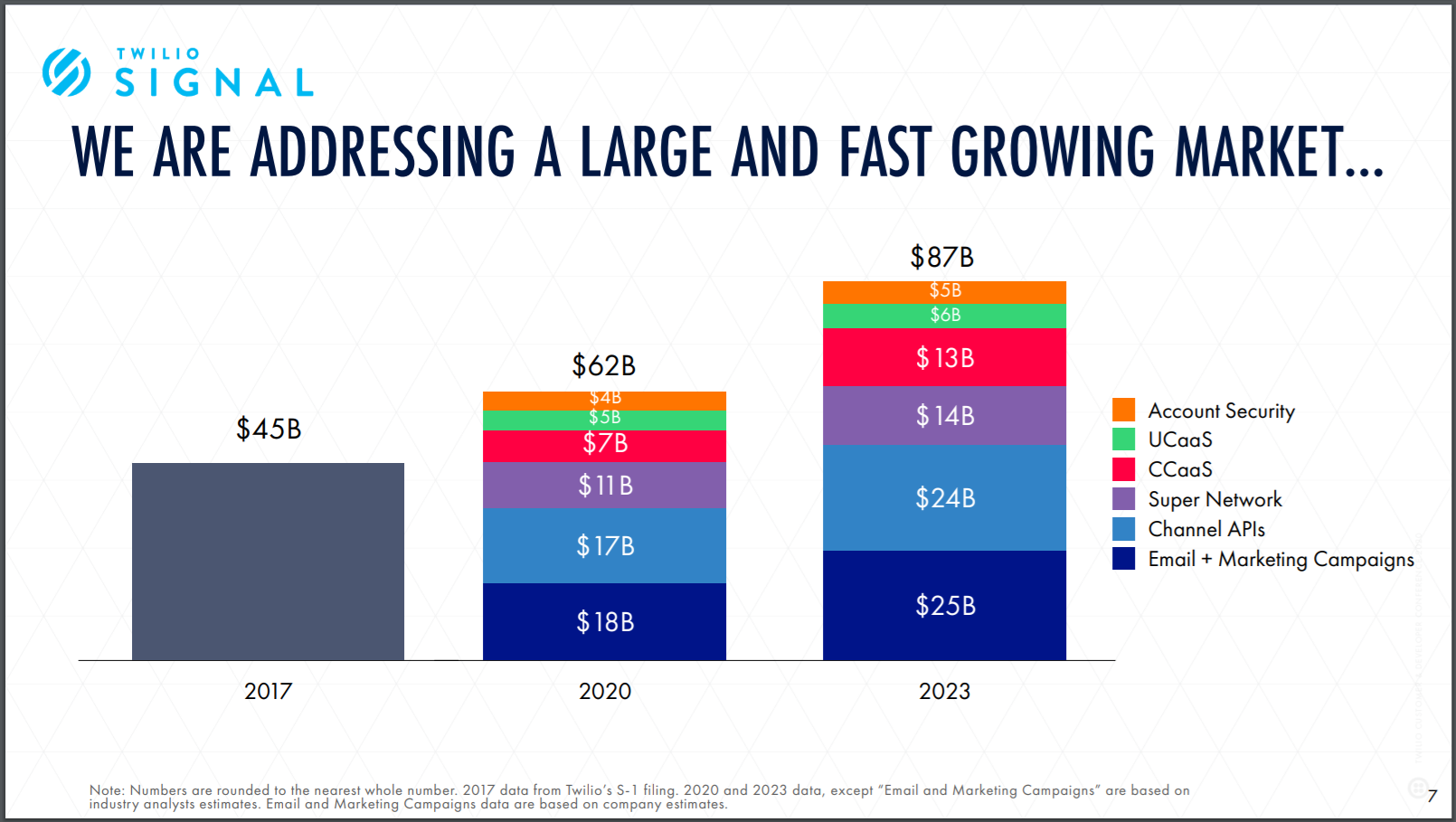

Twilio’s addressable market is large compared to the company’s revenue. More importantly, we believe that the addressable market is growing. The chart below is from Twilio’s Investor Day event held last month and it shows the evolution of the company’s addressable market from 2017 to 2023.

Source: Twilio 2020 Investor Day presentation

Back in 2017, Twilio was tackling a communications market that was worth US$45 billion, according to data from market researcher IDC that was cited in Twilio’s initial public offering (IPO) prospectus. This year, the company thinks its addressable market would have grown by more than 11% per year to reach US$62 billion, based on data by industry analysts. By 2023, Twilio thinks its market would increase by a further 12% annually to hit US$87 billion. For perspective, Twiilio’s revenue in the 12 months ended 30 September 2020 was just US$1.54 billion. These numbers mean that the company has barely scratched the surface of its potential.

We also think that Twilio’s market opportunity is likely to continue growing in the future for a few reasons. First, the ability to have personalised communications with customers at scale should become increasingly important for businesses in the years ahead. And as mentioned earlier, Twilio’s software products allow developers to easily incorporate many different kinds of communication capabilities into their own software applications. Second, Twilio is a highly innovative company (more on the innovation later), which means the company will likely introduce new products in the future that can address new use cases. Third, as already mentioned, Twilio’s APIs function as building blocks for the company’s customers to build communication capabilities. In our view, this trait of Twilio’s APIs could unleash the creativity of the company’s customers, leading them to invent new use cases for Twilio’s existing products.

2. A strong balance sheet with minimal or a reasonable amount of debt

Twilio has a robust balance sheet. The company exited the third quarter of 2020 with US$1.13 billion in cash and cash equivalents, and US$2.17 billion in short-term marketable securities. Meanwhile, total debt was just US$432.7 million (all in convertible senior notes).

For the sake of conservatism, we also note that Twilio had a total of US$229.2 million in operating and finance lease liabilities. But Twilio’s short-term investments and cash and cash equivalents still significantly outweigh the sum of its debt and operating and finance lease liabilities (US$661.9 million).

3. A management team with integrity, capability, and an innovative mindset

On integrity

Jeff Lawson, 42, is a co-founder of Twilio. He has been Twilio’s CEO since 2008 (the year of the company’s founding) and has been chairperson since 2015. We appreciate the fact that Lawson already has more than a decade of experience leading Twilio despite being relatively young (in a business sense). The table below shows some of the other important leaders at Twilio. Although none of them have been at Twilio for a long time, we like that they are all relatively young and have years of experience in important leadership roles at other technology companies.

