Compounder Fund: Wix Investment Thesis - 16 Aug 2020

Data as of 12 August 2020

Wix.com (NASDAQ: WIX) is one of the 40 companies in Compounder Fund’s initial portfolio. This article describes our investment thesis for the company.

Company description

Wix is listed in the US, but it is the only company in Compounder Fund’s portfolio that is headquartered in Israel. The company was founded in 2006, with the goal to enable anyone to build a website even if they do not have a technical programming background. Wix’s products enable business owners and organisations to take their businesses, brands, and workflow online to create and manage a fully integrated and dynamic digital presence.

Wix offers its solution through a freemium model, which includes free and premium services. The company’s platform consists of three web creation products that are built for different purposes and primary audiences:

- Wix ADI is the most basic of them and uses artificial intelligence to allow users to create beautiful websites quickly and easily, with no technological background required

- Wix Editor is intended for users who possess basic to above-average technological skills

- Editor X, which is currently in open beta mode, offers the widest range of capabilities and is suited for advanced users

In 2017, Wix launched Wix Code, which was rebranded as Corvid in 2019. Corvid is combined with Wix ADI, Wix Editor, and Editor X, and it is a development environment that allows users to create content rich, custom websites and web applications. Interestingly, Corvid does not require users to code and so it allows them to focus on the creative process.

Wix also offers a variety of other products and services, some of which include:

- Ascend by Wix, which includes a suite of 20 products and features that enable users to take payments, easily connect with customers, manage customer relations, generate more traffic, capture leads, automate their work, grow their business and more.

- Wix Payments, a payment platform that helps Wix’s users receive payments from their users through their Wix website.

- Vertical-specific applications for business owners to run mission-critical functions online, such as selling goods, taking reservations and scheduling and confirming appointments. These applications are integrated into Wix’s website templates or can be installed on any existing website, and they can be set up with only minimal effort by the user (there’s no need to write code). The verticals that are served include retail and online stores, services, event planners and management, hotel and property management, music, photography, restaurants and more.

- App Market, which offers users access to a variety of free and paid web applications that are developed by Wix or third-parties. The web applications in the App Market can be installed with one click without the need for coding.

Here’s a chart showing the range of Wix’s products and services:

Source: Wix investor presentation

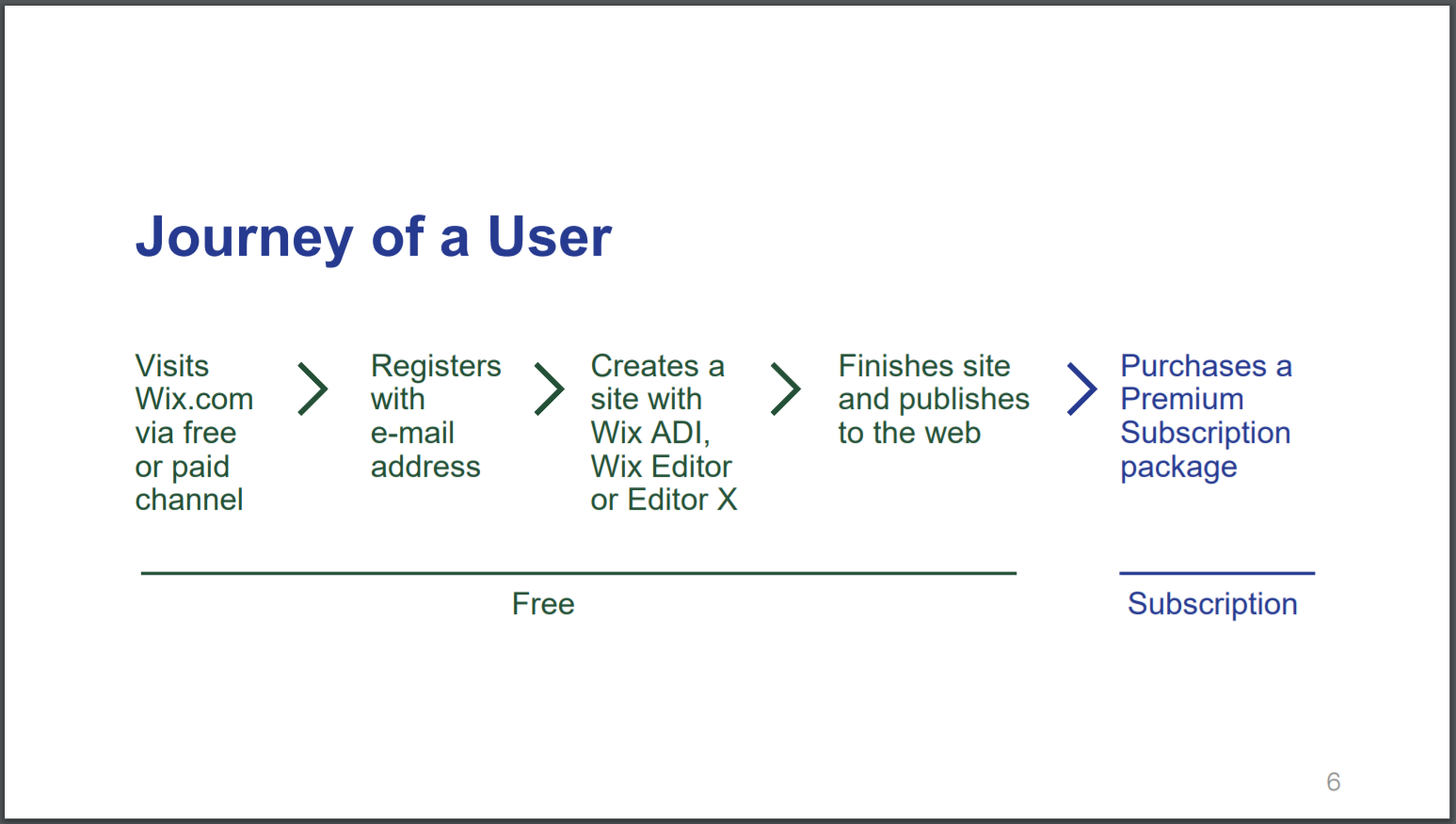

The chart below shows the typical journey of a Wix user. As of 30 June 2020, Wix had 182 million registered users and 5.0 million premium subscriptions.

Source: Wix investor presentation

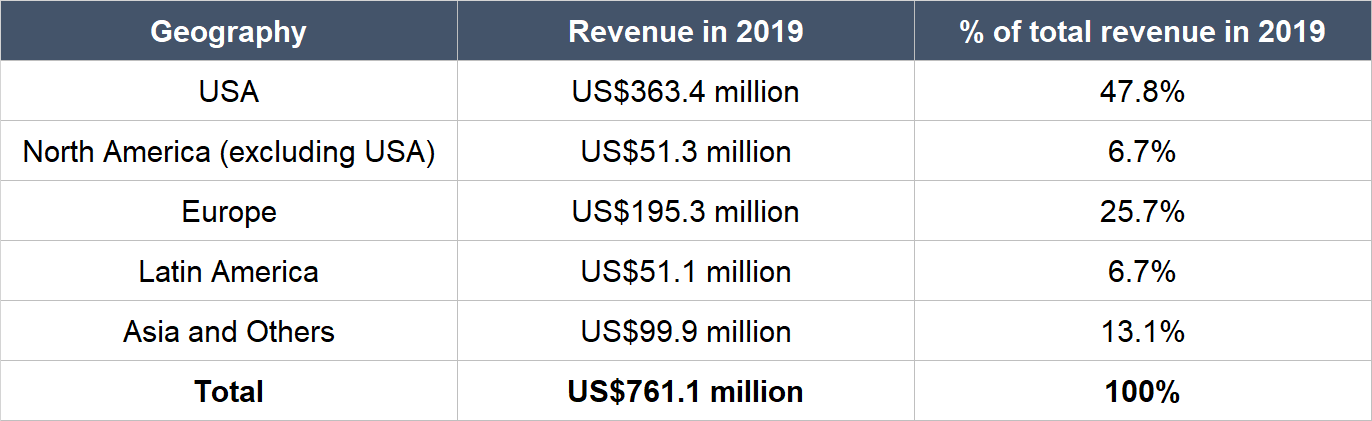

At the end of 2019, Wix offered its platform in 20 languages (although users can create websites in any language) and the company has plans to add more languages in the future. In a reflection of its ability to offer many languages, Wix’s business is also global in nature. The company has users in around 190 countries, and it has a geographically-diverse revenue base as shown in the table below.

Source: Wix annual report

Investment thesis

We have laid out our investment framework in Compounder Fund’s website. We will use the framework to describe our investment thesis for Wix.

1. Revenues that are small in relation to a large and/or growing market, or revenues that are large in a fast-growing market

Wix believes that no company “currently offers a comprehensive, customisable, fully integrated workflow solution to create and manage a professional digital presence comparable” to what it offers, according to its latest annual report. This is great, because Wix’s market for providing web-based website design and management software is large and growing. Here are some data for perspective:

- According to a May 2020 Wix investor presentation, there were around 330 million existing active domains, but only 3.5 million Wix premium sites.

- The percentage of websites that used some form of content management systems (includes platforms from Wix and its peers such as Shopify and WordPress) has swelled from 23.6% in 2011 to 59.8% in August 2020.

- Prior to the introduction of Corvid in 2017, Wix’s estimate of its market opportunity was around US$30 billion. The launch of Corvid increased Wix’s market opportunity by a factor of 10 to more than US$300 billion. Wix estimates its addressable market based on all the services that it provides, which includes website building, vertical-specific products, marketing support, communication support, customer management, mobile websites etc. According to W3techs.com, Wix’s market share in the content management system space has increased from less than 0.1% in January 2013 to 1.5% in August 2020. With Corvid, we believe Wix is well positioned to gain market share by allowing users to create more complex websites.

Wix’s revenue was merely US$853.4 million in the 12 months ended 30 June 2020, which scratches less than 0.3% of the US$300 billion-plus addressable market that the company sees.