Source: Twilio proxy statement

We think Twilio’s compensation structure demonstrates integrity in its leadership team. A few points we want to highlight:

- In 2019, Lawson’s total compensation was US$12.29 million, which is high. But it looks reasonable when compared to the scale of Twilio’s business. Moreover, 95.5% of Lawson’s total compensation in 2019 came from stock options and restricted stock units that vest over four years.

- Shipchandler did not receive any stock-related awards in 2019 because he was already given significant stock-related awards in 2018 (amounting to US$14.19 million) for joiningTwilio in November of the year. His 2018 stock-related awards have similar traits as Lawson’s in 2019. For 2019, Shipchandler’s total compensation came only from his base salary, which was a modest US$567,000.

- In a similar manner to Lawson, the sheer majority (92.7%) of Hu’s total compensation of US$8.44 million in 2019 was from stock options and restricted stock units that vest over four years.

- Chew’s total compensation for 2019 was a princely sum of US$23.63 million. But this was because he was given stock-related awards for joining Twilio in January of the year. 98.3% of his total compensation in 2019 came from the stock-related awards that again have similar traits as those of Lawson’s that we described earlier.

- So, nearly all of the compensation of Twilio’s key leaders come from stock-related awards with a four-year vesting period. In our view, this means that the interests of Twilio’s management team and shareholders are well-aligned, since their compensation depends on the long-term growth of Twilio’s stock price, which in turn, is tethered to the company’s business performance.

And speaking of alignment of interests, Lawson has significant skin in the game. As of 31 March 2020, he controlled 7.357 million Twilio shares. This is equivalent to a 5.2% stake and makes Lawson the single largest individual shareholder of the company. Based on Twilio’s stock price of US$306 as of 5 November 2020, Lawson’s shares are worth US$2.25 billion.

We want to highlight that nearly 96% of Lawson’s Twilio shares are of the Class B variety. Twilio has two share classes: (1) Class B, which are not traded and hold 10 voting rights per share; and (2) Class A, which are publicly traded and hold just 1 vote per share. As a result, Lawson controlled 28.8% of Twilio’s voting power (as of 31 March 2020) despite holding only 5.2% of Twilio’s total shares. A manager having significant control over the company can potentially be bad for shareholders. This concentration of Twilio’s voting power in the hands of Lawson means that we need to be comfortable with him at the company’s helm. We are.

On capability and ability to innovate

We think Lawson shines on this front and there are a few things we want to discuss.

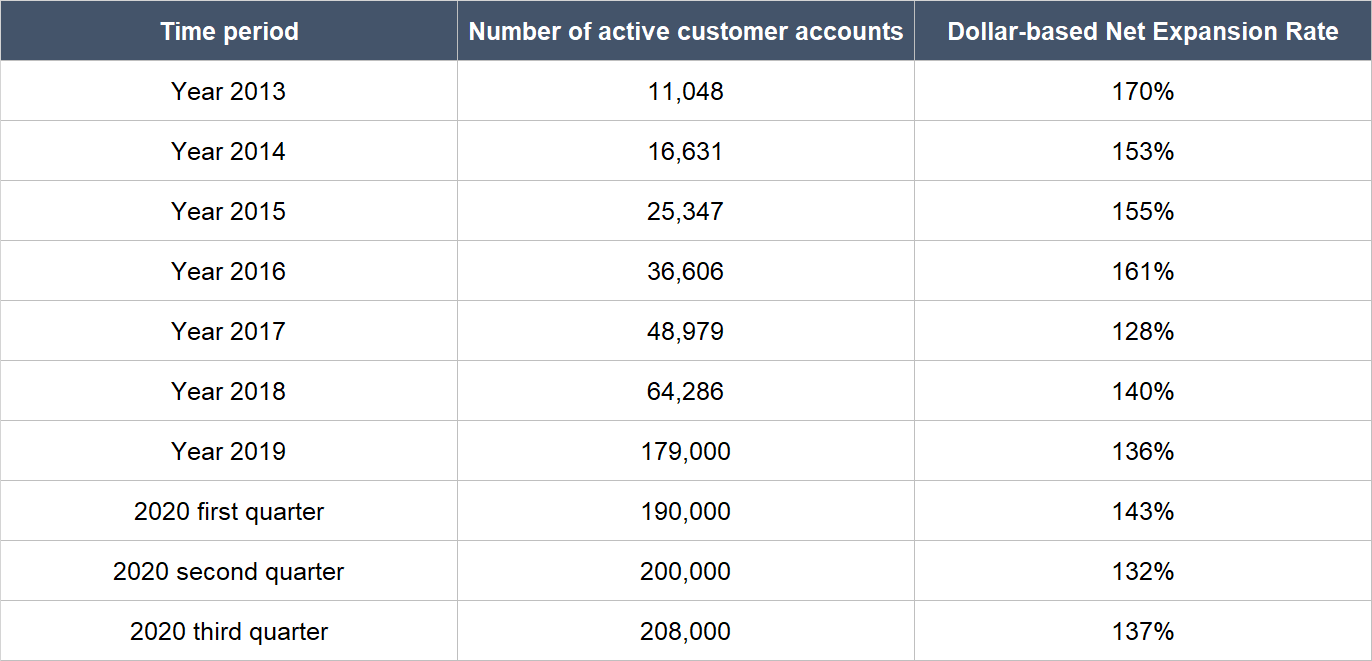

First is Twilio’s excellent track record at winning customers and increasing their spending over time. This can be illustrated through Twilio’s impressive dollar-based net expansion rates (DBNERs) and growth in customer-count. The DBNER metric measures the change in revenue from Twilio’s customers a year ago compared to today; it includes positive effects from upsells as well as negative effects from customers who leave or spend less. Anything more than 100% indicates that Twilio’s customers, as a group, are spending more. From 2013 to the third quarter of 2020, Twilio’s DBNER has never been below 128% and that’s a noteworthy feat. Meanwhile, the company’s customer count has surged from around 11,000 to more than 200,000 over the same period.