We also want to point out that the current COVID-19 pandemic has accelerated the adoption of technology by many companies that want a simple and quick way to move their business online – this is where Wix excels. Here are some comments on the matter that were shared by Wix’s co-founder and CEO, Avishai Abrahami, in the company’s earnings updates for the first and second quarters of 2020:

“[First quarter of 2020]

“The COVID-19 crisis has forced a massive change upon our users. The need for SMBs, entrepreneurs and brands to move online quickly, to communicate with their customers and to deliver goods and services has never been clearer. Demand for our platform offerings boomed at the beginning of April, and I am extremely proud to say that our team responded quickly to make sure we can deliver the best service to our users across the globe.”[Second quarter of 2020]

“The trends that began in late March continued throughout the second quarter, driving record-setting results. The need for business owners to move online quickly, communicate with customers, and deliver goods and services has never been more imminent, and the Wix platform continues to provide millions of users with the ability to thrive during these unprecedented times. Our focus remains on the success of our users, and we continue to deliver innovative products and technology, marked this quarter by the public launch of Editor X and our expanded eCommerce offering.”

2. A strong balance sheet with minimal or a reasonable amount of debt

Wix has a strong balance sheet. As of 30 June 2020, the company had US$903.8 million in cash and equivalents, short-term deposits, and investments, against merely US$359.9 million in debt (consisting of US$358.7 million in convertible notes and US$1.2 million in loans).

Moreover, Wix has been generating free cash flow in the past few years while maintaining strong revenue growth. We will discuss Wix’s financials in greater detail later.

3. A management team with integrity, capability, and an innovative mindset

On integrity

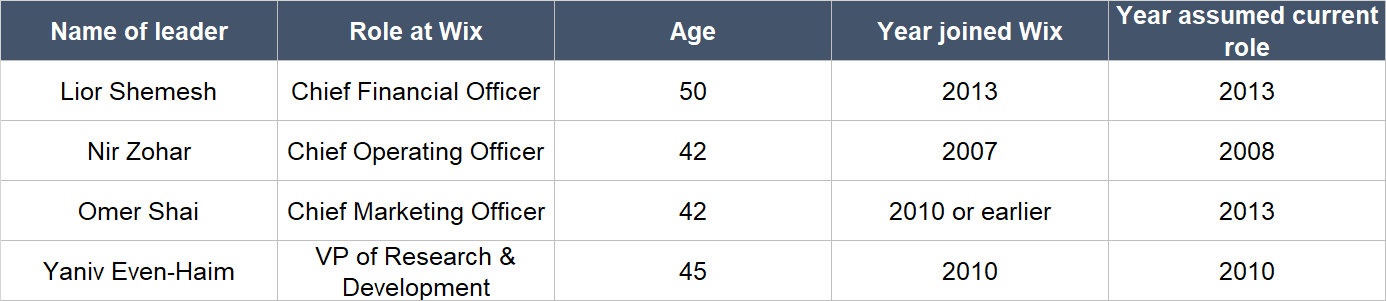

Wix is led by co-founder Avishai Abrahami, 48, who has been in the CEO role since the company’s founding in late 2006 (he was co-CEO from October 2006 to September 2010). The other important leaders in the company include Lior Shemesh, Nir Zohar, Omer Shai, and Yaniv Even-Haim. All of them are relatively young but have long tenure at Wix as key leaders, as shown in the table below.

Source: Wix annual report

Wix’s other co-founders are Nadav Abrahami (brother of Avishai Abrahami) and Giora Kaplan. Nadav Abrahami currently serves as Vice President of Client Development at Wix. Kaplan was Wix’s Co-CEO from 2006 to March 2008 before he became the company’s Chief Technology Officer; he stepped down from Wix’s management bench in February 2020 but remains as an advisor.

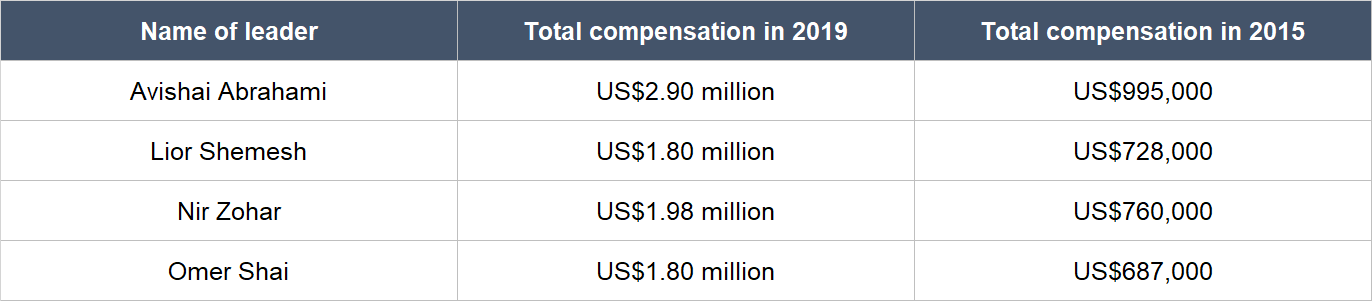

The table below shows the total compensation for Avishai Abrahami, Lior Shemesh, Nir Zohar, and Omer Shai in 2019 and 2015:

Source: Wix annual report

We think that Wix has a great compensation structure for its executives. Here are three reasons why:

- The total remuneration for Wix’s executives looks reasonable to us given the scale of the company’s business.

- 73% to 81% of the four leaders’ total remuneration in 2019 came from equity-based incentives that vest over four years. We typically frown upon compensation plans that are linked to short-term changes in a company’s stock price. But in the case of Wix, the compensation for its key leaders is tethered to multi-year changes in its stock price, which in turn is driven by the company’s business performance. So we think this aligns the interests of Wix’s shareholders with the company’s leaders.

- The total compensation for Abrahami (Avishai), Shemesh, Zohar, and Shai grew from 2015 to 2019 at a range of 147% to 192%; in contrast, Wix’s total revenue growth over the same period was significantly higher at 274%.

As of 2 April 2020, Avishai Abrahami controlled 1.38 million shares of Wix that are worth around US$300 million at the 12 August 2020 share price of US$272. This large ownership stake means the chances are high that Abrahami views himself as being on the same boat as Wix’s other shareholders.

On capability and ability to innovate

Wix was born when the company’s three co-founders – Avishai Abrahami, Nadav Abrahami, and Giora Kaplan – wanted to build a website years ago. Even though all three were tech-savvy, they still found the process excruciating. There was no easy way for people with non-technical backgrounds to build websites and so the trio decided to form a company to solve this pain point. We are attracted to companies that are created because their founders saw a big problem that needed fixing – to us, it’s a sign of the entrepreneurial drive and innovative mindset of the companies’ leaders.

As a testament to the capability of Wix’s management team, the company has done really well over the years at attracting, upselling, and retaining subscribers – these are really important things for a SaaS (software-as-a-service) company such as Wix.