Source: Twilio annual reports and quarterly earnings updates

(There was a big jump in Twilio’s customer-count in 2019 because of its acquisition of SendGrid. We will share more about the acquisition later.)

Second, we’re impressed with Lawson’s history as an entrepreneur and employer before his Twilio days. Here’s an excellent recap from a 2016 article written by Miguel Helft for Forbes:

“Soon after, Lawson launched his first Internet startup, Versity.com, which published notes from the biggest courses on campus. As Versity gained traction and pulled in advertising revenue, Lawson dropped out of school, raised money from venture capitalists, moved the company to Silicon Valley and expanded the business to about 200 campuses.

In 2000, as the dot-com wave was cresting, Versity was acquired by a competitor, CollegeClub.com, which had filed for an IPO. Unfortunately, the crash hit before the company could go public, and it collapsed soon after. Since Versity had been acquired for stock, Lawson ended up empty-handed. “No one looked at their burn rate or their cash balance,” he says. “I learned a lot and became very cognizant of spending money wisely.”

Bitten by the entrepreneurial bug, Lawson teamed up with a friend, Jeff Fluhr, who had recently cofounded StubHub. As the company’s first CTO [Chief Technology Officer], Lawson developed the original version of the ticket-reselling site in just six weeks. “He architected the whole thing and recruited a couple of people to help build it,” says Fluhr. But sports wasn’t his thing, and Lawson left the company after a few months, dabbling in a brick-and-mortar retail venture and finishing his college degree.

Hungry for some big-company experience to round out his skills, Lawson interviewed at Amazon in 2004. He got an offer from a tiny team that couldn’t tell him what it was up to until after he accepted. It was the beginning of what would become Amazon Web Services, and Lawson helped build the technology that Amazon launched publicly in 2006. “This whole idea that you can offer infrastructure as a service was kind of mind-blowing,” he says.

His 15 months at Amazon proved to be formative. Selling the building blocks of computing as a service was a brand-new idea, and Lawson was at its epicenter. The model gained traction with the advent of mobile apps, which over time prompted scores of businesses to turn to software as a way to interact with customers. As he began to think about where he could apply the Amazon Web Services model, Lawson homed in on communications, which had proved essential to every business he had started.”

Third, Twilio has a long history with innovation, not just in the introduction of products, but also in its go-to-market strategy and how it introduced itself to the world in its early days. Regarding its go-to-market strategy, Twilio was – and still is – targeting software developers to be the buyers of its software. Twilio’s products are mostly self-serve and come with free trials, and these traits make it easy for developers to give Twilio’s products a spin. Initially, many people could not see the company’s logic for doing so. From the aforementioned Forbes article:

“Many VCs told Lawson that targeting developers, who don’t control budgets of any significance, was a bad strategy. And his timing was lousy: One meeting [during the 2008 financial crisis] with a prominent early-stage firm was interrupted by news of Lehman Bros.’ collapse.”

But Lawson’s insight was prescient, judging by the growth in Twilio’s number of customers over the years. By focusing on developers, Twilio managed to unlock a new set of buyers (the developers) within an enterprise that previously did not exist. Lawson realised that if he could allow developers to easily and cheaply experiment with Twilio’s software, the developers could create a lot of excitement about Twilio within their enterprise, leading Twilio to land the enterprise as a customer and grow from there.

Turning to how Twilio introduced itself to the world in its early days, the Forbes article we referred to earlier has a delightful snippet (notice how clever Twilio’s software demonstration was, and how effective the company’s products were):

“About a year after Lawson and two friends founded Twilio in 2008, Lawson was invited to introduce it at a popular networking mixer called the SF New Tech Meetup. Rather than talk about an inherently difficult-to-explain technology, Lawson decided to let the Twilio software speak for itself.

In front of a thousand people Lawson began telling his story while simultaneously coding a Twilio app – a simple conference line. In just a few minutes he opened an account and secured a phone number, and after writing a handful of lines of code that everyone in the room could understand, his conference line was up and running. Lawson then asked everyone to phone in, and just like that a mob of developers was on a giant conference call. Lawson then added some more code, and his app called everyone back to thank them for participating. As phones throughout the room began buzzing, the crowd went wild with enthusiasm.”

To us, the unique way that Lawson presented the value proposition of Twilio’s products, along with his successful go-to-market strategy that was initially not widely accepted, are wonderful signs that he thinks about the world in a unique way. At Compounder Fund, we like to partner with management teams that have a different way of looking at the world.

Coming to product innovation, the following’s a timeline of the introduction of some of Twilio’s important products:

- Launched Programmable Voice – the company’s first product – in 2008

- Launched Programmable Messaging in 2010

- Launched feature in 2013 that allow Twilio’s customers to exchange messages with their customers that contain pictures and attachments

- Launched two-factor authentication software and Programmable Video in 2015

- Launched Flex in 2018

- Launched email-communications APIs in 2019

We also credit Lawson and his team for the development of the Super Network, the global software layer that underlies all of Twilio’s products. The Super Network analyses the massive communications-traffic flowing through Twilio’s products and intelligently routes the communications of Twilio’s customers across the world, optimising for both quality and cost. There’s a network effect at play here regarding the Super Network. With every new message or voice call that Twilio handles, the Super Network learns and becomes more intelligent and efficient. So, the more Twilio users there are, the better Twilio’s products become for the users. This is a difficult advantage for Twilio’s competitors to break.

Fourth, we think that Lawson has been deploying capital very intelligently. Earlier, we mentioned Twilio’s launch of two-factor authentication software in 2015 and email-communications software in 2019. The genesis for these products were acquisitions, namely, Authy in February 2015 for two-factor authentication, and SendGrid in February 2019 for emails.

Twilio acquired SendGrid for US$2.66 billion and paid for it all in shares (specifically, 23.6 million shares). SendGrid complemented Twilio by giving the latter the capability to provide APIs for email communications to its customers. SendGrid also had a ready base of users that Twilio could cross-sell its existing products to. We mentioned earlier that Twilio experienced a surge in customer-count from around 64,000 in 2018 to 179,000 in 2019 (a jump of 105,000). An important part of the increase was because of SendGrid; it had 74,000 customers as of 30 June 2018. Twilio issued new shares to acquire SendGrid, which resulted in dilution for Twilio’s existing shareholders. But we think it was still smart of Lawson and his team to use Twilio’s shares as currency. This is because the use of shares protected Twilio’s balance sheet (since the company did not have to borrow) and the dilution was not egregious. For perspective, Twilio’s weighted average share count in 2018 was 97.1 million, and the company had a market capitalisation of US$11.1 billion as of 31 January 2019.