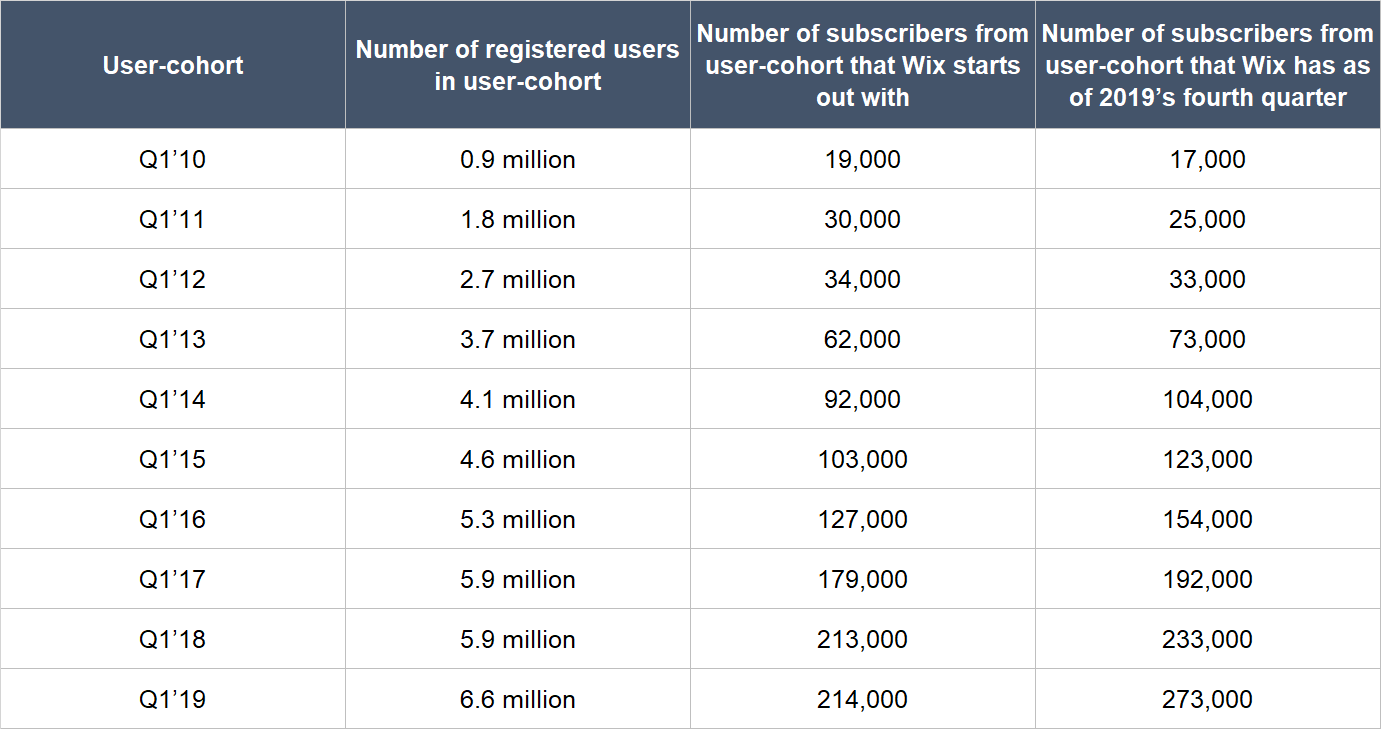

On the point of retention, see the table below. It shows the number of premium subscriptions that Wix captures for each user-cohort over time. In reference to the table, you can see that Wix managed to gain 0.9 million registered users in the first quarter of 2010 – these users are known as the Q1’-10 user-cohort. Within the Q1’-10 user cohort, Wix started with around 19,000 subscribers. Remarkably, by the fourth quarter of 2019 (that’s after 10 years), Wix still had 17,000 subscribers from the Q1’-10 user cohort. The Q1’11 user-cohort, for example, started with 30,000 subscribers for Wix; by 2019’s fourth-quarter, Wix had 25,000 subscribers from this user-cohort.

Source: Wix investor presentation

On Wix’s great track record in attracting and upselling subscribers, check out the table below, which shows Wix’s registered users, premium subscriptions, and average revenue per subscriber from 2013 (the year of Wix’s listing) to the first half of 2020.

Source: Wix earnings updates; average annual revenue per subscriber is derived simply by dividing revenue for the year with the number of premium subscriptions at the end of the year

Wix’s management team appears to have built a great culture at the company. According to Glassdoor, a website that allows a company’s employees to rate it anonymously, Wix has a 4.2-star rating out of 5, and CEO Avishai Abrahmai has a 95% approval rating. We also like the fact that as of end-2019, 50.5% of Wix’s total workforce of 3,071 individuals (including contractors) are in research and development roles; this statistic tells us that Wix’s management is serious about innovation and improving the company’s product-suite.

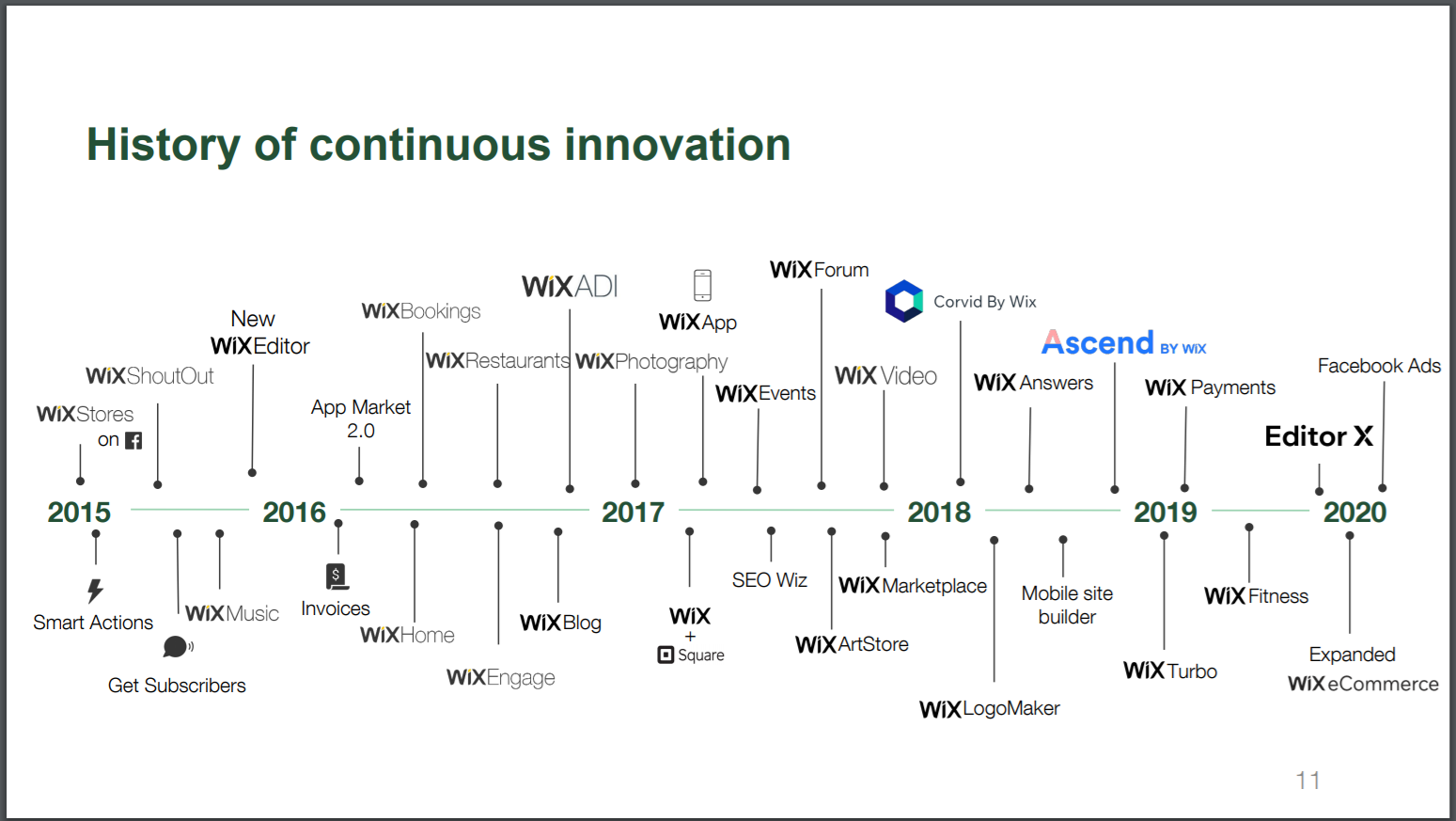

And speaking of innovation, the chart below is another sign of Wix management’s strong appetite for and capability in creating products and services – it shows the flurry of new product/service launches at Wix over the past few years.

Source: Wix investor presentation

The COVID-19 crisis we’re going through now has generated tailwinds for Wix’s business and we’re impressed with management’s willingness to invest. Wix increased its marketing investments in the first half of 2020 – and is continuing to do so – to drive future growth. We think it’s really smart for Wix to go on the offensive and increase its investments into its business at this current time.

4. Revenue streams that are recurring in nature, either through contracts or customer-behaviour

Wix has high levels of recurring revenue. The company has two revenue segments: Creative Subscriptions and Business Solutions. As its name suggests, revenue from the Creative Subscriptions segment come from monthly, yearly and multi-year subscriptions for Wix’s premium website solutions and domain registrations service. The Business Solutions segment generates revenue from the sale of additional products and services that are offered to all of Wix’s registered users.

In 2019, 84.7% of Wix’s revenue of US$761.1 million (US$644.5 million) came from Creative Subscriptions. The remaining 15.3% of Wix’s total revenue in 2019 was from Business Solutions. It’s worth noting too that 84% of Wix’s net overall premium subscriptions as of 31 December 2019 were yearly or multi-year subscriptions, with the remaining 16% being monthly subscriptions; yearly or multi-year subscriptions have a higher chance of renewal than monthly ones.

Drilling down deeper, the Business Solutions segment includes (1) applications developed by Wix or third parties – the apps include Google’s G-Suite and Ascend by Wix – that are sold through Wix’s App Market or elsewhere on the company’s platform and (2) services such as Wix Payments, Wix Answers, Wix Logo Maker, and DeviantArt. Although not explicitly broken down, we believe that at least a part of Business Solutions’ revenue is recurring in nature because users are likely to use some services – such as Wix Payments and Ascend by Wix – repeatedly.

5. A proven ability to grow

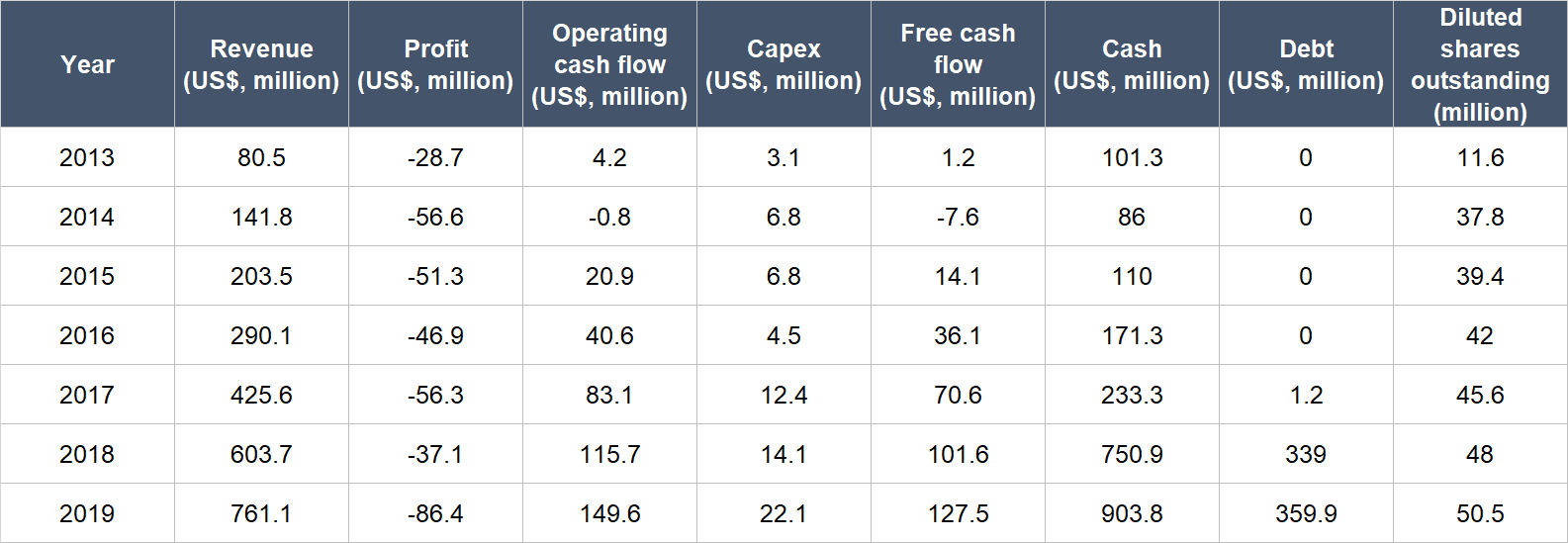

The table below shows the important financial figures for Wix from its listing in 2013 to 2019:

Source: Wix annual reports

A few points about Wix’s financials:

- Revenue compounded at a strong annual clip of 45.4% from 2013 to 2019. Growth was still impressive in 2018 and 2019 at 41.8% and 26.1%, respectively.