And earlier this month, Twilio acquired Segment for around US$3.2 billion, again in an all-stock deal. We think this acquisition makes great sense for Twilio. Yes, the use of shares as currency will mean dilution for Twilio’s shareholders. But Twilio’s market capitalisation on the eve of the deal was US$42.1 billion, which is far higher than Segment’s price-tag – this means that any dilution will be minimal. More importantly, Segment is a software company that helps businesses sort out customer-data in a single platform to get a unified view and better understand their customers. This can improve the customer-communication efforts of businesses and it ties nicely with Twilio’s products, which help companies perform outbound communications. In a recent article for his excellent business newsletter Stratechery, Ben Thompson interviewed Lawson and they talked about Twilio’s reason for acquiring Segment. Here’s Lawson’s explanation:

“But the thing is, to build a relationship really needs two things. First, it needs an understanding of your customer. Who are they? What do they buy? Why are they your customer? What are their preferences? And then the second thing is it takes engagement. Reaching out to the customer, talking to them, having them talk to you. Historically, we had always done the latter. It was like, “Hey customer, you wrote some code. If you want us to send that text message or answer the phone call or send an email, great, we’ll dutifully do that for you.” But we never actually had a part in the, well, why are you reaching out? Who is this customer? What content should you send? When should you send it?

That’s what Segment does, because in a B2C company, understanding your customer is data. And it’s the data that is thrown off from all the myriad systems that you might be using touch your customer. You’ve got e-commerce systems, you’ve got marketing automation systems, you’ve got CRM systems, you’ve got support systems. There are so many different systems… And when we talk to customers about their customer engagement strategy, how are you going to make this a cohesive experience across all these touch points? How are you going to personalize every touch point you have with that customer? We’ve all had those horrible experiences like you go to some websites and you’ve been browsing around for like men’s shirts, you filled out your email and you left and you start getting marketing the next day for like women’s undies and there’s a sale on toddler shoes or whatever…

… We introduced our product, Flex, which is a contact center platform. We introduced it a few years ago, now some of the leading consumer companies have adopted Flex and are using it to build these amazing relationships with their customers. Shopify uses Flex, Lyft uses Flex, at our conference we announced Nike is using Flex and that’s because it enables them to go build. Instead of a monolithic fixed feature solution, like most of the industry has had forever, Flex allows companies to unlock the ideas that they have and they say, “Oh, wouldn’t it be great if, when you’re on the website, we can auto log you in to the chat session” or they say, “Oh, we want to follow it up with a text message or, actually, we’re going to do the whole thing over text.”

So instead of sitting there with the chat window open, or if you walk away from your computer and the agent says, “Hello, hello” and close the session, you’ve got to start all over again. They’re like, “We can stop having these horrible experiences if only we were able to take our ideas and actually build them.” And that’s what Flex allows companies to do in the contact center realm but we envision similar capabilities across many of the touch points. So having this one customer engagement platform where there’s a window for the contact center people and a window for the marketer, and a window for the analysts, and a window for the salespeople, that all coming from one platform is really a new way of thinking about it.

When we look at all the B2C companies out there, they’re all building and they need a new infrastructure that’s not just a bunch of apps stitched together in a very hodgepodge way. They need an architecture and they need something that is designed for building and that’s what we’re focused on.”

Fifth, we’re impressed by how Twilio supported its customers as they transitioned to a shelter-in-place environment because of COVID-19. Here are Lawson’s comments on the matter shared during Twilio’s 2020 first quarter earnings conference call:

“Let me give you just a few use cases across various industries that we’ve helped our customers win over the last couple of months. With shelter-in-place and social distancing going into effect, demand for telehealth solutions has soared. Virtual care became a new reality for doctors, nurses, clinicians and millions of patients around the world. And Epic, the company that supports the comprehensive health records of 250 million people, mobilized to build its own telehealth platform powered by Twilio’s programmable video. The solution allows providers to launch a video visit with a patient, review relevant patient history and update clinical documentation directly within Epic.

Protecting customers and employees from unnecessary in-person contact became a top priority for many businesses, including Comcast. Over the course of just a few weeks, developers at Comcast integrated Twilio Voice into their homegrown customer database, enabling technicians and customer care to contact customers for service requests remotely. They also initiated a pilot to incorporate Twilio Video into the same database, which could enable a customer to use the camera on their phone to show a Comcast technician their setup and the technician can walk them through a self-diagnosis and repair without ever stepping foot in their home.

With widespread school closures, online learning has gone mainstream in a hurry, posing new challenges to keep students engaged and on track with their studies. Blackboard is using Twilio SMS for critical communications to connect patients and teachers and keep students updated. And Schoolclosures.org deployed a distributed contact center on Flex in two days to connect families and teachers during the closures with educational specialists that have experienced teaching from home. Nearly every contact center, especially those on-prem, needed to be reconfigured to support distributed workforces and increased usage.

The City of Pittsburgh needed a way to enable 311 operators to continue to perform their critical work without going to their legacy on-premises call center as usage was spiking in response to COVID-19. They turned to Twilio Flex for a solution. And within four days, we’re up and running with agents working safely from home and no disruption in service for residents.

Non-profits have also had the scale-up to support the unprecedented demand of the current environment. City Harvest provides New Yorkers with emergency food relief in a safe way through Plentiful, an SMS reservation system built in partnership with United Way for New York City and Twilio. And with 62% more clients scheduling appointments and a 474% growth in volume of messages from partners, they are helping more people safely get through during this critical time.”

We think Lawson’s comments just above showcase two really positive traits about Twilio: (1) Its software products work really well and can be deployed very easily and quickly by users; and (2) its management team can execute brilliantly, since Twilio was able to support the rapid-deployment of its software by its customers during a difficult environment.