- Wix is still making losses, but the good thing is that it started to consistently generate positive operating cash flow and free cash flow in 2015.

- Annual growth in operating cash flow from 2015 to 2019 was strong, at 63.6%. Free cash flow has increased at an even faster pace of 73.5% per year.

- The company’s balance sheet remained robust throughout the time frame under study, with significantly more cash and investments than debt.

- At first glance, Wix’s diluted share count appeared to increase sharply from 2013 to 2014. But the number we’re using is the weighted average diluted share count. Wix was listed in November 2013 and the company ended 2013 with a share count of around 37.5 million. Moreover, Wix’s diluted share count has grown at an acceptable (but still high) rate of 6.4% per year from 2015 to 2019, which is much slower than the company’s free cash flow growth. This means that the all important metric, free cash flow per share, has still increased at a healthy clip.

We mentioned earlier that the current COVID-19 pandemic has benefitted Wix. Just to be clear, the company was already growing rapidly even before COVID-19 appeared – what the virus has done is to accelerate digital trends that are in favour of Wix. During the first half of 2020, Wix posted strong results. Revenue was up 25.7% year-on-year to US$452.0 million. The company’s loss ballooned from US$47.5 million to US$96.9 million, but operating cash flow surged 31.5% from a year ago to US$95.0 million, driving a 42.5% jump in free cash flow to US$86.6 million. For the third quarter of 2020, Wix anticipates strong revenue growth of 26%-27%, although free cash flow is expected to fall by 42%-49% – we’re not worried about the projected decline in free cash flow.

6. A high likelihood of generating a strong and growing stream of free cash flow in the future

Over the past few years, Wix’s free cash flow has been consistently positive and growing. We think it’s likely that the company’s free cash flow will continue to increase at a rapid clip in the future for two reasons.

First, it looks likely to us that Wix will continue to produce strong top-line growth. As we discussed earlier, COVID-19 is a positive catalyst for Wix’s business. But even when the pandemic blows over, we think Wix is set to capitalise on strong secular tailwinds with a platform that is well-placed to meet the growing demand for businesses to shift online.

Second, we think Wix can enjoy a higher free cash flow margin in the future as its business scales. The company’s trailing free cash flow margin (free cash flow as a percentage of revenue) is already respectable at 18%. But we think there’s still plenty of room for improvement given the typically asset-light nature of a software business.