Sixth, we see strong signs that Lawson and his team have built a great corporate culture at Twilio:

- Glassdoor is a platform that allows employees to rate their companies anonymously. Currently, 79% of Twilio-raters on Glassdoor will recommend the company to a friend. Meanwhile Lawson has a 94% approval rating, far higher than the average Glassdoor CEO rating of 69% in 2019.

- Twilio believes it can create “greater social good through better communications.” To this end, the company owns an organisation known as Twilio.org. Through Twilio.org, Twilio donates or discounts its software to non-profit organisations. Twilio.org’s mission is to “fuel communications that give hope, power, and freedom with a 10-year goal to help one billion people every year.”

- In 2019, Twilio launched WePledge, an internal employee impact program. WePledge encourages Twilions (the endearing term Twilio uses for its employees) to commit 1% of their individual time and/or equity to causes they care about. Under the program, Twilio in turn gives employees 20 hours of paid volunteer time, a US$500 matching gifts budget, and a convenient way for them to donate their company equity through an app.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

In 2019 and in the third quarter of 2020, usage-based fees accounted for 75% and 77%, respectively, of Twilio’s total revenue. Some examples of Twilio’s usage-based fees include minutes of call duration activity for Programmable Voice, number of text messages sent and received for Programmable Messaging, and the number of authentications sent for Account Security. We believe that Twilio’s usage-based fees are recurring because the activities these fees depend on have to be repeated often by Twilio’s customers.

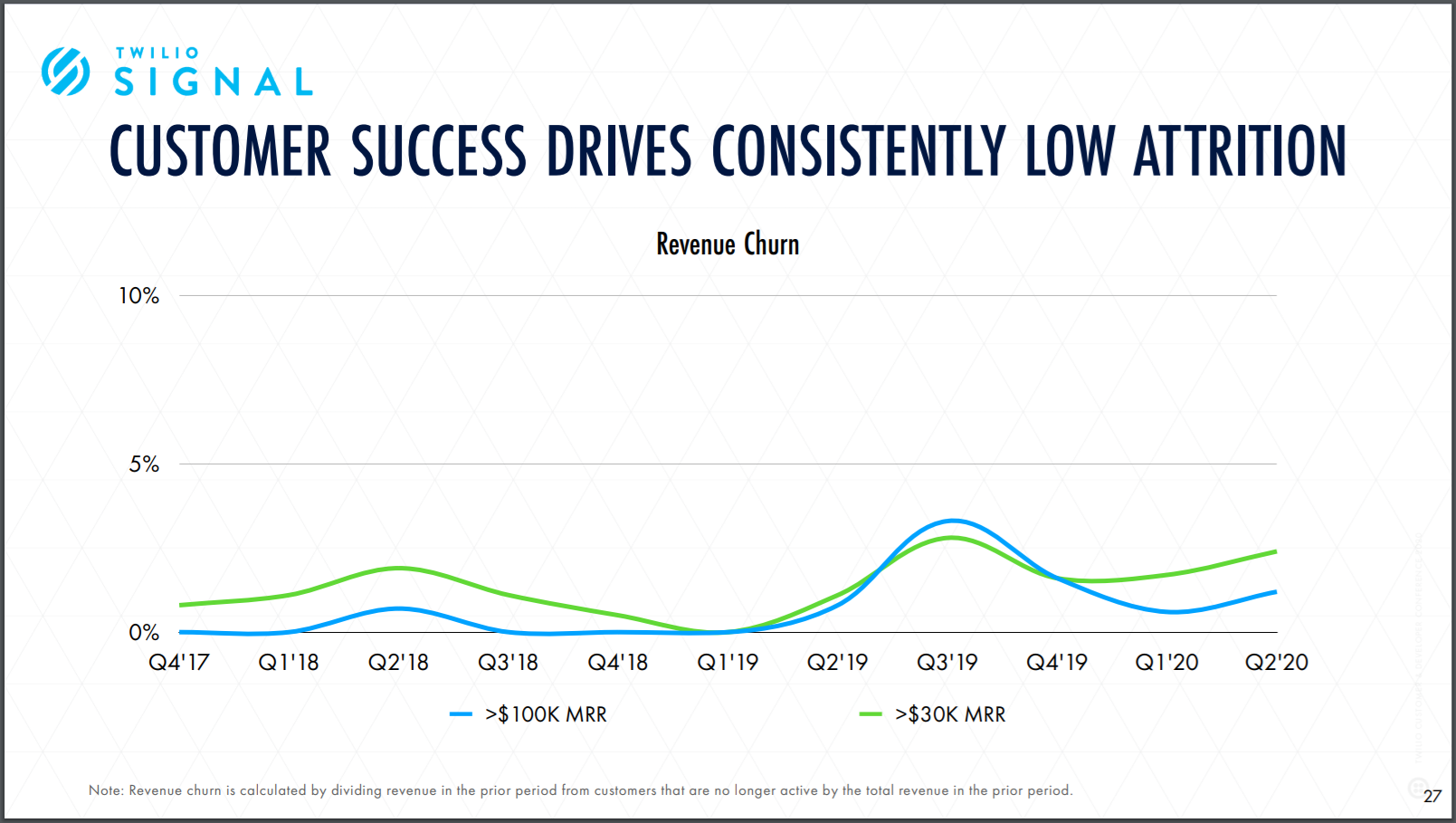

Lending weight to our view that Twilio has a high level of recurring revenue are two things. The first is the fact that Twilio has done a great job at retaining customers and getting them to spend more over time. The chart below shows Twilio’s consistently low revenue churn rate (the rate of customers leaving) of below 5% from the fourth quarter of 2017 to the second quarter of 2020. And as we already mentioned, Twilio’s DBNER has been excellent from 2013 to the third quarter of 2020, coming in at 128% or higher in that period.