Valuation

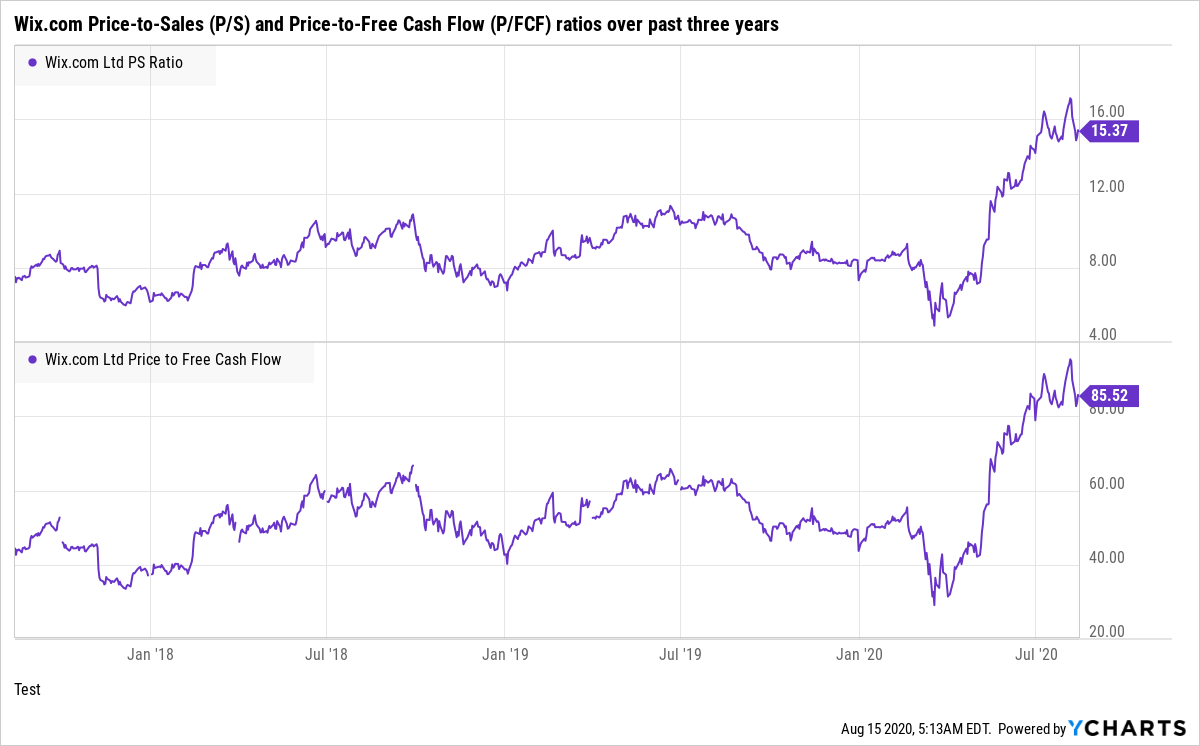

We bought Wix shares for Compounder Fund at an average price of US$275 each. This translates to trailing price-to-sales (P/S) and price-to-free cash flow (P/FCF) ratios of 17.2 and 95.6 respectively. These are high valuations in and of themselves; even if we apply a 30% free cash flow margin to Wix’s current revenue, we’re looking at a projected P/FCF ratio of 57. Furthermore, Wix’s P/S and P/FCF ratios are high relative to history; both ratios have been climbing over the past three years as shown in the charts below.

(We chose a three-year timeframe because Wix’s free cash flow numbers were still small in 2015 and 2016 and this distorted the P/FCF ratio in these years. The valuation numbers in the chart also differ slightly from our calculations, but this is not important. The focus here is the general picture of how the two ratios have changed over the past three years.)

We recognise that a high valuation is a risk – any slowdown in growth could cause Wix’s valuation ratios to compress and lead to an extended decline in its share price. But we’re not too concerned. We believe that Wix still has plenty of growth ahead, and can easily compound revenue at north of 20% per year for many years in the future. Meanwhile, its sticky subscription business model also means that past user-cohorts continue to provide a consistent and regular stream of revenue, allowing Wix to concentrate its efforts on acquiring new registered users and converting its huge base of registered users into paying subscribers. We’re also encouraged by Wix’s ability to innovate and consistently create new revenue streams through the introduction of new products/services.

The risks involved

There are four key risks with Wix that we’re keeping an eye on.

First, Wix competes in a highly fragmented market. WordPress dominates this space but there are also others such as Squarespace and Weebly (and many more) that are also fighting for market share. Wix believes its platform is the most well-equipped for users to quickly and easily bring their businesses online; by looking at Wix’s historical growth, many users and customers agree. But competition still poses a risk to Wix. For example, in the area of providing software for companies to sell online, there is the rapidly-growing Shopify (another of Compounder Fund’s holdings). Although we believe there is a large enough market for both Wix and Shopify to thrive in the e-commerce shop-front space, Shopify offers more well-rounded services such as logistics and fulfilment capabilities and this may pose a threat to Wix’s e-commerce-related ambitions. Wix’s ability to innovate and provide a great experience for users will be key to it maintaining or winning market share.

Second will be Wix’s high valuation. It’s something we’ve already discussed so we will not repeat this here.

Geopolitical risk is the third. Wix is headquartered in Israel and more than half of its employees are based in the country. Historically, Israel has had – and continues to have – tense relationships with its neighbouring countries. But we’re comforted by the fact that Wix has managed to grow strongly since 2012 despite Israel having been in multiple armed conflicts with its neighbours over the past decade. Nonetheless, we’re watching the situation.

Lastly, there’s key-man risk. Avishai Abrahami has been leading Wix since its founding 14 years ago in 2006. In our view, he has been a key architect of the company’s growth over the years. Should he step down, we will be observing the succession plan closely.

Summary and allocation commentary

Summing up Wix, we have a company that aces Compounder Fund’s investment framework:

- Wix has captured less than 1% of its addressable market. Importantly, its market – website creation and management – is also likely to enjoy lasting demand as businesses increasingly want to build and maintain an online presence.

- The company’s balance sheet is robust with significantly more cash than debt

- Wix is founder-led, and it has a well-designed compensation structure for its leaders. The management team also has a solid track record in innovation and growing Wix’s user and subscriber bases.

- The lion’s share of Wix’s revenues come from subscriptions, which are recurring in nature. Moreover, the company’s subscribe-base is incredibly sticky.

- Wix has produced strong revenue growth since 2013, and free cash flow has also increased consistently at a rapid clip since 2015.

- The company is already free cash flow positive with a respectable trailing free cash flow margin of 18%. As Wix’s business scales over time, it’s likely that its free cash flow margin can improve. So, we think Wix has a high likelihood of generating a strong and growing stream of free cash flow in the future

In our view, the key risks for our investment in Wix are competition, a high valuation, Israel’s tense relationships with its neighbours, and key-man risk.

We initiated a 2.5% position in Wix – a medium-sized allocation – with Compounder Fund’s initial portfolio. The company has tremendous room to expand its business, but competition in its space could also easily intensify in the future and stunt its growth. Moreover, Wix carries a high valuation. The company has all the traits that we want in Compounders so we’re happy to own its shares. But for now we think that a medium sizing is appropriate from a risk/reward perspective.

And here’s an important disclaimer: None of the information or analysis presented is intended to form the basis for any offer or recommendation; they are merely our thoughts that we want to share.