Source: Twilio 2020 Investor Day presentation

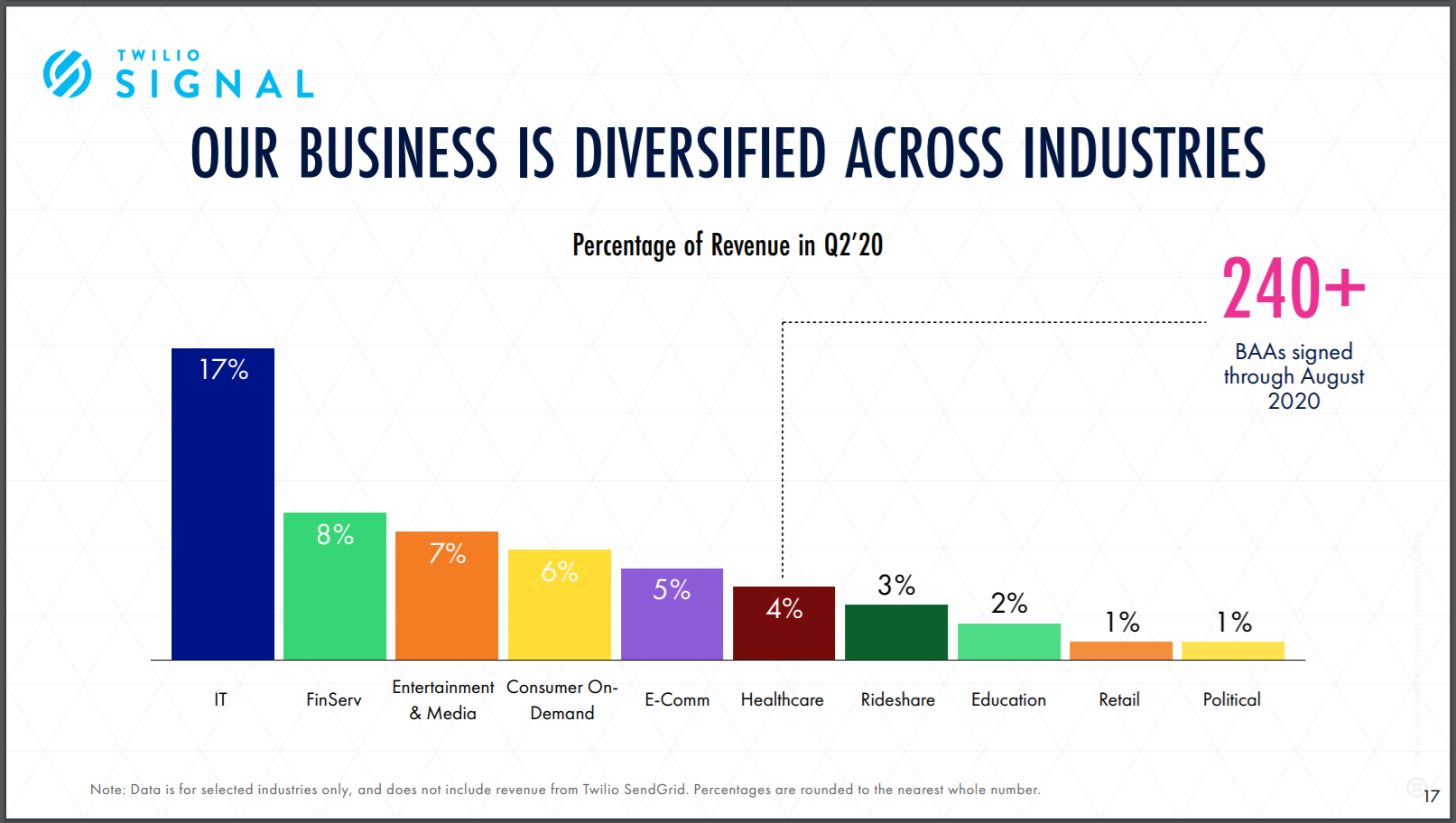

Second is the absence of concentration-risk in Twilio’s business across a few dimensions. The company does not have revenue concentration in terms of:

- The number of customers: No single customer accounted for more than 10% of Twilio’s total revenue in 2019 and the first nine months of 2020.

- Industry exposure: See chart below, which shows a breakdown of Twilio’s revenue in the second quarter of 2020 by industry.

- The size of customers: In the second quarter of 2020, 36% of Twilio’s revenue was from customers who had more than 2,000 employees, 28% was from customers with between 101 and 2,000 employees, and 36% was from customers with 100 employees or less.

Source: Twilio 2020 Investor Day presentation

5. A proven ability to grow

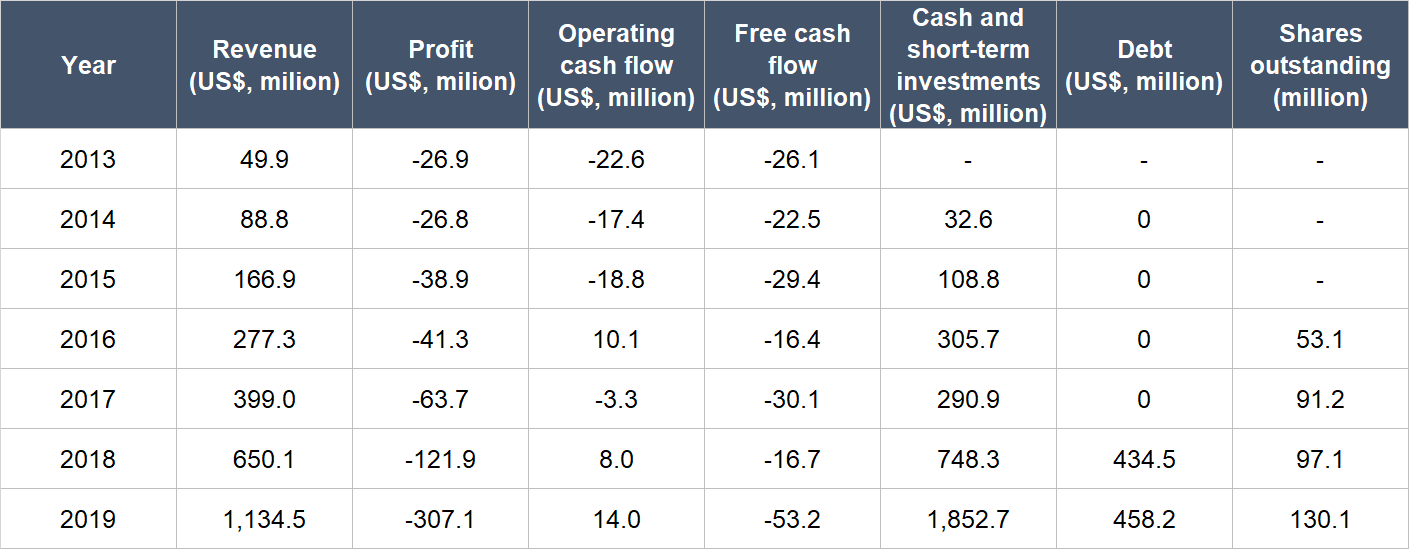

The table below shows Twilio’s key financials since 2013 (they are the earliest data we can find, since the company was listed only in June 2016):

Source: Twilio annual reports and IPO prospectus

Some important things to highlight from Twilio’s historical financials:

- Revenue has compounded at a rapid rate of 68.3% per year from 2013 to 2019, with most of the growth being organic. The reported revenue growth in 2019 was 74.5%. Excluding SendGrid’s contribution, Twilio’s revenue increased by 47% during the year, which is still impressive.

- Twilio has been unable to generate a profit so far, but we’re not worried. The company is incurring high expenses (such as stock-based compensation) in recent years as investments into the business for future growth.

- Starting from 2018, Twilio seemed to begin generating positive operating cash flow consistently. But the company’s free cash flow was negative from 2013 to 2019. We’re also not concerned here, as we think that Twilio’s reinvestments into its business make good sense.

- Twilio’s balance sheet has been really strong for the entire time frame we’re studying. From 2013 to 2019, Twilio’s debt was either zero or low compared to its cash and short-term investments. But we want to point out that Twilio’s cash and short-term investments, net of debt, had increased from US$32.6 million in 2014 to US$1.39 billion in 2019 mainly because of (1) the sale of shares during its IPO and a secondary offering in June 2019 which netted US$970 million, and (2) the use of its own shares as currency when making big acquisitions.

- At first glance, Twilio’s diluted share count appeared to increase significantly by 71.7% from 2016 to 2017 (we only started counting from 2016 since Twilio was listed in the month of June during the year). But the number we’re using is the weighted average diluted share count. Right after Twilio got listed, it had a share count of around 86 million. From 2017 to 2019, Twilio’s weighted average diluted share count increased by 19.4% per year. It’s not a surprise to learn that Twilio has exhibited shareholder-dilution given the aforementioned secondary offering in 2019, the company’s use of stock-based compensation, and its penchant for using shares to pay for big acquisitions. The share count growth of 19.4% annually from 2017 to 2019 is much lower than the company’s revenue growth of 52.4% per year over the same period, so that’s good. But it is still higher than what we typically like to see and we’ll be keeping an eye on future changes in Twilio’s share count. To be clear, we still think it’s sensible for Twilio to take advantage of its rising share price (Twilio’s share price has increased from US$29 on the close of its first trading day to US$306 as of 5 November 2020) by issuing new shares to raise capital, and by paying for smart acquisitions (we like both the SendGrid and Segment deals) with shares.

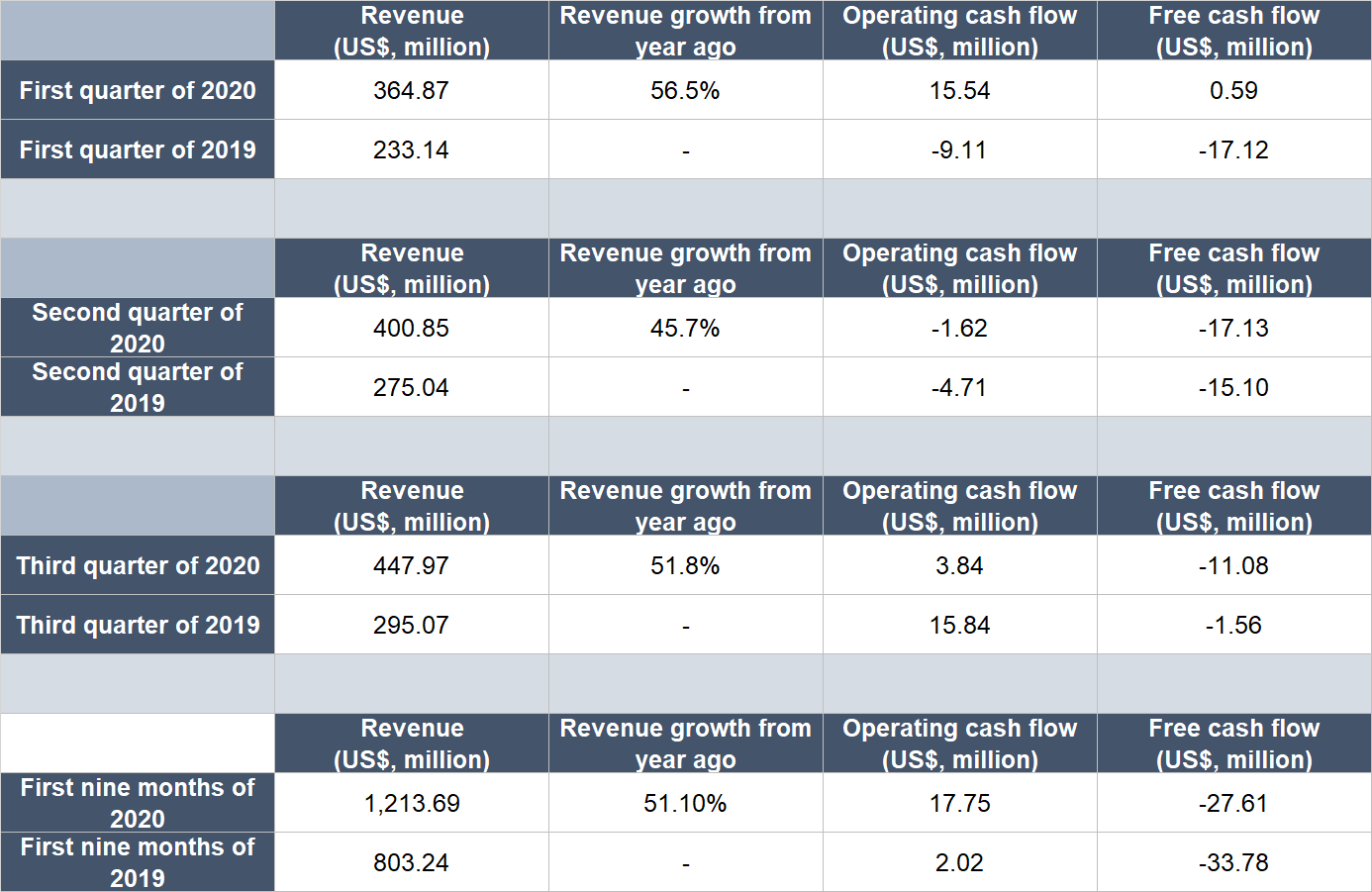

So far in 2020, Twilio has extended its winning streak of blistering revenue growth despite COVID-19 having wreaked havoc in the global economy. The table below shows the year-on-year changes in Twilio’s revenue, operating cash flow, and free cash flow for the first three quarters of this year. Note the improvement in both the company’s operating cash flow and free cash flow in the first nine months of 2020. Over the same period, Twilio’s weighted average diluted share count increased by 12.1% from a year ago; this could be lower, but it still looks good, since the company’s revenue growth was much faster at 51.1%.

Source: Twilio quarterly earnings updates

Twilio’s management is confident in the company’s growth over the medium term. In Twilio’s Investor Day event held in October 2020, management provided an estimation for organic revenue growth of more than 30% per year for the next four years. We think this projection is sensible and could even be understating the company’s actual future growth.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Twilio has not consistently generated positive free cash flow in the past but we think it has the ability to do so in the future.

We believe Twilio has strong economics. This can be seen from the company’s low revenue churn and high dollar-based net expansion rate that we shared earlier, and it should aid the company in producing strong free cash flow eventually. During Twilio’s October 2020 Investor Day event, management shared a target for an operating margin of more than 20% over the long run. Given that Twilio is a software company, we think that an operating margin of more than 20% is easily achievable when it is more mature. And this level of operating margin should also lead to a free cash flow margin (free cash flow as a percentage of revenue) of around 20%.

Valuation

We completed our purchases of Twilio shares with Compounder Fund’s initial capital in late July 2020. Our average purchase price was US$258 per Twilio share. At our average price and on the day we completed our purchases, Twilio shares had a trailing price-to-sales (P/S) ratio of around 28. We like to keep things simple in the valuation process. In Twilio’s case, we think the P/S ratio is an appropriate metric to value the company, since the company does not have a long history yet of generating free cash flow.

There’s no need to consult any historical valuation chart to know that the P/S ratio of 28 is high – and that’s a risk. For perspective, if we assume that Twilio has a 20% free cash flow margin today, then the company would have a price-to-free cash flow ratio of 140 (28 divided by 20%). But we think Twilio is an excellent company that has years of rapid growth ahead of it. This makes us comfortable with paying up for Twilio’s shares, since we think the company has a good chance of being able to grow into its valuation.

For perspective, Twilio also carried a P/S ratio of 28 at the 5 November 2020 share price of US$306.

The risks involved

We see four main risks with Twilio

1. We think Jeff Lawson’s leadership has been a critical reason behind Twilio’s success since its founding 12 years ago in 2008, so there’s key-man risk. If Lawson were to hand over the keys for any reason, we’ll be watching the leadership transition closely. The good thing is that Lawson is still only 42 years old, so he can likely continue leading the company for years to come.

2. We are also mindful of the risk from competition. Twilio operates in a competitive environment that is intensifying. Ride-hailing giant Uber was once a major customer of Twilio, accounting for 14% of total revenue in 2016. But in 2017, Uber decided to move away from Twilio as its key communications platform and adopt a multi-platform approach. Twilio’s growth was not really affected. Twilio revealed the news of its breakup with Uber during its 2017 first quarter earnings update and guided for revenue of between US$85.5 million to US$87.5 million for the second quarter. The midpoint of Twilio’s revenue guidance represented year-on-year growth of 34%. Twilio ended up posting revenue of US$95.9 million for the second quarter of 2017 instead, up 49% from a year ago. And Twilio has continued to produce robust growth numbers since Uber walked away from it. We also think that Twilio has very high-quality software products. Nonetheless, we’re keeping an eye on Twilio’s competition.

3. Dilution is another risk we’re watching. We mentioned earlier that Twilio’s share count has increased at a faster rate than we like to see since it went public in 2016. We think the company has so far been opportunistic in the way it has raised capital through secondary offerings and used its shares as currency for acquisitions – these actions have been a net positive for Twilio’s investors so far, in our view. But we are still mindful of dilution, so we’re paying attention to Twilio’s capital allocation decisions. We also want to see secondary offerings disappear or at least become a rarity for Twilio once the company starts generating substantial free cash flow. (We note that the company had conducted a secondary offering in August 2020 to raise US$1.4 billion by issuing 5.82 million new shares.)

4. Lastly, there’s valuation risk. We can’t ignore that Twilio has a lofty P/S ratio. We believe that Twilio deserves its premium multiple given its bright growth prospects. But if there are any slowdowns in Twilio’s growth – even if they are temporary – there could be a painful fall in its share price. This is a risk we’re comfortable taking on as long-term investors.

Summary and allocation commentary

To summarise Twilio, it has:

- Important software products for communications that save its customers significant time and effort

- A large addressable market that is also likely to grow in the future because of the company’s innovative spirit

- A balance sheet that is flush with cash and has little debt

- An innovative, highly capable, and young CEO in Jeff Lawson

- A well-designed compensation plan for its management team

- A high level of recurring revenue because of repeat-use of its products by customers

- A solid track record of revenue growth

- Good economics in its business that we believe will lead the company to rake in free cash flow in the future

There are important risks we’re watching with Twilio, including key-man risk; growing intensity in the company’s competitive landscape; the risk of shareholder dilution; and the risk of a high valuation.

After weighing the pros and cons, we initiated a 2.0% position – a medium-sized allocation – in Twilio with Compounder Fund’s initial capital. We appreciate all the positives that we see in Twilio, but our enthusiasm is also tempered by the company’s high valuation and the company’s current losses and negative free cash flow.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share. Of all the companies mentioned in this article, Compounder Fund also currently owns shares in Amazon.com, Facebook, and Shopify. Holdings are subject to change at any time.